China's turning point?

Your international property and economics update tracking, analysing and forecasting trends from around the world.

4 minutes to read

China

This week, China’s property sector received a shot in the arm as policymakers announced a 16-point plan to relieve the country’s credit crunch. This follows a lengthy period when strict curbs on property developers put a halt to overborrowing in light of the Evergrande debacle and stalled construction.

Adjustments have also been made to China’s zero-Covid policies to make them less onerous. Taken together, The Economist considers the joint move “the biggest shift in Chinese policymaking in years.”

Whilst property speculation is still frowned upon as President Jinping continues his mission towards ‘common prosperity’, access to finance is set to loosen with down payments reduced. Developers’ loans are to be extended, state-run banks will help finance stalled housing projects, and lenders will show greater flexibility to those with mortgages on unfinished schemes.

Investors welcomed the news with shares in Chinese developers increasing but buyer confidence will be the key factor. If buyers remain unconvinced that the apartment they plan to buy will be built and economic growth stalls due to further lockdowns, the market may struggle to gain traction.

Ski homes

In 2022, the price of a ski chalet across the French, Swiss and Austrian Alps increased at its fastest rate for eight years.

Knight Frank’s annual Ski Property Index which tracks 23 top ski destinations across the Alps reveals that prime prices increased 5.8% in 2022, up from 4.6% the previous year.

It’s no secret that ski homes were in the spotlight during the pandemic as we witnessed a move to hybrid working, a rekindled love of the great outdoors and heightened interest in health and wellbeing.

But, what’s surprising is that demand and prices continued to strengthen last year despite the fact that we saw a third year of interruptions due to travel restrictions, and economic clouds mounting on the horizon.

The Swiss resorts of Crans-Montana and St Moritz led the annual rankings, both registering annual price growth of 14% in the year to June 2022.

A lack of supply and the increasing pull of year-round resorts, which offer a broad a range of activities in the summer months, explain both resorts’ outperformance.

But the mood is shifting. Whilst the high proportion of cash buyers in the Alps will mean they are less exposed to the rising mortgage costs; the sector will face headwinds and the rate of price growth is expected to moderate after the exuberant pandemic years.

This year’s Ski Property Report, our 14th edition, also includes the results of our first Ski Sentiment Survey and a roundup of the latest market trends in Colorado’s top resorts of Aspen and Snowmass.

Prime prices

The rate of prime price growth across 45 cities around the world slowed for the second consecutive quarter in Q3 2022.

At first glance, the annual performance of our latest Prime Global Cities Index looks robust with price growth averaging 7.5% year-on-year, but a deeper dive confirms that markets are cooling on a quarterly basis.

Of the 45 cities tracked, 19 saw prime prices decline between June and September 2022, up from seven in Q1 2022.

Those markets that registered some of the largest falls also equate to those cities that saw some of the strongest price rises during the pandemic: San Francisco, Toronto, Wellington, Stockholm, Vancouver, Los Angeles and Seoul, as well as some Chinese mainland cities.

View the full city rankings here.

Tracking the slowdown

It is clear property markets globally are set for an extended period of instability and insecurity.

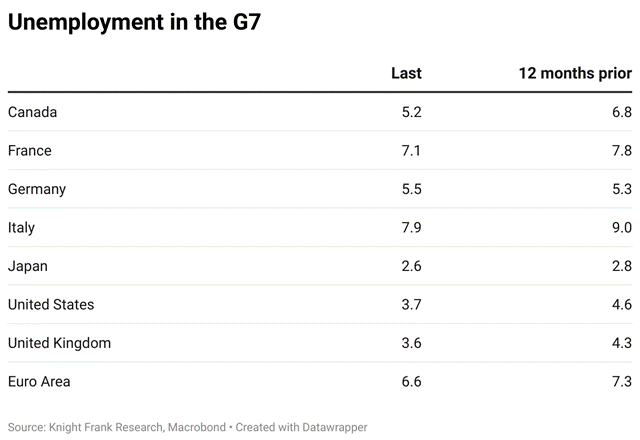

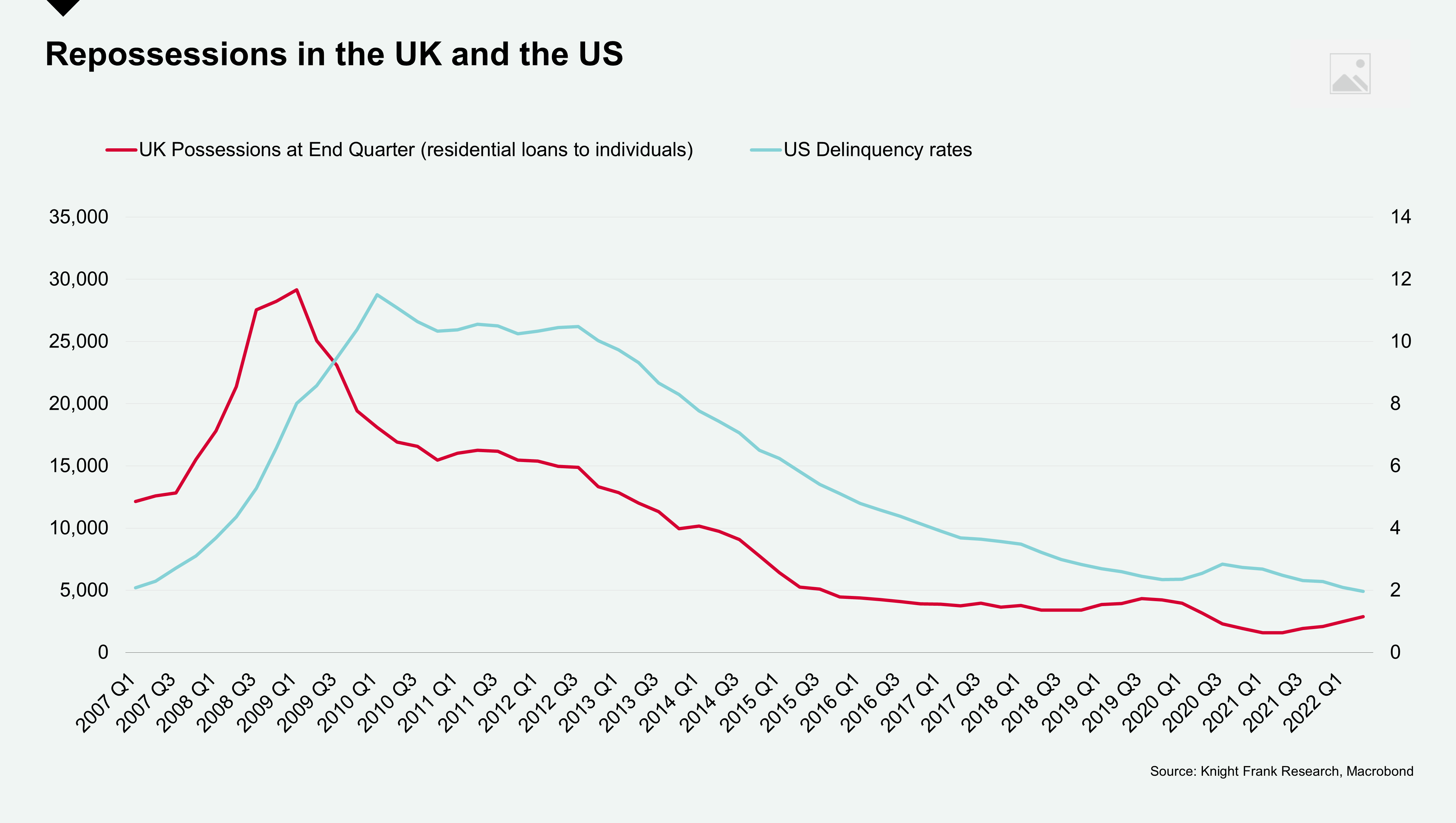

To gauge the scale and longevity of the slowdown as well as its regional variations, we are tracking a range of live datasets from unemployment rates to repossessions and consumer sentiment.

A quick look at some of the key indicators reveals relative resilience. Unemployment has decreased year-on-year in all but one of the G7 members, Germany being the exception.

And despite UK repossessions starting to rise, numbers in both the US and UK remain significantly lower than during the GFC.

While risks are firmly titled to the downside, the IMF in its latest World Economic Outlook states, “This is the weakest growth profile since 2001 except for the global financial crisis and the acute phase of the Covid-19 pandemic,” there are several factors cushioning the downturn in prime markets globally:

• Safe haven flows emerging into tier 1 cities

• A lack of supply

• Resilient labour markets

• Currency shifts are influencing cross-border investment flows

• Household balance sheets are relatively robust due to accrued savings during Covid-19

• Fixed rate mortgages account for a larger market share in advanced economies than a decade ago

Plus, inflation in the US at least, may have peaked according to the latest CPI numbers published last week.

In other news...

A weak pound increases the need for action over expat pensions (International Investment), Luxury Manhattan property sales have had their best week since May (Mansion Global), Los Angeles votes on a mansion tax for homes above US$5 million (Bloomberg) and Singapore home sales hit 2.5 year low as cooling curbs begin to bite (SCMP)