Daily Economics Dashboard - 15 April 2021

An overview of key economic and financial metrics.

2 minutes to read

Download an overview of key economic and financial metrics on 15 April 2021.

Equities: In Europe, stocks are higher. Gains have been recorded by the STOXX 600, FTSE 250, CAC 40 and DAX, which have all increased +0.3% over the morning. In Asia, the S&P / ASX 200 (+0.5%), KOSPI and TOPIX (both +0.4%) all closed higher, however, the CSI 300 (-0.6%) and Hang Seng (-1.4%) were both down on close. In the US, futures for the S&P 500 and Dow Jones Industrial Average (DJIA) are +0.5% and +0.4%.

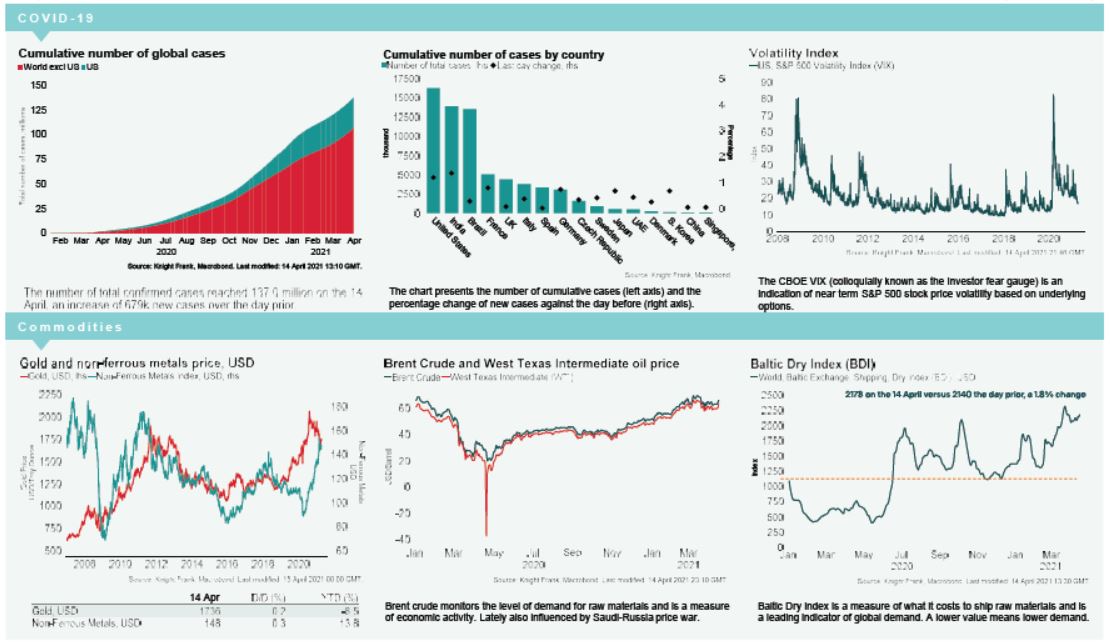

VIX: After increasing +2% over Wednesday, the CBOE market volatility index has since decreased this morning, down -0.7% to 16.9, remaining below its long term average of 19.9. The Euro Stoxx 50 volatility index has also declined, down -3.6% to 15.6, its lowest reading since December 2019 and comfortably below its long term average of 23.9.

Bonds: The UK 10-year gilt yield and US 10-year treasury yield have both compressed -2bps to 0.79% and 1.61%, while the German 10-year bund yield is down -1bp to -0.28%.

Currency: Sterling and the euro are currently $1.38 and $1.20, respectively. Currency hedging benefits for US dollar denominated investors into the UK and Eurozone are at 0.52% and 1.66% on a five year basis.

Oil: Over Wednesday, Brent Crude and the West Texas Intermediate (WTI) increased +4% and +5% to $66.25 and $63.15, their highest levels in a month. This morning, Brent Crude and the WTI have since moderated to $66.10 and $62.83, respectively.

Baltic Dry: The Baltic Dry increased +1.8% on Wednesday to 2178, its highest level since 26th March. Prices were pushed higher by panamax rates which increased +6.3% yesterday, as well as capesize rates which added +0.3% to their highest level since mid January. While the index is currently +59% above where it was at the beginning of January, it remains -6% below the March peak of 2,319.

European Industrial Production: Eurozone industrial production declined -1% over the month of February, compared to a +0.8% increase in January and market expectations of a -1.1% decline. Industrial production contracted -4.7% m-m in France and -1.8% in Germany, while in Spain and Italy, it remained broadly flat.