Prime London sales market resilient as supply builds

May 2023 PCL sales index: 5,438.8

May 2023 POL sales index: 277.0

3 minutes to read

The mini-Budget is fast becoming a distant memory in the prime London property market.

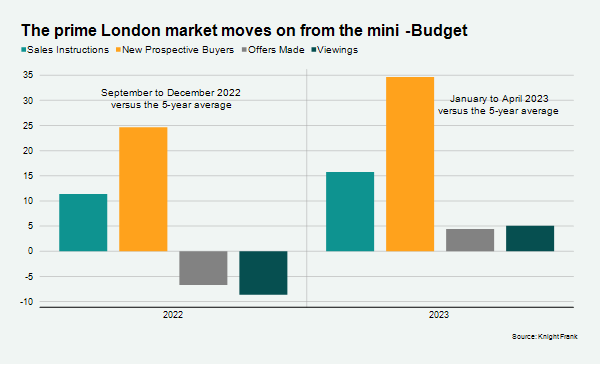

Demand is robust, with the number of new prospective buyers 35% above the five-year average in the first four months of this year, excluding 2020.

Supply is also picking up and the number of sales instructions was 16% higher over the same period, which helped push the number of exchanges up by 8%.

London has benefitted as demand gravitates back towards the capital following the pandemic. Prime markets have also been buoyed the return of international travel, a relatively weak pound, and the fact average prices in prime central London (PCL) are still 15% below their last peak in mid-2015. In prime outer London (POL), the equivalent drop is 7%.

Transaction activity was particularly strong in higher price brackets, with the number of exchanges above £5 million up by 40% over the same period. Below £2 million, there was a 3% decline.

Higher levels of cash sales, housing equity and affluence mean that buyers and sellers inside zone 1 have been more immune from the volatility in mortgage rates that followed the mini-Budget.

But lower-value markets are performing more strongly than most anticipated despite the fact mortgage rates are more than double the level of two years ago. A strong jobs market, accumulated lockdown savings and readjusted price expectations have all played their part.

The bottom line is that the market is experiencing a robust period of activity as confidence returns following a chaotic end to 2022. The number of offers made and viewings are also picking up, as the chart shows.

By way of comparison, the number of new prospective buyers outside the capital was down by 7% over the same period in 2023 and viewings were 9% lower as the ‘race for space’ slows down.

How long will it last in London?

On the one hand, the economic backdrop is broadly improving. Inflation has reduced to single-digits and the IMF has become the latest organisation to revise away its predictions of a recession. However, upwards pressure on rates in the face of higher-than-expected inflation means more financial pain will enter the system.

Average prices in PCL were again broadly flat, falling 0.1% in the year to May. In POL, there was an increase of 1.4%.

Political risks are also rising as housing becomes a key battleground ahead of next year’s general election.

Proposals being floated by the Labour Party include higher stamp duty for overseas buyers and limits on international sales for new UK developments. The latter is a policy followed by London Mayor Sadiq Khan, but one that lives alongside the reality that some schemes are forward-funded by overseas sales.

Overseas home ownership is less than 1% across the UK and in varying degrees of single-digits across London, according to the Centre For London think tank. Will higher stamp duty for international buyers reduce house price inflation across the capital? With an election around the corner, the answer doesn’t really matter.

We are not at the stage yet when politics is more of a concern than what is happening in the economy or lending market, but it will happen at some point over the next 12-18 months.