Green shoots emerging in new homes and land markets

Plus, the Living Sectors shine and how many homes can be built on brownfield sites in London?

4 minutes to read

The improved outlook for interest rates has underpinned a busy start to 2024 for the new homes market.

In January, the number of prospective buyers registering their interest in purchasing a new home in London climbed 9% compared with the same month a year earlier and was up by more than 50% compared to 2019, before the pandemic, Knight Frank figures show.

A pick-up in new enquiries chimes with other market data. The latest RICS monthly market survey of estate agents shows that new buyer enquires turned positive for the first time since April 2022. The agreed sales indicator also hit a 32-month high.

So, what is driving this shift in sentiment?

Much of it comes down to stability. Mortgage rates are lower than they were six months ago and, despite edging up in the last week, are forecast to fall over the medium term. The suggestion is that many potential buyers are dusting off plans on the back of the improved outlook. With that in mind, the early part of 2024 could offer a period of relative stability for buyers.

Outlook improves in land market

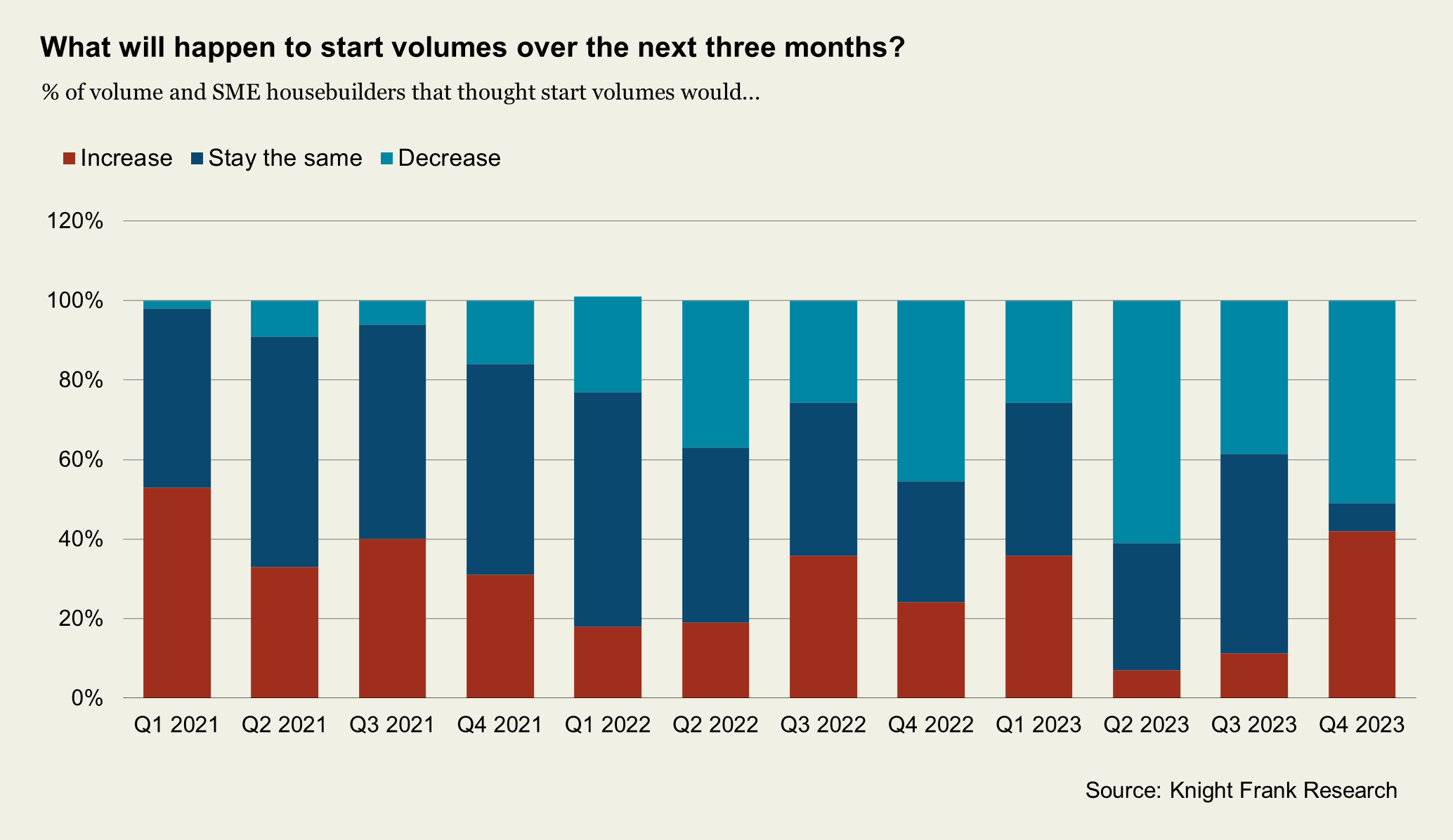

One group that will be watching the performance of the sales market closely are the volume and SME housebuilders. Each quarter we survey 50 of them as part of our Residential Development Land Index. The latest results point to a welcome improvement in site visits and reservations.

Other indicators have also improved. Some 40% of respondents said they expect new starts will rise this year, up from just 12% the previous quarter. This was the highest such reading since early 2021.

Admittedly, any improvement will come from a low base; the latest data suggests housing starts slumped to their lowest level since 2009 in Q3 last year. But the reading does suggest we are at a turning point. That should support a more active land market in 2024, particularly as buyer and seller expectations for land prices align.

Housing policy takes centre stage

All signs point to housing being a central issue in the run-up to the next general election. This month the Housing Secretary, Michael Gove, put forward several proposals designed to boost new supply.

One of the key proposals is that the planning system should tilt in favour of approving applications for homes on brownfield sites in England’s 20 largest urban centres, if local housing targets have not already been met.

There are questions over whether this approach will deliver the right homes in the right places, or in the volume required. There is also a limit to what the government can do to support a sector that is largely demand-led, a key conclusion of the CMA’s recent year-long study into housebuilding.

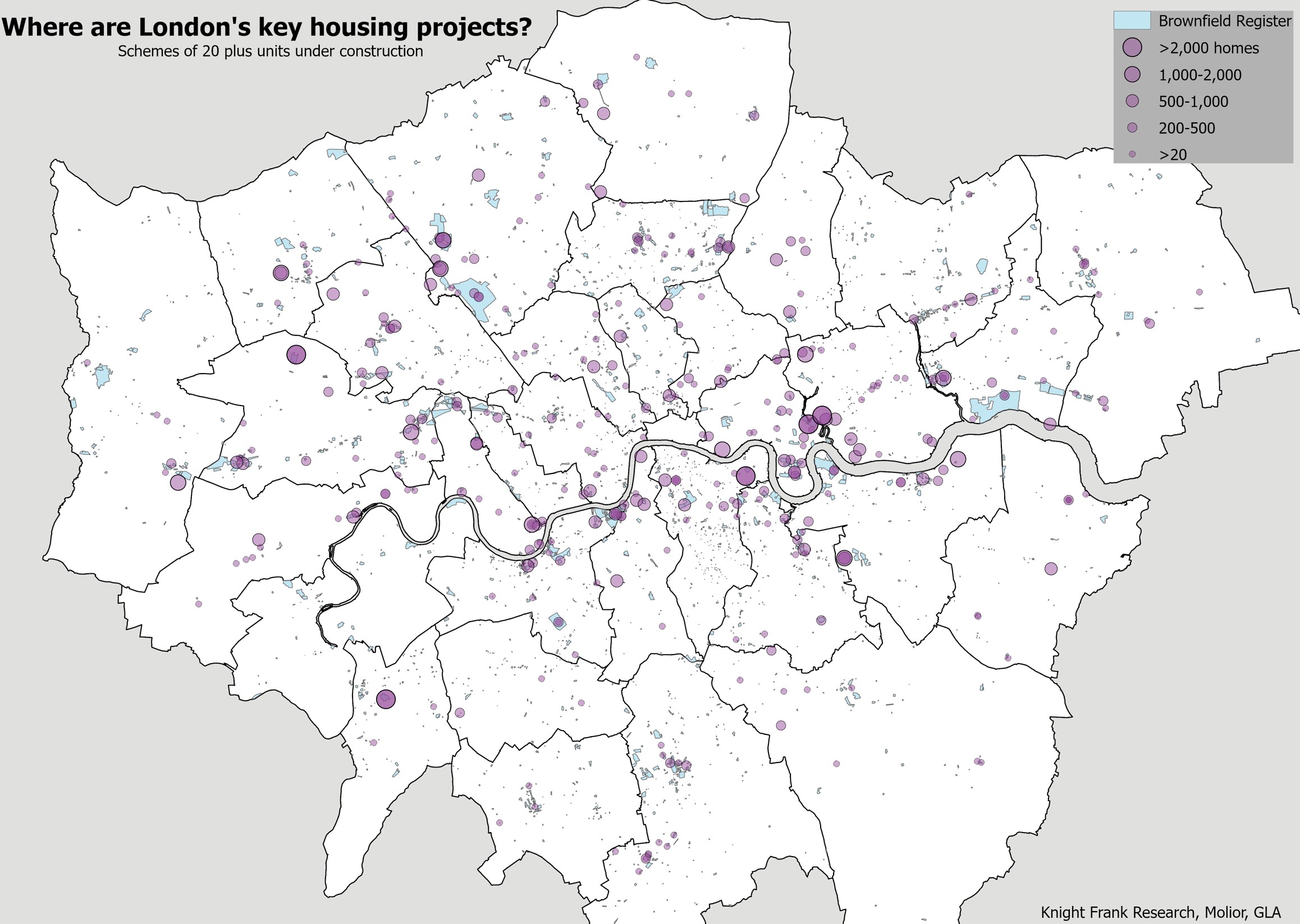

Anna Ward has taken a deeper dive into the scale of the brownfield opportunity, focusing first on London. Analysis of sites capable of providing at least 50 dwellings from the London Brownfield Land Register shows there is potential capacity for 160,000 homes in inner London. Strip out sites already with planning or under construction though and that does not leave much spare capacity for new homes.

Living sectors continue to shine

Investor interest in the Living Sectors shows no sign of waning, thanks to a combination of predictable demographic drivers, secure income streams and ongoing strong rental growth.

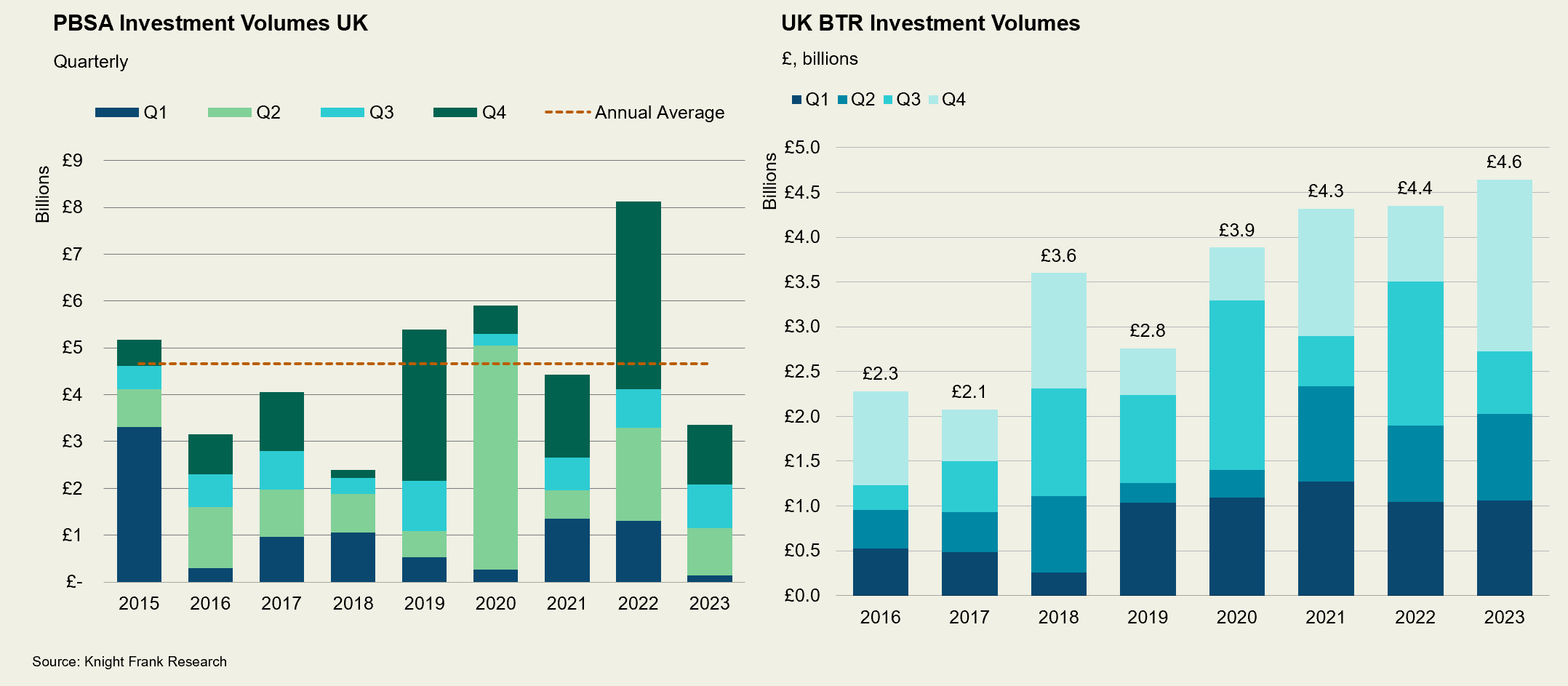

Investors spent £4.6 billion on UK Build to Rent (BTR) assets during the year, boosted by a £1.9 billion splurge in the final quarter, according to Knight Frank figures. Investors spent £1.9 billion on Single Family Housing (SFH) during the year, bringing the sector to a little more than 40% of total volumes.

A bumper Q4 and an improving macroeconomic backdrop set the scene for a strong BTR investment market in 2024. Those who have been ‘waiting in the wings’ are becoming active again and we expect there will be increased competition for limited investment opportunities.

In the Student sector, full year investment volumes hit £3.35 billion. Investment was spread over 57 transactions, slightly above the five-year annual average of 55 deals a year.

The performance of Purpose-Built Student accommodation (PBSA) as an asset class in 2024 will continue to be underpinned by the same theme: a structural imbalance between supply and demand for accommodation. Our expectation is that transactional volumes will exceed £4 billion this year.