A spring upswing

Making sense of the latest trends in property and economics from around the globe

4 minutes to read

Global businesses are being squeezed by higher debt costs, rising salaries and weakened consumer purchasing power. More than 6,500 companies have announced layoffs since 2023, largely from the banking and technology sectors.

Reducing headcount is one way to cut costs, but offshoring services offers an increasingly compelling alternative. Technological advances and a booming pipeline of talent, particularly from Asia-Pacific nations, is driving more and more companies to consider moving services overseas, according to our new Asia-Pacific Horizon report. The global offshoring market is predicted to grow from US$245.9 billion in 2022 to US$544.8 billion in 2032, reflecting an 8.5% compound annual growth rate (CAGR).

India has long been among the first ports of call. Global Capability Centres accounted for 35% of all Indian leasing transactions last year, up from 10% in 2022, for example. However, relative newcomers are beginning to command a larger share of the market, particularly the Philippines, Malaysia and Vietnam. See the report for more.

The turn

The improved outlook for inflation enabled the high street lenders to lower mortgage rates through the early weeks of the year, paving the way for a busy spring. Half year results published by Bellway yesterday offered some clues as to how much trading conditions have improved.

In the six weeks since February 1st, the Bellway's private reservation rate increased by 20.7% to 163 per week, up from 135 during the same period a year earlier. That represents a private reservation rate per outlet per week of 0.67, up from 0.56. Given the improving outlook, the company has been more active in the land market since the start of the new calendar year. It had heads of terms agreed on 6,600 plots as of March 10th.

We expect these conditions to underpin a 3% rise in UK house prices this year and next, before gains pick up to 4% in 2026. That's despite increasing numbers of buyers rolling off sub-2% mortgage deals. The absorption of higher mortgage rates is a gradual process, which is part of the reason we expect pricing to remain so stable.

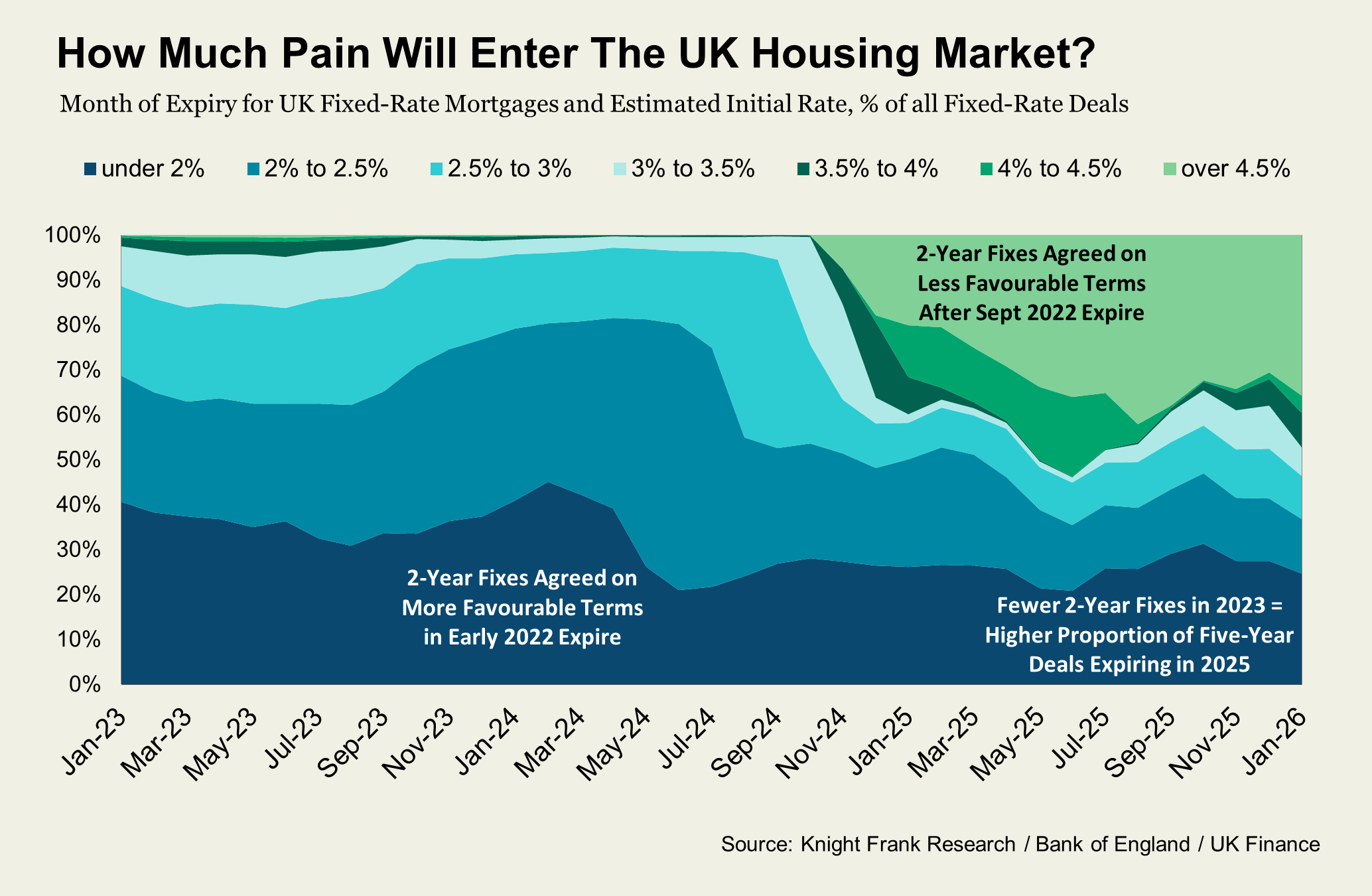

Tom Bill provided a detailed look at how many borrowers still face remortgaging yesterday (see chart). The proportion of all fixed-rate mortgages being renewed where the initial rate was less than 2% will fall from a peak of about 45% in February to approximately 26% by December. By the final months of 2024, the majority of sub-2% deals due for renewal will be five-year mortgages from 2019 (the rest will be three or four-year deals). Sub-2% five-year mortgages will disappear from mid-2027.

Affordability

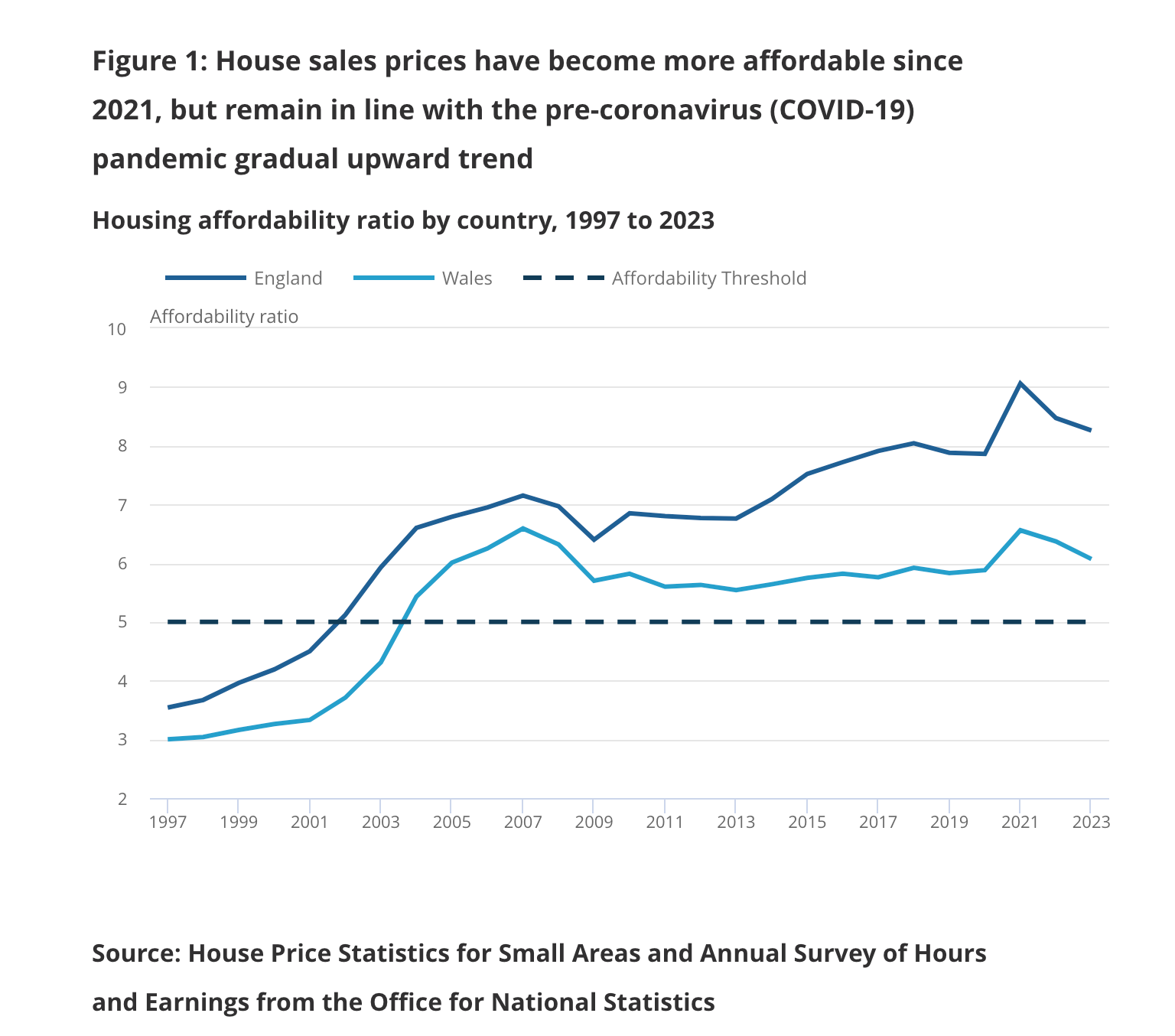

House prices fell 1.8% over the course of 2023, leaving them about 4.5% below the all-time high recorded in late summer 2022, according to Nationwide data. While those declines marginally improved affordability, full time employees in England can still expect to spend around 8.3 times their annual earnings buying a home, according to official figures published on Monday.

Affordability is now back in line with the pre pandemic trend line (see chart). It's a neat illustration of why the major political parties are finding it so difficult to make headway on a key issue for young voters. House prices have proved incredibly resilient and even a massive increase in housebuilding will do little to improve affordability. Raising a deposit is still the biggest barrier to ownership for many young people, which is why the conservatives were flirting with 99% mortgages.

The lenders are coming up with their own ideas. Yorkshire Building Society today said it plans to release a five-year fixed-rate deal that requires just a £5,000 deposit. It can be used to purchase properties worth up to £500,000. Borrowers can expect to pay 5.99%.

Sub-7% mortgages

In December, US borrowers were given a reprieve as the 30-year fixed rate mortgage fell below 7% for the first time since August 2023. Rates are still hovering a little below the 6.9% market, though both inventory and new construction are picking up in anticipation of rate cuts later this year.

Prices have so far displayed more resilience than sales volumes, according to Kate Everett-Allen's latest New York update. Luxury prices dipped 2% in 2023 with prime sales declining 28% in 2023 on an annual basis, according to data from our residential partners in the US, Miller Samuel and Douglas Elliman.

Where possible, buyers are opting to pay in case to avoid paying elevated mortgage rates. Of all Manhattan buyers, 68% paid cash for their home in the fourth quarter of 2023, up from 55% a year earlier.

In other news...

From our team - Stephen Springham on the mixed picture presented by the latest retail sales data, and Andrew Shirley on getting to grips with greenwashing.

UK businesses trim hiring and pay plans, Lloyds says (Reuters), Duke of Westminster’s property group launches £900mn lending arm (FT), US investment funds pull $13.3bn from BlackRock in anti-ESG campaign (FT), and finally, markets expect too many interest rate cuts, says BoE hawk (Times).