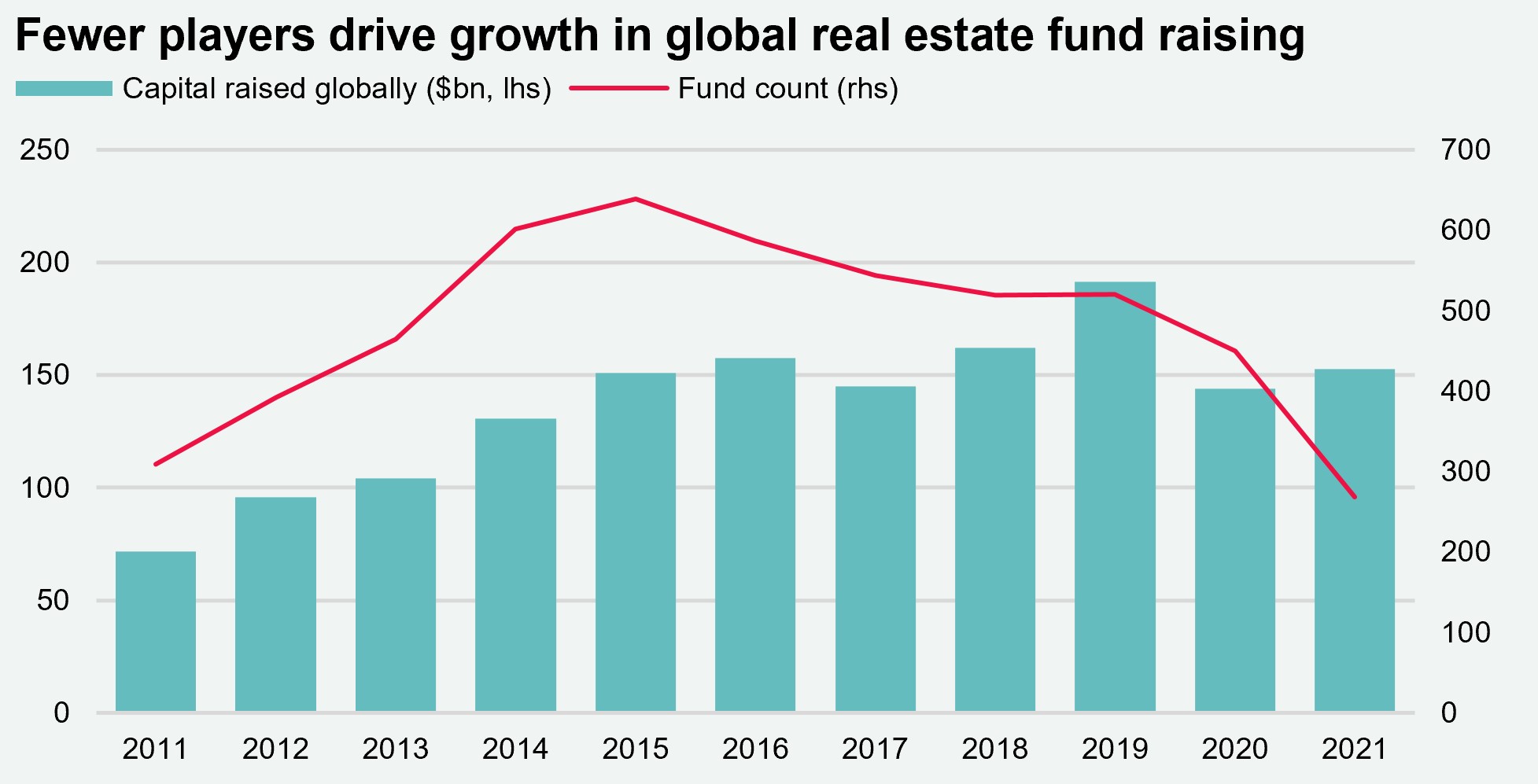

Interest rates on the rise, portfolios realigned, and the ongoing Covid impact

Discover key economic and financial metrics, and what to look out for in the week ahead.

1 minute to read

Here we look at the leading indicators in the world of economics. Download the dashboard for in-depth analysis into commodities, trade, equities and more.

Central banks: onwards and upwards

The Bank of England and US Federal Reserve meet later this week and markets are expecting a 25bps rate rise from both. This follows last week’s unexpected decision by the European Central Bank to accelerate the tapering of its asset purchasing scheme. Short-term inflationary pressures continue to build, with some market commentators expecting UK CPI will reach 9.5% by October. Despite this we believe central bank rate rises will top out during 2023, after relatively modest increases, with limited direct impact on property yields.

Investors realign portfolios to capture higher returns

$230bn of inflows from government bonds into equities are expected to occur this month, as institutional investors seek to meet their asset allocation strategies by the end of the fiscal year. With investors’ cash holdings now rising to levels above those reached in March 2020 (when pandemic uncertainty resulted in a flight to liquidity), we could see some turn to real estate in search of a less volatile, income producing asset class, which in some cases can act as an inflation hedge.

Covid still a risk to global growth

While some territories including Japan and Western Australia have relaxed border restrictions for the first time since April 2020, some 17.5 million people in China are facing renewed lockdown measures. In particular, the city of Shenzhen, which is a large manufacturing hub, has closed its factories as mandatory stay at home orders have been implemented. While these restrictions are only in place until 20th March, this could have global implications for supply chains, adding to inflationary pressures around the world.

Download the latest dashboard