The battle for Asia's wealthy families

Making sense of the latest trends in property and economics from around the globe.

4 minutes to read

Heat pumps

The UK's transition to heat pumps faces a series of obstacles. There aren't enough trained installers, for example, and policy ambiguity is preventing manufacturers from backing the technology wholeheartedly. But even if we could sort those out, how do you make people actually want heat pumps?

Cost is often cited as the biggest obstacle, so either energy bills for competing systems climb high enough to act as an incentive, or the government introduces subsidies to bring heat pump costs down.

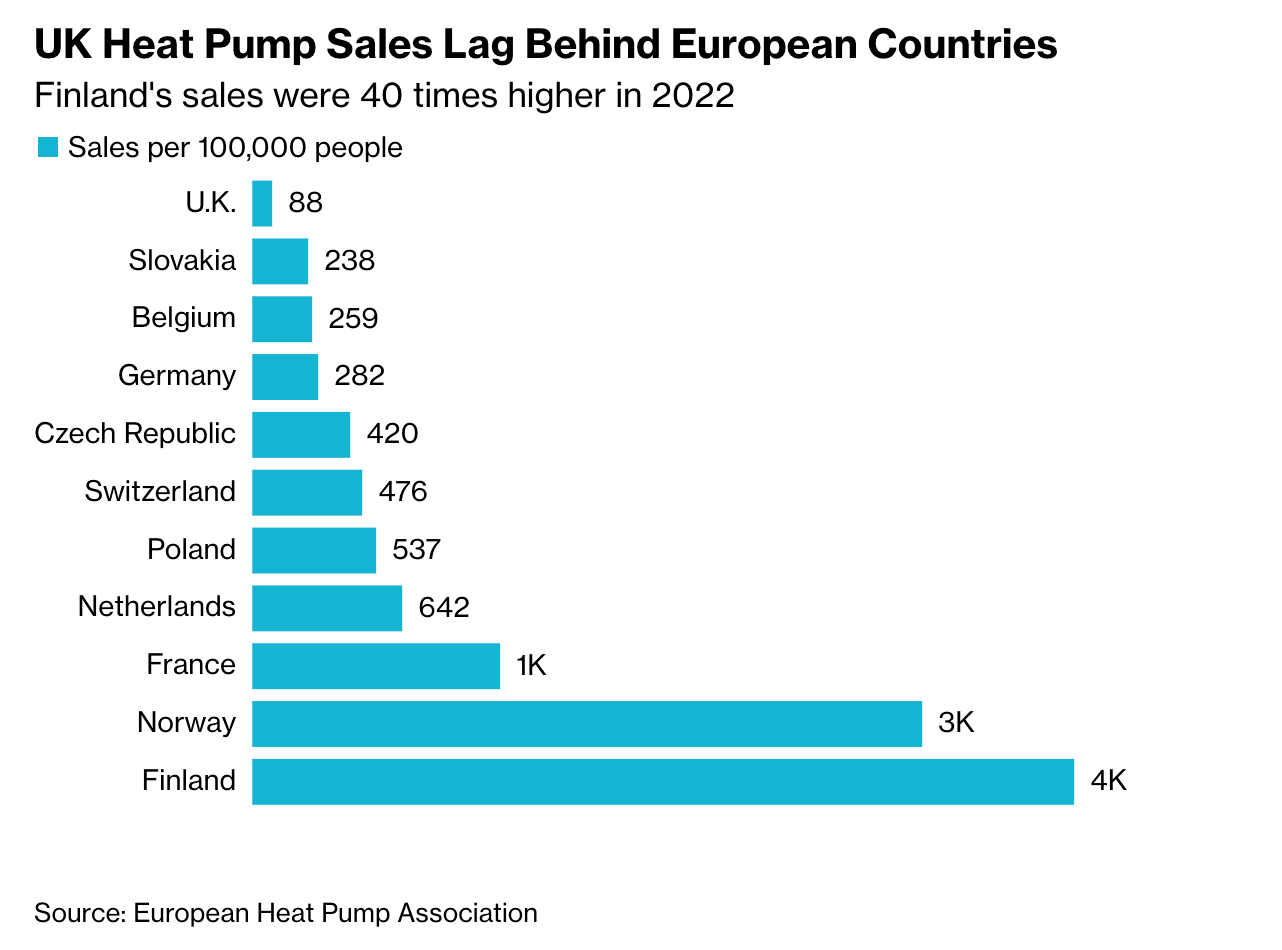

The UK is lagging behind other European nations when it comes to heat pump installations, according to figures published last week by the Energy and Climate Intelligence Unit think tank (see chart from Bloomberg). Finland has sold more than 40 times as many heat pumps per 100,000 people than the UK. Its transition, like that of other Scandinavian nations, has been light on subsidies and has largely relied on consumers stumping up their own cash. France, a relative newcomer to the market, has increased installations 12-fold compared with Britain. It took the other route by ending subsidies for installing fossil-fuel-fired heaters while meaningfully boosting funding for heat pumps.

Mission zero

UK "consumers’ exposure to high fossil fuel prices has created a window to encourage even faster decarbonisation," the government's climate watchdog flagged last year. There exists "the potential to push harder, in particular on energy efficiency and heat pump roll-out in the buildings sector. It is important that efforts to ameliorate consumer costs do not entrench existing use of fossil fuels."

That report arrived in the midst of an energy crisis that has since eased to a degree. Typical annual energy bills are now forecast to be £2,400 next year (2023-24), down from the forecast of £3,000 at the time of the Autumn Budget, the Resolution Foundation calculated in February. Has the opportunity already been missed?

Perhaps, which leaves a substantial government intervention as the other option. Granted, the government has pledged £450 million to assist consumers seeking to upgrade natural gas boilers to heat pumps, but it's still a long way short of recommendations published in January by the government's net zero tsar Chris Skidmore. Mr Skidmore wants the government to "urgently" adopt a 10-year mission to make heat pumps a widespread technology in the UK and regulate now for the end of new and replacement gas boilers by 2033 at the latest. The government's response to that report is due out before the end of the month, Mr Skidmore said last week.

Private capital in Asia

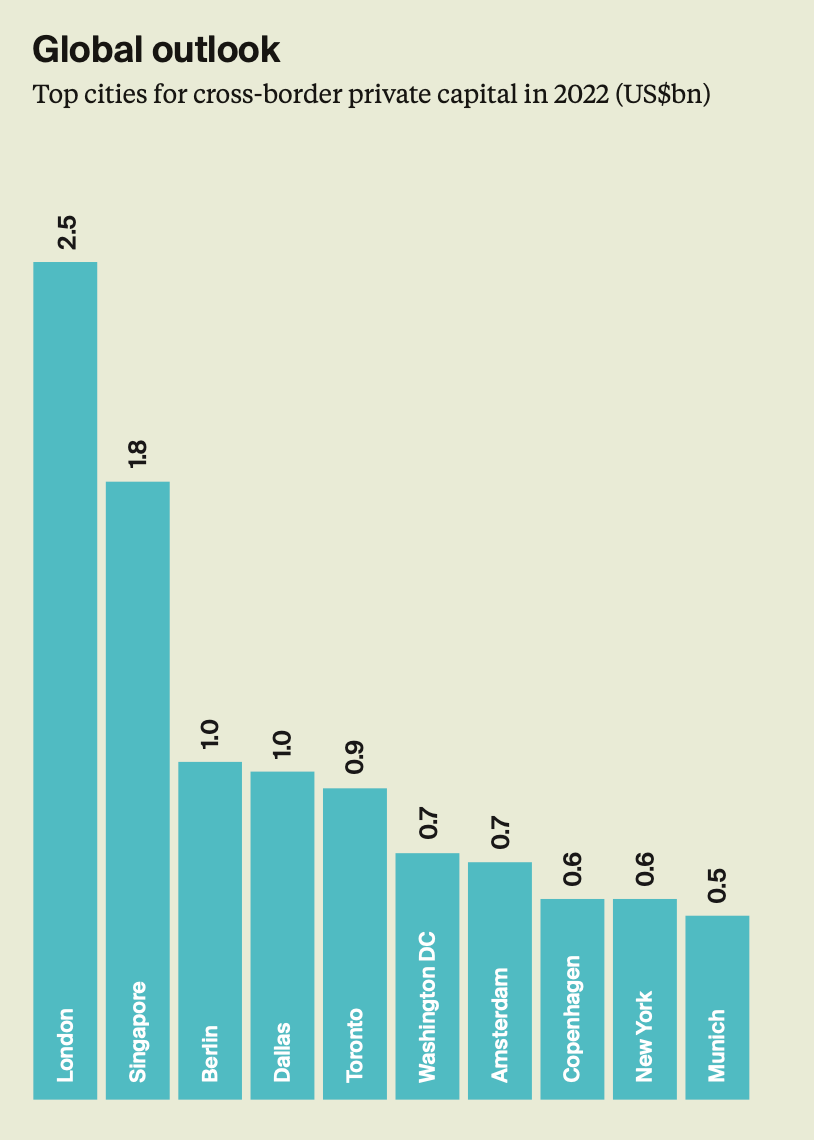

Singapore is now several years into the development of a tax and regulatory framework aimed at making it Asia's leading hub for private capital. So far it's working. As we revealed in The Wealth Report 2023, the city-state has enjoyed sevenfold growth in the number of family offices and secured US$1.8bn in cross-border private capital last year, second only to London.

Hong Kong responded on Friday with plans for a raft of tax cuts aimed at wealthy families. Those plans will include a relaunch of its capital investment entrant scheme - though reporting so far has suggested that investment requirements will be 'multiples' of the old HK$10 million threshold for a similar programme suspended eight years ago.

Mortgage rates

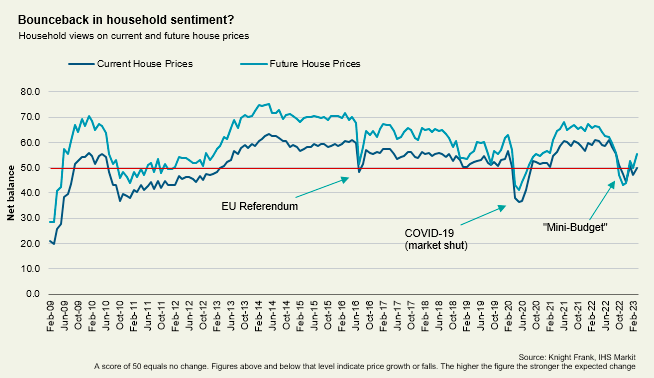

The Bank of England's decision to raise the base rate to 4.25% is unlikely to dampen buyer demand, which is proving more resilient than expected against an improving economic backdrop, Tom Bill writes in his weekly update this morning. Indeed, the latest survey from IHS Markit out late last week suggests that sentiment continues to improve (see chart).

We talked on Friday about uncertainty over the path of mortgage rates. Spreads between mortgage rates and banks' cost of funding has been narrowing since the mini-budget. That narrowing accelerated amid the recent turmoil in the banking sector. The BoE said it was yet to see clear signs that the recent increase in bank funding costs is feeding through to mortgage rates, but it's still early days.

There have been small moves in mortgage rates in either direction in recent days - a trend that is likely to continue for now, according to Simon Gammon of Knight Frank Finance (see Tom's update linked above for more):

“Rates should fall in the longer-term but until we get to the point where inflation and the bank rate have clearly peaked, I suspect lenders will keep tip-toeing up and down with their rates depending how confident they are feeling at the time.”

In other news...

Commercial property risks rise up bank investors’ worry list (FT), IMF urges ‘vigilance’ as it warns over increased financial stability risks (Telegraph), and finally, buyers look beyond big-name resorts to get around Swiss restrictions (FT).