London new homes update – Summer 2024

Demand for new build homes in London eased in the run up to and just after the General Election, but more recent data points to building momentum.

4 minutes to read

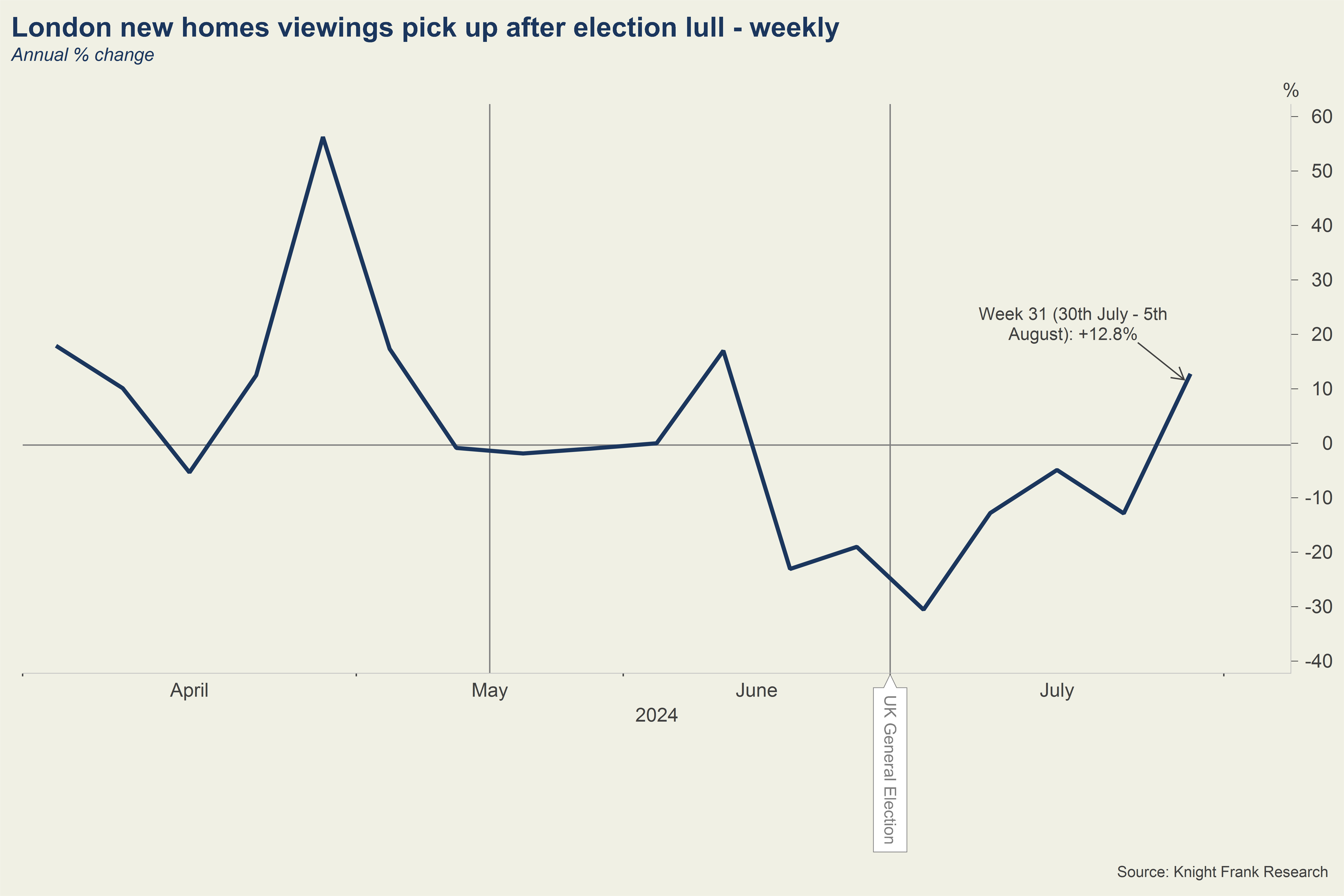

Overall, the total number of offers made on new build homes in the capital fell around 50% in both June and July this year compared to a year earlier, while viewings eased by just over 10%. The election also caused activity to drop off across the broader London housing market, with new offers falling to their lowest level in June and July combined since 2012, Knight Frank data shows.

It comes after an improvement in Spring, when the total number of offers made on new homes in the capital rose 9% in April compared with a year earlier, while viewings were up 17%.

But last week, viewings started picking up again, climbing 11% in the seven days ended 5th August compared to year earlier (see chart), while weekly offers made have now recovered back to 2023 levels.

Overall, sentiment has improved with the Bank of England cutting the base rate for the first time in over four years last month to 5% from 5.25%. Financial markets are pricing in a further 0.25% cut in November.

Domestic demand for new homes picked up in the first half of 2024, and has been supported by an uptick in international buyers, who have returned following the lifting of all international travel restrictions for those entering the UK in March and after the end of the third national lockdown in July 2021.

Buyer appetites

Currently, buyers are focused on well-located central schemes in London. Current top-selling schemes in the London market include One and 10 Park Drive in Canary Wharf which have just 56 one or two bed apartments remaining out of a combined 830 private units. These schemes completed in 2022 and 2020 respectively. Notting Hill’s The Auria has only 20 remaining private apartments out of a total 111, which are due for completion in late 2024. Other schemes which have proven popular include Capella, the final residential building on the King's Cross estate, which has just six flats remaining of a total 120 private units.

In the first half of 2024, off plan sales accounted for a third of all new homes sold with Knight Frank in London, where at least one year has elapsed between the exchange and completion date. This is up from a quarter in H1 2023.

Further over in West London, and particularly popular with the more domestic based buyers is Chiswick Green, the former Empire House office building site. Out of 121 private apartments, just 45 are remaining. Two of the blocks have completed with the third remaining due to complete this month.

In contrast, other schemes in the capital have seen a majority of sales achieved off-plan to British buyers, such as The Clay Yard in Hampstead which is due to complete this summer. So far, The Clay Yard has sold around 75% of its available 102 private apartments. The majority of these sales were off-plan to domestic purchasers.

The concept of buying off-plan is, however, less familiar to most UK buyers who typically prefer to view build complete product before making a decision, while uncertainty over mortgages has also led some to hold off buying until a later stage.

This, coupled with the fact developers have slowed down their build out rates as demand has reduced, means options for completed homes are more limited in some areas. Outer London has seen a 50% fall from a peak of just over 2,100 unsold finished homes in Q4 2019 down to 1,030 in Q2 this year.

Delivery stays static

More broadly, as demand does pick up, the availability of stock is a potential concern. Housing delivery in London remains sluggish, despite more ambitious targets coming out of the Labour party. The new government has asked London Mayor Sadiq Khan to more than double the number of new homes being built in the capital each year. He has been set a new target of around 80,000 homes, which compares to just 35,000 built in the 12 months to March 2023.

More recent data points to stable housing delivery rates in the capital boosted by a surge in starts last year to beat regulation deadlines. Energy Performance Certificates granted to new homes, a useful barometer of supply, rose in the first half of 2024 compared to H1 2023. New supply has plateaued in London around the 30-35,000 market for the past three years.

The slight pick-up in delivery in the first six months of the year can in part be explained by a jump in new starts last year ahead of environmental regulations coming in. In Q2 2023, new starts in London more than doubled on quarter to over 7,200. This coincided with changes to new home building environmental standards which came into effect on the 15th of June and encouraged some builders to start work on homes ahead of the rules coming in.

In the near-term, the capital faces a supply crunch due to a collapse in new housing granted permission. Out of all regions in the UK, London saw the steepest drop (35%) in new homes granted approval last year versus 2022.