UK residential property market continues to defy gravity

Knight Frank's Monthly UK Residential Market Update provides a snapshot of the health of the UK housing market, assessing its performance, and proving analysis of the latest economic developments

3 minutes to read

While the world waits to gauge the impact of the Omicron variant of Covid-19, the UK residential property market continued to experience its own supply-chain disruptions in November.

RICS described a ‘dearth of new instructions holding back activity’ in its latest sentiment survey. A net balance of +13% of survey respondents reported an increase in new buyer enquiries during November, compared to +11% in October. However, a net balance of -18% of respondents noted a further deterioration in new instructions for sale, which was the eighth consecutive decline.

With supply remaining so tight, prices continue to defy gravity. Nationwide recorded UK annual house price growth of 10% in November.

Halifax data for the month shows the same trend, with quarterly growth at a 15-year high of 3.3%.

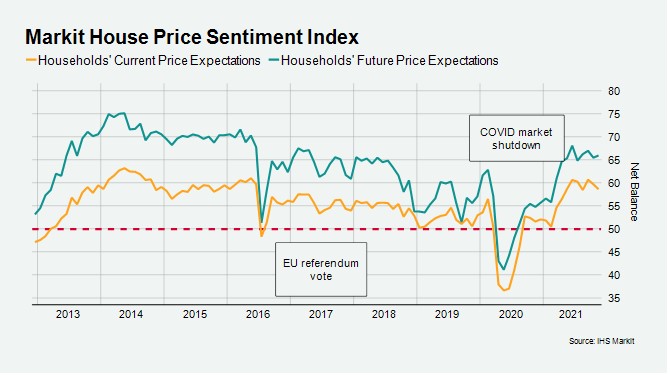

Sentiment around the future trajectory of prices remained well above pre-pandemic levels in November, as the chart below shows. It will be interesting to see how this changes in December as the Omicron news unfolds.

There were 76,930 UK transactions in October, down 52% on 160,220 in September, which marked the end of the stamp duty holiday. The distortions of the stamp duty holiday also meant that net mortgage borrowing fell to £1.6 billion in October from £9.3 billion in September.

Meanwhile, in a sign of how the economy is shrugging off the end of the furlough scheme, the unemployment rate fell to 4.2% in the three months to October. Along with lingering Omicron uncertainty, the Bank of England took this into account at its meeting in December and made the decision to raise interest rates for the first time in more than three years.

The increase in the bank rate from a historic low of 0.1% to 0.25% is in reaction to surging inflation, which hit 5.1% in December, and you can read our initial thoughts here.

Further increases in the base rate are expected in 2022. The initial increase is likely to have limited impact on the housing market, with UK Finance stating that 74% of mortgages are currently on a fixed rate.

Prime London Sales

The number of offers accepted in November reached a ten-year high as the capital moved firmly back onto the radar of buyers.

In prime central London, the figure was 116% higher than the same month last year while in prime outer London, there was a 25% increase on last November.

It is indicative of how demand has shifted back towards London as the pandemic has evolved. Across the UK, the biggest increases in the number of new prospective buyers in the three months to November compared to last year were all in London, recent analysis shows.

Prime London Sales Report: December

Prime London Lettings

Rental values continued their strong recovery in November, pushing the annual change into positive territory in some parts of London for the first time since early 2020.

Average rents rose 5.3% in the three months to November in prime central London (PCL) while there was an increase of 5.1% over the same period in prime outer London (POL).

It was the largest quarterly gain in POL since March 2004 and the biggest such increase in PCL since September 2010 as the lettings market continued to recover from the pandemic.

Prime London Lettings Report: December

Country Market

In November, the number of properties for sale on the market was 56% below November 2019, a consequence of high demand throughout 2021 and some owners choosing to hold off during the stamp duty holiday frenzy due to a lack of purchase options.

New listings typically surge in the spring and there are positive signs that sellers are already planning their return next year.

Market valuation appraisals for sale were at their highest level for the month of November in more than ten years, suggesting that subject to further Covid restrictions, sellers plan to make the most of a strong market early next year.