Offices - a new sense of purpose

Covid-19 led to the reprisal of the ‘death of the office’ narrative. Whilst this is misplaced, the post-pandemic period will see occupiers repurpose the office in three key ways.

5 minutes to read

Nearly two years into the black swan event of Covid-19, one word is dominating the post-pandemic narrative - purpose. The virus has led individuals and companies to question their purpose. In so doing, some of the mainstays and orthodoxies of pre-pandemic life are undergoing a fundamental re-evaluation. Whether it is the structure of the working week or day, the balance between work and personal life, the effect of our working lives on our mental and physical health, the sustainability of commuting, or the office as the central place of work, all are in the analytical spotlight. This is right, proper and has precedence. History shows that when we emerge from crises – be they political, economic or health-related - this process of reflection often occurs. History also suggests, however, that the result of such reflection is rarely as radical as initially assumed. Revolution tends to be avoided but so too does recidivism. What occurs instead is a process of accelerated evolution where change or re-purposing occurs with a greater pace and a more widespread application than would otherwise have been the case.

This dynamic is abundantly clear in the UK office market. The hyperbole and sensationalism of the mainstream press, who conflated a relatively short period of enforced working from home with the long-term death of the office, increasingly appears wide of the mark. While occupiers have naturally been slower to make real estate decisions, few have taken the knife to their occupied portfolios with anywhere near the ferocity feared in the early months of the crisis. Illustrating this point, just one fifth of global CEO’s surveyed by KPMG in August 2021 were planning to downsize their physical footprint, a stark contrast with the 70% who believed they would be making cuts a year prior. These results are consistent with those in the 2nd edition of Knight Frank’s (Y)OUR SPACE research. That is not to suggest, however, that the form, function or purpose of the office is not subject to change. Indeed, there are three key areas of office repurposing emerging.

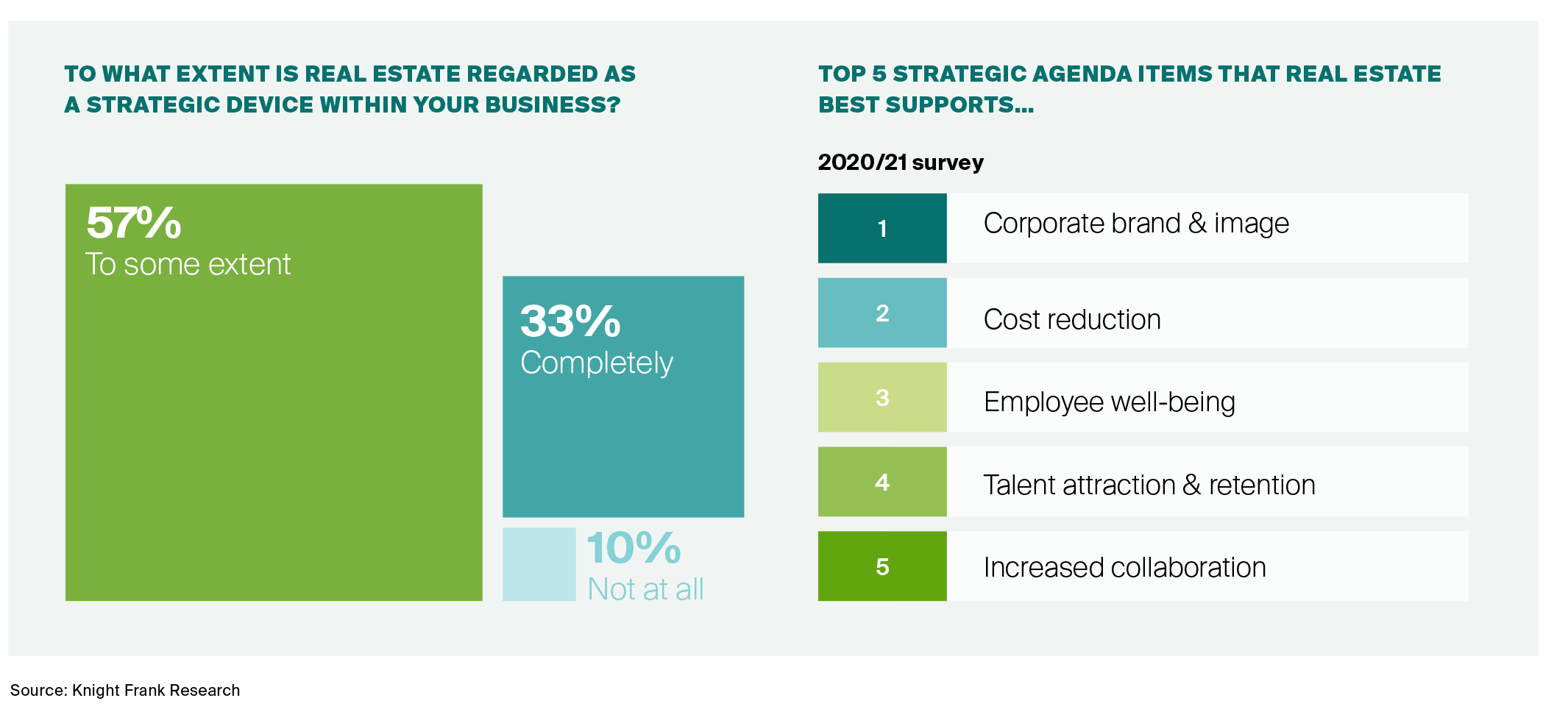

1. A more strategic role for the office

Ninety per cent of our survey respondents regard real estate as a strategic device for their business. The office is something that supports, facilitates or portrays a wider business agenda or purpose. What is telling is this represents an increase on the 80% of respondents who believed so when we first surveyed back in 2018. Despite the recent hyperbole, the office continues to matter – having strategic purpose and significance. The top 5 strategic agenda items best supported by the office are shown below. Foremost is the role of the office in showcasing corporate brand, identity and culture. As such, the office increasingly portrays the values and purpose of the wider business, something that has been difficult to sustain during lockdowns where staff were both dispersed and remote. These five items, in particular, will be at the heart of the push by occupiers to repurpose their offices.

2. A more compelling environment AND experience

They will also lead occupiers towards a different quality of product. A flight to quality is evident across all UK cities as occupiers seek office space that is both attractive to staff and compelling relative to alternative work settings, such as home. The office increasingly needs to provide its occupants with more than they can obtain elsewhere. So the flight to quality is synonymous with a flight to amenity rich buildings, particularly related to health and personal wellbeing. Whilst a single office building cannot feasibly provide all such amenities, they can be delivered within a managed estate or within the boundaries of a micro-market. This complementarity between amenities, even if in disparate ownerships, is important and central to the workplace experience – and experience is central to the modern workplace. Building owners need to deliver workplace experiences, through a service and amenity layer which supports their customers (and their staff) in creating that all-important sense of purpose and belonging.

3. A more heavily utilised and productive space

Real estate typically represents the second largest cost of any occupier. At times of crisis, or in a post-crisis response, real estate has often been in the cross hairs when it comes to cost reduction. This was certainly the case in the immediate post-GFC period when there was a ‘slash and burn’ attack on corporate office space. The fact that this, as noted above, has not occurred in response to the pandemic is significant. It suggests that occupiers have recognised that the simplistic reduction of quantum of space is not effective and actually creates environments and experiences that are sub-optimal for staff and their productivity. It appears the approach to real estate costs is instead focused around maximising the return on investment an occupier makes when taking a lease. This supports the provision of a more compelling and attractive office, but also requires the space to be more intensely and more consistently utilised. Consequently, occupiers are reconfiguring office space towards more collaborative, shared spaces underpinned by hot-desking and desk-sharing regimes rather than the move towards more personalised space, as noted in the chart below.

The post-pandemic period does not generate the existential crisis for offices that some have predicted. It does however usher in a period of accelerated evolution, whereby business leaders seek to repurpose their office space to support wider strategic agendas, create an attractive and compelling workplace for their staff, and ensure that the investment made in that space is fully maximised. These dynamics will shape the behaviour of occupiers across the UK over the next cycle.

Download UK Cities 2022