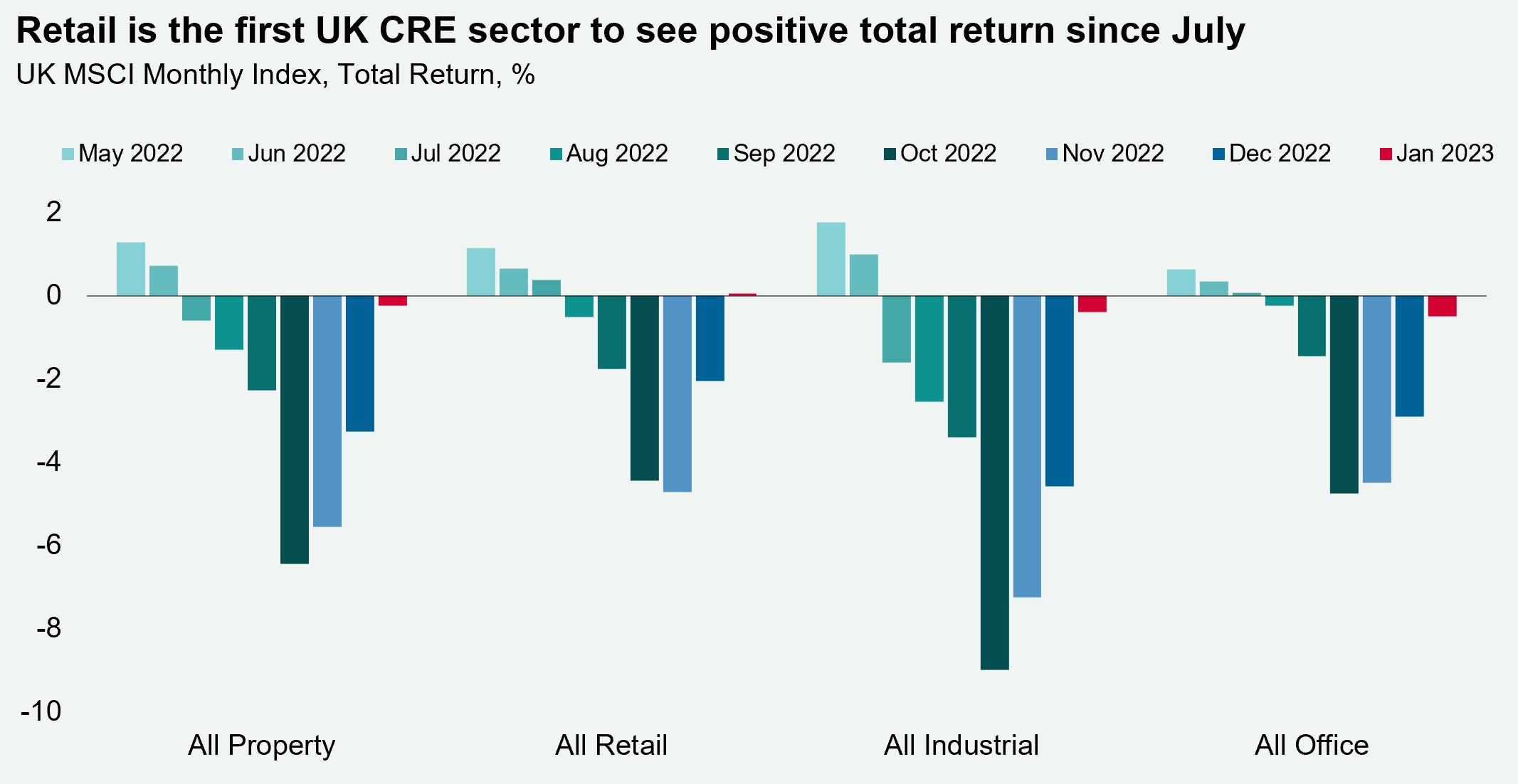

Leading Indicators | Inflation | Public Finances | Business Profitability

Discover key economic and financial metrics, and what to look out for in the week ahead.

2 minutes to read

Here we look at the leading indicators commodities, trade, equities and more. in the world of economics. Download the dashboard for in-depth analysis into commodities, trade, equities and more.

Inflation continues to slow

UK inflation slowed for the third consecutive month in January to 10.1%, from 10.5% in December, better than expectations of 10.3%. Producer price inflation also moderated for the seventh successive month in January to 14.1%. The positive inflation news has left market commentators deliberating the Bank of England’s (BoE’s) next interest rate decision on 23rd March. Capital Economics outlined that the likelihood of its 4.5% peak interest rate forecast is “now a bit slimmer”, while Oxford Economics expects the central bank to lift its rate by 25bps to 4.25% in March, where it will remain until at least the end of the year. Before the BoE’s next MPC decision, it will want to see wages and inflation slow further, as the MPC stated this would be “key” to determining the necessity of further hikes.

UK Public finances beat expectations

The UK’s Public sector net borrowing (PSNB ex) was in a surplus of £5.4bn in January, £5.0bn higher than the OBR forecast. In the financial year to January, public sector borrowing was c.£117bn, c.£30bn less than what the OBR forecast. Better than anticipated public finances data will likely provide Chancellor Hunt with more scope to offer support in the upcoming spring budget on 15th March. We could see some funds re-allocated towards the UK’s Levelling Up agenda that has experienced delayed funding and tightened spending controls in the last year. As part of the Levelling Up agenda, the relocation of some of the UK’s civil service is expected to ‘bolster employment and secure viability for some development schemes’, which could be supportive of real estate demand nationally, as explored in our recent UK cities research.

UK business profitability moderates, but activity returns to growth

The net rate of return for private non-financial corporations fell by 10bps to 9.7% in Q3 2022. However, for businesses on the UK continental shelf, the net rate of return was 24.9%. This was the seventh consecutive quarter of increasing profitability for businesses and the highest value in 14 years, driven by elevated gas and oil prices. Meanwhile, the latest UK PMI results surprised on the upside, with both services and manufacturing businesses reporting growth for the first time in six months (figure above 50), at 53.3 and 51.6 in February, respectively. The UK life sciences sector has been particularly robust, with 913 life sciences companies incorporated in the UK in 2022, the second highest year on record. Indeed, the supply of suitable space for life sciences occupiers remains constrained in the Golden Triangle of Oxford, Cambridge and London.

Download the latest dashboard