Subdued Spring in Prime London Market as Mortgage Rates Rise

April 2024 PCL sales index: 5,301.4

April 2024 POL sales index: 273.6

3 minutes to read

The seasonal spring bounce in the UK housing market looks a little lacklustre.

Admittedly, the number of UK mortgage approvals hit an 18-month high in March, but the figure has only inched higher in recent months and transaction volumes are still a quarter below their five-year average.

Furthermore, the Nationwide said annual price growth narrowed to 0.6% in April, meaning ‘house price fall’ headlines will only gather momentum.

The outlook isn’t exactly gloomy, but neither does the warmer weather signal lift-off for the market.

The primary cause is stubborn services inflation, which means rate cut expectations have moved further into the distance since January, as we explored here. Money markets are currently pricing in between one and two cuts in 2024 and lenders have been forced to raise rates.

Despite the greater proportion of cash buyers (historically half of sales inside zone 1), prime London markets have not been immune to the pervading mood of hesitancy.

Annual price growth in prime central London fell to -2.6% in April, which was the lowest figure in three years.

Needs-driven markets are performing better as rates edge higher, as we explored last month. As a result, the annual price decline in prime outer London narrowed to -1.2% in April.

It followed a quarterly increase of 0.4%, which was the highest in 18 months. Wandsworth (4%) and Dulwich (3%) were the strongest-performing areas in London over the last 12 months.

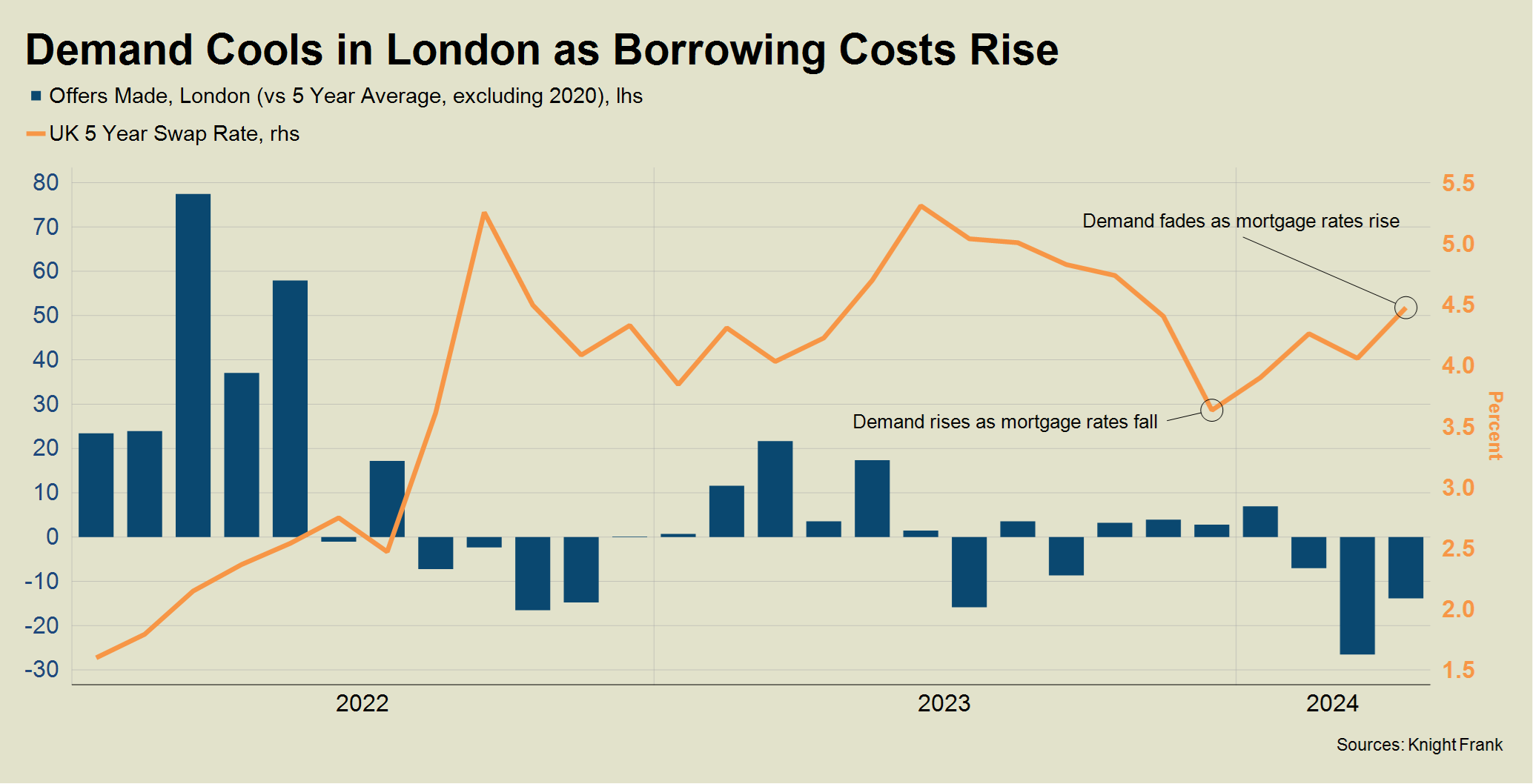

The close relationship between the cost of borrowing and demand in recent months is evident across the whole of London, as the chart shows.

The number of offers made was 14% below the five-year average (excluding 2020) in April, underlining how demand has weakened.

Meanwhile, the five-year swap rate ended last month at close to 4.5% after spending most of January under 4%. Lenders set the rate for fixed-rate mortgages based on the swap market.

The poor weather since the Easter holiday won’t have helped much, but if you want to take the pulse of the housing market, your mortgage broker is a good place to start.

The bad news for buyers and anyone re-mortgaging is that the prospect of a May rate cut feels remote. Meanwhile, the question of whether we see one in June has divided the opinion of economists.

Should services inflation fall by more than expected when the data is next published on 22 May, there would be downwards pressure on lending rates and the spring bounce would feel more palpable. Admittedly, it doesn’t feel like the most likely scenario, for reasons explored here.

The better news is that supply has risen in recent months, which means it has a better chance of meeting demand when the latter eventually picks up.

The number of sales instructions in London in April was 21% higher than the five-year average (excluding 2020), having risen by 10% over the first four months of the year.

As we saw in January, the market can turn quickly when mortgage rates begin to fall. If there is better news on inflation towards the summer and lending costs start to fall, buyers will need to remain alert from the comfort of their sunbeds.