Post-Budget Certainty Will Support Super-Prime Country Market

With a general election behind us, a Budget that did not explicitly target wealth and clarity around property taxes, super-prime demand is expected to strengthen next year.

4 minutes to read

Political and economic uncertainty means discretionary buyers have been more circumspect than normal this year.

The first Labour government in 14 years is taking UK tax policy in a new direction, interest rates have vacillated, and Donald Trump recently won power in the US after a polarising election.

It’s no surprise that UK super-prime residential transactions have fallen in 2024, as we explored here in London.

It has been a similar story outside the capital.

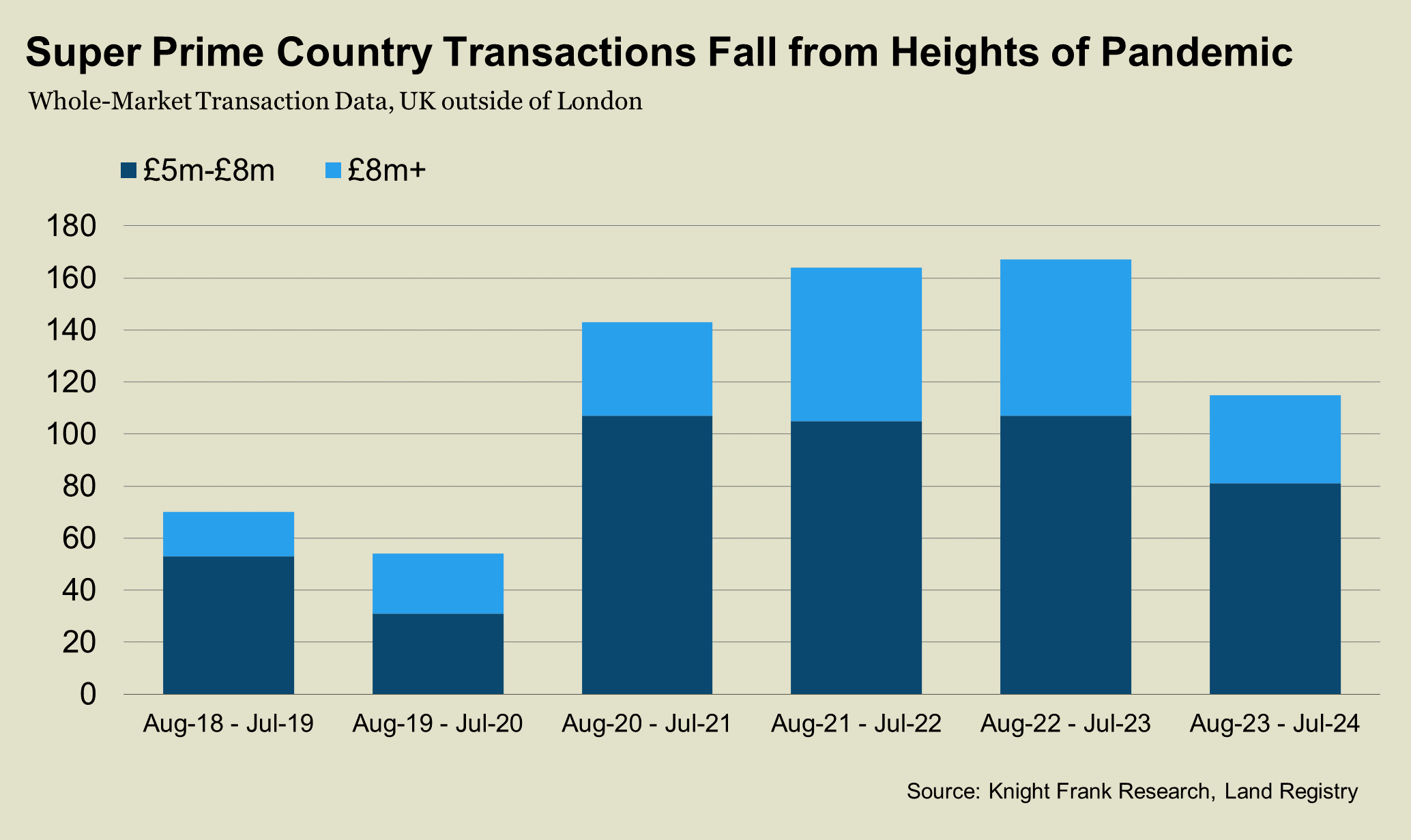

There were 115 deals above £5 million in England and Wales outside London in the year to July 2024, which is down by a third from 167 in the previous 12-month period. Above £8 million, there were 34 transactions versus 60 a year earlier, whole-market data shows.

The figures were also lower than the previous two years, when successive pandemic-era lockdowns drove demand for space and greenery.

For transactions below £2 million, there was a smaller fall of 9% over the same period, Knight Frank data shows. It demonstrates how lower-value markets, which are driven by needs-based buyers moving for schooling or employment, have performed better.

“Uncertainty stagnates markets, which we had this year in the run-up to the election and during the prolonged wait for the Budget,” said Ed Rook, head of the Country department at Knight Frank. “There was talk that those with the broadest shoulders would bear the heaviest load, which created renewed concerns about the prospect of a mansion tax among other things.”

How did the super-prime market react to the Budget?

Following the Budget, the top rate of stamp duty rose to 19% although the top rate of capital gains tax remained at 24% for residential property. While no measures specifically targeted wealth, there were changes to business property relief, the status of non doms and the taxation of private equity. Our full analysis can be found here.

Mortgage rates have also increased as financial markets digest rising levels of government borrowing and the impact of higher employer national insurance costs on inflation and the labour market.

“The fact rates have risen hasn’t gone down particularly well, even in the super-prime market,” said Ed. “If you’re not borrowing money there is a negative impact on sentiment if you see demand, transactions and prices going down.”

However, a combination of pent-up demand and more certainty following the general election and Budget means super-prime activity is likely to increase in 2025. The scrapping of the non dom tax status should not have a material impact on demand as such individuals typically account for 10% to 15% of buyers above £5 million outside the capital, said Ed.

“There is more pent-up demand at the discretionary end of the market. After a subdued autumn we may see a stronger spring as buyers adjust to new borrowing costs and sellers show more flexibility on price after being on the market for a prolonged period of time. A lack of supply won’t be a problem.”

Other factors that will support demand in the super-prime market include higher levels of cash and equity as well as the pace of global wealth creation. The number of ultra-high net worth individuals is forecast to increase by 28% in the five years to 2028, according to the Knight Frank Wealth Report.

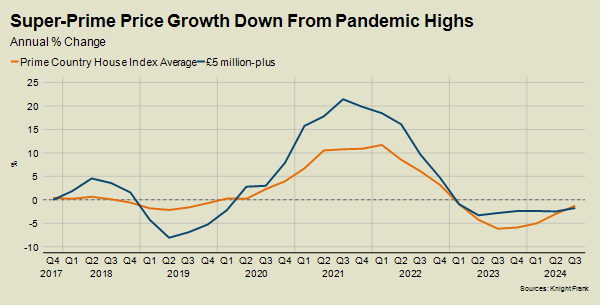

Prices above £5 million in the Country fell 1.7% in the year to Q3 2024, which is down from an increase of 21% at the height of the pandemic, as the chart below shows. As demand picks up, we expect average prices in the Country to rise by 17.6% over the next five years, according to our latest forecast.

The Americans are coming

Will those buyers coming off the sidelines include a number from the US following the election last month?

“Some Hollywood royalty have already been in touch, looking for privacy as their number one requirement and that is something the UK countryside can give you,” said Ed.

“Demand is across all prices and not limited to the Cotswolds and we have seen strong interest in the Home Counties. Some have been told by friends to focus on one particular area, whereas others are more open-minded.”

The domestic competition should be less stiff than during the pandemic, when a large number of buyers swapped their urban life for a rural one.

“Buyers spend more time and invest more heavily in the Country market since Covid,” said Ed. “There is still strong demand for the Country lifestyle, but it’s no longer a race.”