Rising mortgage rates: this time it's different

Making sense of the latest trends in property and economics from around the globe

3 minutes to read

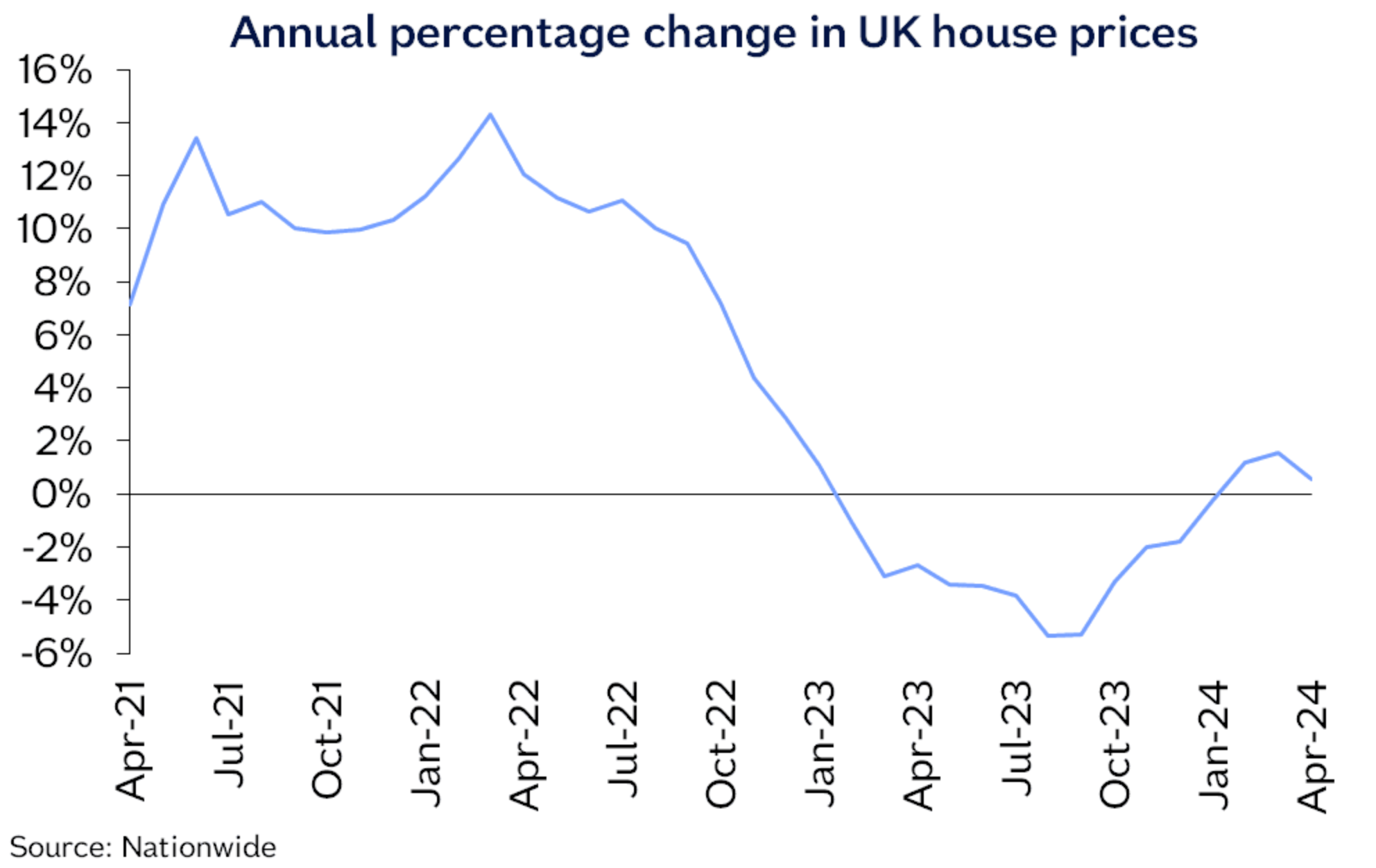

UK house prices fell 0.4% in April, Nationwide reported this morning. That follows a 0.2% decline in March and trims the annual rate of growth to 0.6%.

Rising mortgage rates put a stop to the new year rally in property values. The latest indicators suggest that activity is still rising, driven largely by people who need to move, but buyers must now account for the fact that typical two-year fixed rate mortgages sit north of 4.5%.

House prices are now about 4% below the all-time high recorded in the summer of 2022.

Mortgage rates

It's been a tricky ten days or so for borrowers. About thirty banks raised rates last week. Natwest, Nationwide and Santander hiked by up to 0.25% yesterday.

Journalists have asked us why this uptick in mortgage rates is any different from the one in late-2022 that followed the mini-budget, but there are several important differences. The high street price war at the start of the year meant lenders were operating on wafer thin margins, which has left them vulnerable to the kind of moves in swap rates we've seen in recent weeks.

“We are now talking about a slower and potentially shallower cycle of interest rate cuts from the Bank of England, rather than a dramatic shift," Hina Bhudia of Knight Frank Finance tells the Times. "It will squeeze the recovery in mortgage rates rather than eliminate it entirely.”

Paul Dales, chief economist at Capital Economics, shares that view: "Our own forecast is that inflation will fall fairly fast and that Bank rate will be reduced to around 4% by the end of the year," he tells the paper. "If we are right, then market rate expectations will fall again, swap rates will decline and mortgage rates will drop back.”

Lending volumes

Net mortgage approvals for house purchases rose to 61,300 in March, from 60,500 the previous month, the Bank of England reported yesterday. That's the highest number of net approvals since September 2022.

We are steadily approaching the 65,000 or so net approvals that we were seeing every month during the three years leading up to the pandemic, though there are good reasons to believe that these figures will soon plateau until rate cuts come into view.

Huw Pill, the Bank of England's chief economist outlined last week why he believes there are greater risks in cutting too early, rather than too late, and it's clear that some policymakers need a lot more evidence that domestic inflation is beaten, and to a lesser degree some clarity as to how the Federal Reserve will behave during the months ahead.

Federal Reserve officials will almost certainly hold interest rates steady when the latest decision is published later today. Economists expect Fed chair Jerome Powell to confirm that any plans to cut rates are on hold until the inflation data starts improving.

Power shortages

A third of developers across the country say the progress of their housing schemes has been impacted by National Grid power constraints, according to our latest quarterly survey of 50 volume and SME housebuilders.

Around 15,000 of their new homes are currently held up by a lack of grid connections. Our poll of 50 housebuilders and developers together build 70,000 homes across England each year.

UK housing supply is already constrained by multiple factors, but power shortages have emerged this quarter as a key concern in our survey. This situation has emerged at a critical point for the sector: the number of new homes coming forward in England is falling, particularly in London where build costs are higher. Historically, the number of homes receiving planning permission has always trended a healthy distance above completions. You can read more from Anna Ward here.

In other news...

Grosvenor bets on hybrid working (FT), first-quarter growth eases fears of eurozone ‘stagflation’ (Times), and finally, Europe's biggest smart city rises in Greece (Bloomberg).