Rate cuts before the end of 2023?

Making sense of the latest trends in property and economics from around the globe

5 minutes to read

Two perspectives

The Bank of England yesterday raised the base rate by 50 basis points to 4%. The minutes published alongside the decision paint very different pictures of the short and long term outlooks.

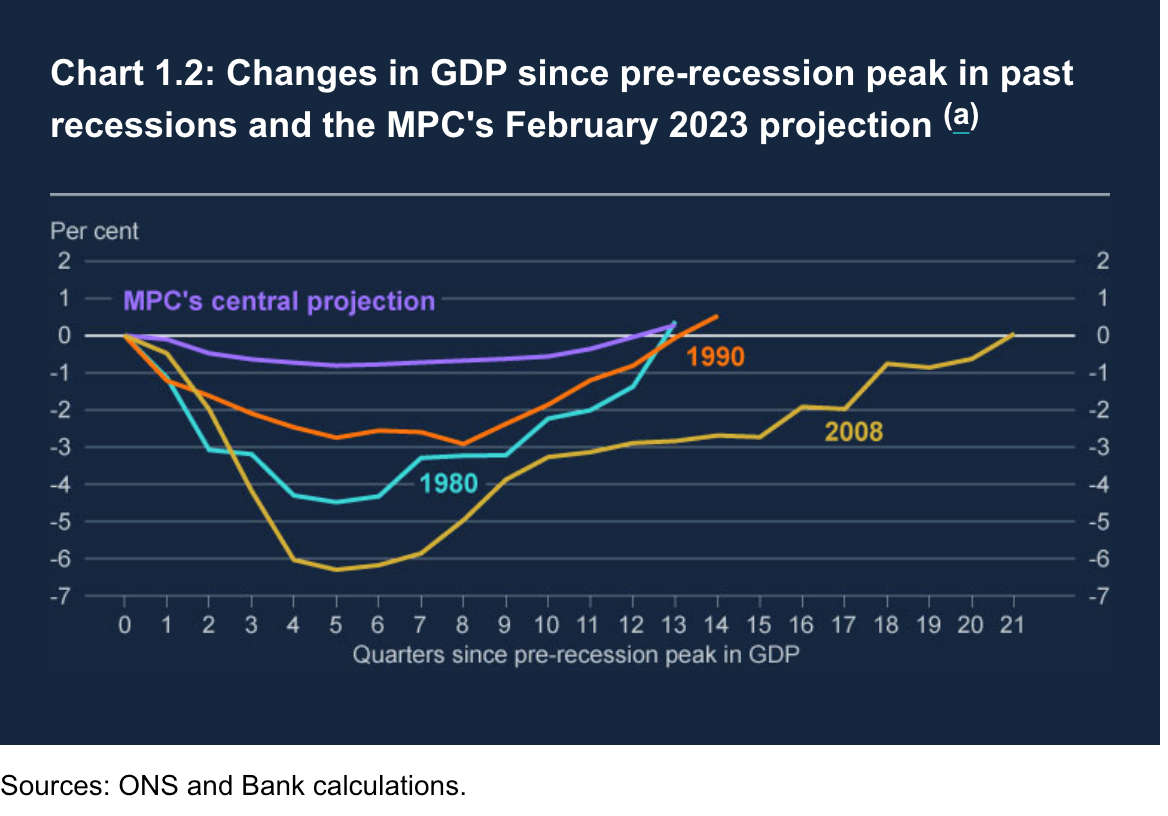

Inflation has likely peaked across many advanced economies, including the UK, according to the Monetary Policy Committee. In fact, inflation will likely fall below the Bank's 2% target next year. Markets are now pricing in one more quarter point hike later in 2023 and for rates to fall below 4% by the end of the year. The recession predicted by the MPC in November will be shorter and shallower - more akin to flatlining - see chart. The FTSE 100 hit its highest level for two weeks and five year swaps dropped to their lowest level since late August, which is good news for mortgage rates.

However, the Bank took a bleak view of the UK's longer term prospects, summarised nicely here by the FT. GDP isn't expected to reach pre-coronavirus levels until 2026. As expected, the outlook is more in line with the IMF's published earlier this week due to declining participation in the labour market, the impact of higher interest rates on mortgages, and the UK's higher dependency on natural gas. The latter is a particular problem for UK housing - an issue we covered in the latest edition of Intelligence Talks.

Disinflation

The US Federal Reserve this week opted for a quarter-point increase to the key interest rate following a year of larger hikes. “The disinflationary process has started,” Fed Chair Jerome Powell said at the subsequent press conference.

As in the UK, there is a disconnect between what the Central Bank says and what markets are hearing. Powell said he expects as many as two more rate hikes this year with no cuts, while investors continue to bet that rates will close the year lower than they are now.

Why does the Fed persist with the hawkish message despite inflation falling? The most straightforward explanation is that the progress we have seen so far only reflects the reversal of temporary factors that were exacerbated by the pandemic - this is good from Matthew Klein. The Fed's preferred measure of inflation - the so-called 'supercore' measure of PCE services prices excluding services and housing - is proving stubborn.

Mortgage rates dropped again this week. The 30-year fixed rate is down nearly a full point since November.

Middle Eastern buyers in Europe

Middle Eastern buyers of prime central London homes hit a four-year high in the second half of 2022 as they took advantage of the weak pound and the relaxation of Covid-19 restrictions, according to data we shared with Bloomberg last week. Buyers from the region accounted for 11% of property transactions, putting them just behind investors from Europe and the UK.

Buyers from the region have been active in Paris, too, Kate Everett-Allen writes this morning. Enquiries from UAE, Saudi, Qatari, Omani and Kuwait-based residents have increased significantly in the last six months. With several Middle Eastern currencies pegged to the dollar, some buyers saw a 19% price discount when purchasing in the eurozone in September 2022 compared to a year earlier.

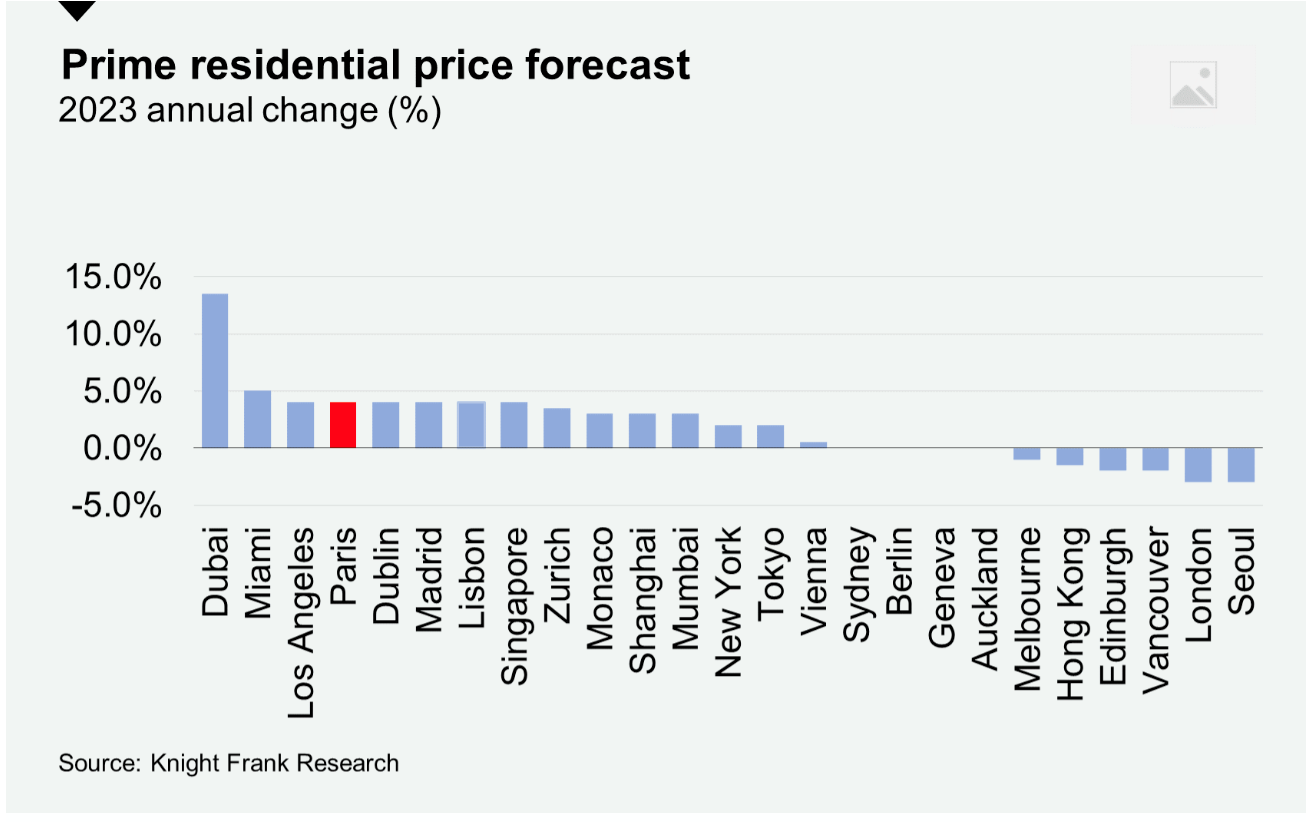

Prices across the French capital’s prime arrondissements increased 6.2% in 2022, down only marginally from the 6.3% registered in 2021. At €20,000 per sq m, luxury prices in the city are competitive when compared with those in New York at €28,000 per sq m and London at €27,000 per sq m. Despite mounting economic headwinds Knight Frank forecasts prime price growth of 4% in 2023, putting Paris in joint third place out of 25 global cities.

Trimming budgets

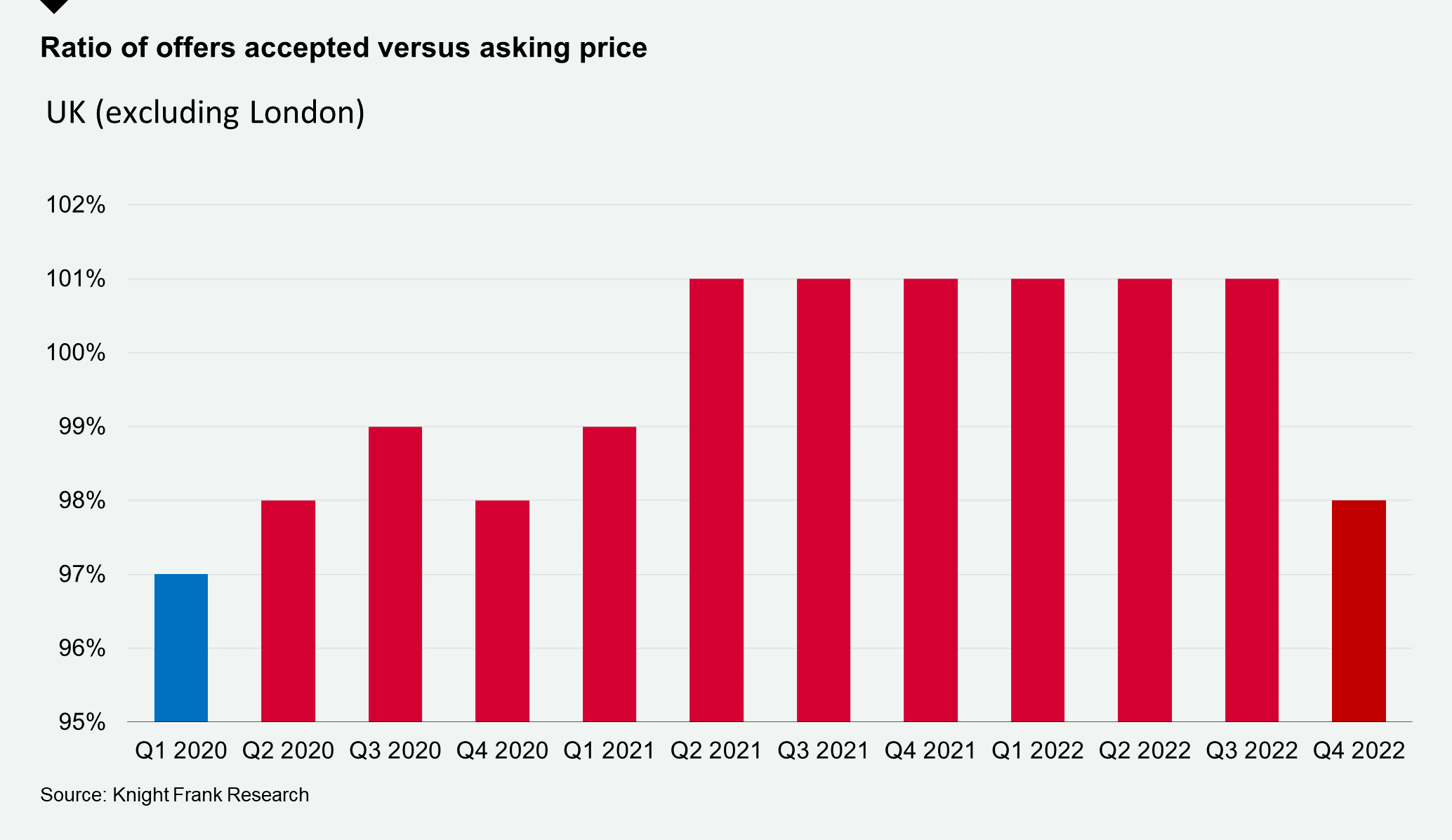

Buyers in UK regional property markets have responded to the recent rise in borrowing costs by realigning their budgets, rather than abandoning purchases, writes Chris Druce.

An analysis of Q4 data (which excludes London) found that offers were accepted on average at 98% of the asking price in the fourth quarter of 2022. The figure was last lower in the first quarter of 2020 (97%), just as the pandemic began. Offers have since regularly exceeded the asking price during the so-called race for space - see chart.

“We saw a few fall throughs due to funding, but mainly it’s been about adjusting to new circumstances,” said James Toogood, office head at Knight Frank Bristol. “One customer that missed out on a £1.5m home in the summer returned in the autumn searching around the £1.1m mark. Another client is progressing with their purchase but has decided to halve the size of their mortgage.”

Where will the land come from?

The government this week published its environmental improvement plan with a pledge to ensure every household will be within a 15-minute walk of a green space or water.

The measures will include commitments to restore at least 500,000 hectares (1.2m acres) of wildlife habitat, and 400 miles of river. That will include 25 new or expanded national nature reserves and 3,000 hectares (7,400 acres) of new woodland along England’s rivers.

It's a bold plan that's light on detail. If all the government targets around land use are to be achieved, it would require an additional area twice the size of Wales by 2050, according to The Royal Society landscapes policy report.

Mark Topliff asks the big question - where will the land come from?

In other news...

Year-round resorts top the wish list of ski home purchasers

Elsewhere - New York property tycoon to give worn-out offices ‘back to the bank’ (FT)