Uncertain Outlook for Prime London Sales Market in 2025

November 2024 PCL Sales Index: 5,279.8

November 2024 POL Sales Index: 275.8

3 minutes to read

UK housing market forecasts should come with a longer list of caveats than normal at the moment.

Short-term distortions created by the Budget and doubts about the long-term effectiveness of Labour’s economic plan mean buyers and sellers will need to pay close attention to the economic data in 2025.

In prime London markets, there was an immediate sense of relief the Budget was better than feared, with many measures publicised ahead of time. As a result, the number of exchanges in October was 30% higher than the five-year average, Knight Frank data shows. The figures were flattered by deals done ahead of a stamp duty increase on 31 October.

However, in November, there was a 19% decline, which suggests momentum isn’t building convincingly yet. In the same month, the number of new prospective buyers registering in London was 5% down on the five-year average while the number of offers made was 11% lower.

In the wider UK market, mortgage approvals and transaction numbers climbed to an 18-month high in October but the picture is nuanced.

The fact sub-4% mortgages have largely disappeared in recent weeks, and some buyers are pre-empting a stamp duty hike in April, means the long-term outlook isn’t necessarily as positive as the numbers suggest.

More sustainable momentum will only come if the economy starts heading in the right direction. Any upwards pressure on unemployment, borrowing costs or inflation would weaken demand and transaction volumes at all price points. We recently downgraded our forecasts to reflect those risks.

Prices in prime central London were flat in November, taking the annual change to -1.4%, which was the narrowest decline in 15 months. Meanwhile, there was a 1.1% increase in the year to November in prime outer London, with demand being supported to a greater extent by needs-driven buyers.

Our latest revised price forecasts can be found here.

The picture is further complicated in higher-value markets by uncertainty among overseas investors and entrepreneurs about what will replace the non dom tax regime.

Although the government has introduced a relatively uncompetitive four-year residence-based system, it is still talking to lobby group Foreign Investors for Britain (FIFB) about a possible Italian-style flat tax. In the meantime, FIFB will attempt to amend sections of the finance bill as it passes through Parliament.

The other major event that could affect the UK economy is the US Presidential election that took place last month. See our analysis of what it could mean for UK property markets here.

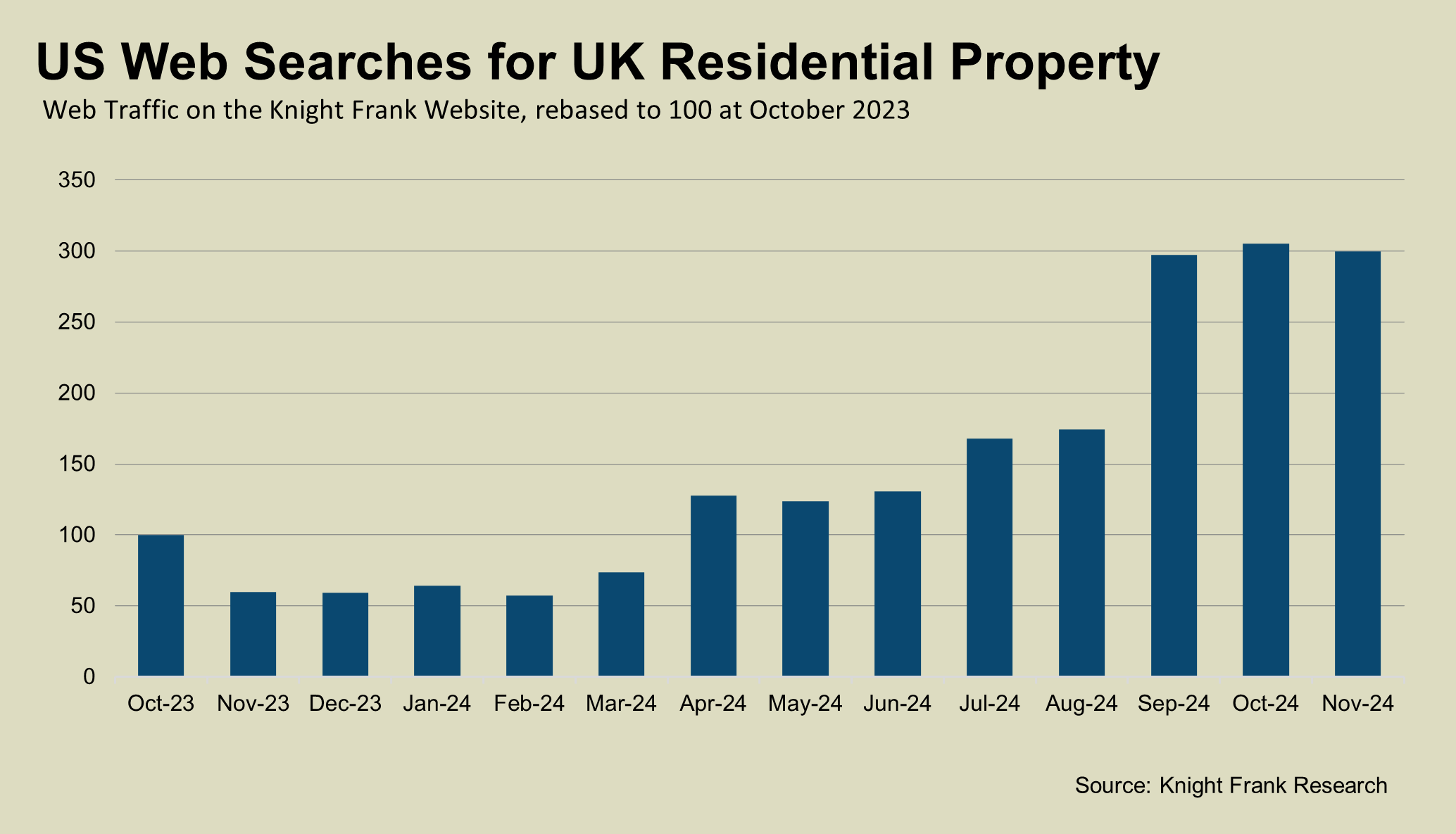

The vote was expected to polarise opinion and Knight Frank web traffic data suggests that was the case. There was a marked increase in searches from the US for UK property in recent months, as the chart below shows. Traffic this November was five times higher than the same month last year.

Furthermore, the busiest day of the year was 5 November, the day of the election, when traffic was 20% higher than any other single day in 2024.

There is anecdotal evidence of more US buyers looking in the UK to start their search since the election, but not in enough numbers to have a material impact on prices or sales volumes.

For that, UK economic data will play a far more important role.