Impact of cheaper mortgages may eclipse house price declines

The effect will be more marked for those with higher loan-to-value ratios

3 minutes to read

Staying close to a mortgage broker will be an important part of timing a house purchase correctly in 2023, as we explored last week.

Mortgage rates will fall as the shock of the mini-Budget works its way through the system and the potential savings for buyers will increase.

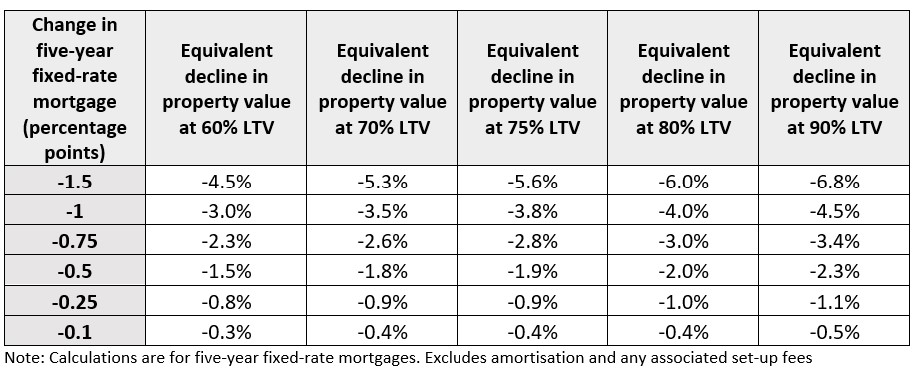

There will be more at stake for those who agree deals at a higher loan-to-value (LTV) ratio, a group that will include more first-time-buyers and younger owners, new data shows.

For anyone seeking a five-year fixed-rate mortgage at an LTV of 90%, a decline of 1 percentage point on the rate (for example from 6% to 5%) is the equivalent of 4.5% of the property’s value.

Based on a property worth £500,000, a 90% mortgage would require a loan of £450,000. A decline of one percentage point would equate to £4,500 per year or £22,500 over the period of the five-year fix, a sum that represents 4.5% of the £500,000 value. The figures would differ slightly if amortisation was taken into account, depending on the overall length of the mortgage.

At an LTV ratio of 60%, the equivalent saving on the mortgage rate would equate to 3% of the property’s value, as the table shows.

Even as the percentages get smaller, the sums involved are still notable. For example, a 0.1 percentage point reduction at an LTV of 70% is a saving of £2,625 over five years on a £750,000 property, which is money most people would rather direct elsewhere.

For anyone attempting to buy at the right time this year, they can operate with more precision by monitoring the mortgage market.

Although UK house prices are expected to fall this year, waiting for the bottom is an unrealistic proposition for some buyers and an inexact science for anyone attempting it.

Many people are driven by need when they move so the scope for timing can be limited. And for those attempting to read the runes of the latest house price data, what is happening at a national or a regional level won’t necessarily tell you very much about what is happening on your street in a hyper-localised market like housing.

For example, prices for the most in-demand properties tend to be resilient whatever is happening in the wider economy.

Neither is getting your timing right straightforward in a relatively slow-moving market like residential property. It means the fabled “bottom of the market” is often only visible in the rear-view mirror, a time when the fear of missing out means that demand and upwards price pressure can rise sharply.

Not that we expect the bottom to be reached this year. We forecast that prices will fall by 5% in 2023 as more people come off relatively lower fixed-rate deals, a process that will last into next year, as confirmed by government data released this month.

Keeping an eye on mortgage rates could prove just as useful for sellers. Owners who secure a better rate on the property they are buying may more readily absorb an equivalent discount on the one they are selling.

The broader trajectory for prices and sentiment should become clearer after sellers’ expectations are more fully put to the test this spring.

That said, a cumulative 10% decline over the next two years would only take prices back to where they were in the middle of 2021. Furthermore, we expect single-digit annual price growth to return from 2025.

Waiting too long for the perfect moment to strike carries its own risks.