Quantifying Obsolescence Risk

The legal requirement to improve the EPC ratings of buildings raises the obsolescence risk for c.7m sq ft of institutional grade leases with a rating below C due to expire by 2027.

3 minutes to read

We believe a structural shift in demand for better quality buildings is unlikely to be filled by the current pipeline under construction, providing development opportunities in those locations with an under supply of new and refurbished buildings.

Shabab Qadar – London Research Partner

Quantifying obsolescence in London office markets

We’ve mapped the government’s database of energy performance certificates to the London office market and broken-down EPC ratings by market. Across London, approximately 140m sq ft of office space has an EPC rating below grade C, a figure which represents 51% of total office floorspace. Breaking down by London’s submarkets shows there is some variation in the EPC C rated stock. With the highest proportion of office space rated below grade C are Rest of Docklands (70%), Knightsbridge/Chelsea (68%) and Victoria (67%).

In terms of London’s three core CBD’s, Canary Wharf ranks favourably with 46% of certified floorspace below grade C, while the City Core is at 55% and the West End Core has the highest level at 60%. Across London, this represents 60m sq ft of floorspace space that will require upgrading to achieve higher levels of energy efficiency.

Impending lease expiries with the greatest obsolescence risk

Between now and 2027, around 7m sq ft of institutional grade leases in London with an EPC rating below grade C, are due to expire. This represents the floorspace with the highest level of re-letting risk, which without capital expenditure to retrofit or refurbish to higher EPC ratings, will no longer be fit for purpose.

Breaking this data down by size-band is especially interesting. Only 5% of those leases expiring with an EPC below C are in buildings of over 75,000 sq ft. Almost three quarters of expiring floorspace with an EPC below C are in accommodation of less than 25,000 sq ft.

The pipeline is not large enough

Historically, the development pipeline serves to replenish the ageing stock reaching the end of its life cycle, providing better quality office space. The present pipeline under construction contains 11m sq ft of speculative space with a delivery timeframe of 2023-26. Based on long-term trend levels, this falls short of the expected level of take-up of new and refurbished buildings. We estimate this to be around 11m sq ft of under-supply of the best quality buildings.

Without a significant increase in construction, most of London’s office submarkets could see an under-supply. Our analysis suggests a shortfall of almost 7m sq ft in the City, nearly 3m sq ft in the West End and the remainder in Docklands and Stratford.

Moreover, in 2022 almost 7m sq ft of take-up was for new and refurbished space, representing close to 60% of all lettings. This is 20% above the long-term trend and the highest level for refurbished take-up we’ve registered since introducing this category in 2004.

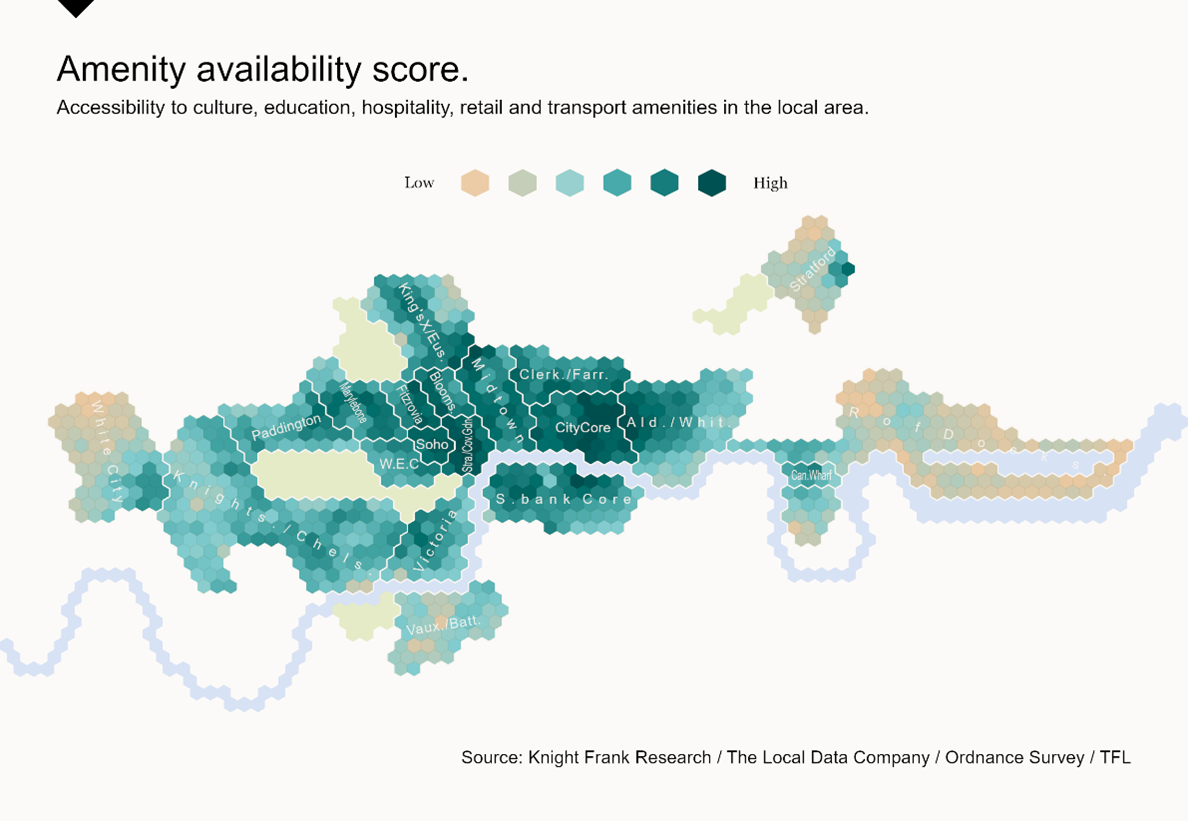

Amenity provision

While the regulatory push to improve the energy efficiency of buildings is a mandatory characteristic of best-in-class buildings, from the occupier’s perspective, amenity provision and commutability are also key criteria. We’ve extended our supply side analysis to calculate a bespoke ‘amenity provision’ score for London’s office submarkets.

We’ve calculated weighted scores by aggregating the quantity and quality of key amenity categories, including Arts and Culture, Education, Health and Wellbeing, Hospitality, Retail and Transport. Furthermore, we’ve used geospatial techniques to account for proximity of amenities to offices.

The top five London submarkets with the highest amenity provision scores include Strand/Covent Garden, Soho, City Core, Fitzrovia and Midtown. The five at the bottom of this table are Rest of Docklands, Stratford, White City, Vauxhall/Battersea and Knightsbridge/Chelsea.

Combining our amenity provision scores with our projections for locations likely to see a shortfall of best-in-class floorspace, or where there are buildings with high obsolescence risk, is a useful location planning tool to better inform the decision-making process.

Figure – Amenity scores highest in most centrally located submarkets