How investors are capitalising on our life online

Global mobile data traffic grew by 49% during 2019, and it’s predicted to expand by 32% per annum until 2025 – when the average person is expected to interact with smart devices 5,000 times a day. On the receiving end of that growth is a lucrative investment with a rising profile: data centres – which welcomed 701 megawatts of take-up in Europe in 2020.

6 minutes to read

Data now forms the most mobile commodity in existence. It’s critical to the new economy, with ‘invisible’ data centres operating as an integral backbone behind every click, swipe or tap we make online. And our ever increasing screen time is no cheap thrill; on average, each new data centre adds up to $700 million to the global economy.

In fact, it’s safe to say that the internet – and the way we use it – is constantly expanding. As shown above, in an internet minute Google receives 3.8 million searches, 4.5 million videos are viewed on YouTube and $997k is spent online. Continued digitalisation, the adoption of remote working, the social media evolution, the Internet of Things and the rise of e-commerce have all added to the increased demand for data centres.

But perhaps the truest catalyst behind this hyperscale growth has been the advent of Cloud services.

What is the cloud?

The Cloud is just a data centre tenant, such as Google Cloud, Amazon Web Services and Microsoft Azure – all of which collectively make up 80% of the occupational market. They take whole building leases and sub-let to financial institutions, ISPs (Internet Service Provider) and gaming companies on a plug-and-play basis so that the customer doesn’t have to worry about sourcing software or infrastructure – it’s a little bit like a WeWork.

The European data centres market

The European market is seeing an unprecedented rate of growth. Tier 1 markets (such as Frankfurt, London, Amsterdam, Paris and Dublin) grew by 24% in size alone through 2019. This growth has been driven by a record increase in take-up over the last four years; throughout the whole of 2016, total take-up was 78 megawatts, but in the small window of Q2 2020, it was 52 megawatts.

In London, for example, we are currently disposing of over £800m / 600 megawatts worth of data centre developments sites, and assuming each of these schemes secures planning consent, the market will double in size again over the next two years.

Those Tier 1 markets are ranked as such because they are either financial powerhouses or are hyper connected cities with numerous sea cable landing stations that connect them to the rest of the globe. There is immense competition in these markets, which I believe could lead to a downward pressure placed on the returns sought by operators and their investors.

What’s the data centres investment landscape?

Data centres and industrial logistics are perhaps the only asset classes to have genuinely benefited from the Covid-19 pandemic, which is unsurprising given our exponential increase in cloud application conference calls while working from home, our rise in mobile screen time and our weekend Netflix marathons.

The likes of Microsoft and Google (who have experienced a 500%+ increase in cloud application usage through Covid-19) are of the opinion that the new normal will see at least a 200% increase on data centre demand and usage compared to pre-Covid levels. For context, data centre REIT performance has been running at circa 10% year-on-year for the last six to seven years.

Plus, there have been several notable transactions in the marketplace that indicate investor appetite has been far from dampened, including Digital Realty’s purchase of Interxion in a deal worth $8.4 billion; one of the largest data centre mergers on record.

How investors can enter the sector

Corporate equity acquisition: Given the record year we had in 2020, there’s now a lack of investible stock in prime markets. In the instances where there are opportunities, most operators are extremely well-backed and as a result, don’t require capital injunction to aid further expansion, particularly if the investor has no operational expertise. However, if you’re willing to get ahead of the Cloud, then there are opportunities in Prague, Athens and Moscow.

Direct investment into new management teams: We’ve seen the emergence of three new data centre development platforms backed by Goldman Sachs, KKR and GAW Capital Partners. Given this market is essentially all about securing the Cloud, management teams for new operating entities only need to be slim; this could include an ex-Cloud employee who knows where the Cloud is drifting (which we believe is west to east), together with a real estate lead, and a head of construction who offers the necessary repertoire and experience.

Development and value add: We’ve seen several alternative-use assets traded over the past few years where a significant premium would have been secured if data centres were considered. Seeing as other use classes might be underperforming, and given government appetite for data centres, it’s worth looking at your existing portfolio. We’re looking for sites of at least five acres within proximity to existing data centre clusters, substations and fibre ducts.

Long income: As most leases are held with the likes of major international industrial developers, long income opportunities are thin. However, we will be launching two asset sales this year to let to major global colocation providers for terms of 20 and 23 years respectively, both with a fixed 2.5% annual rent indexations.

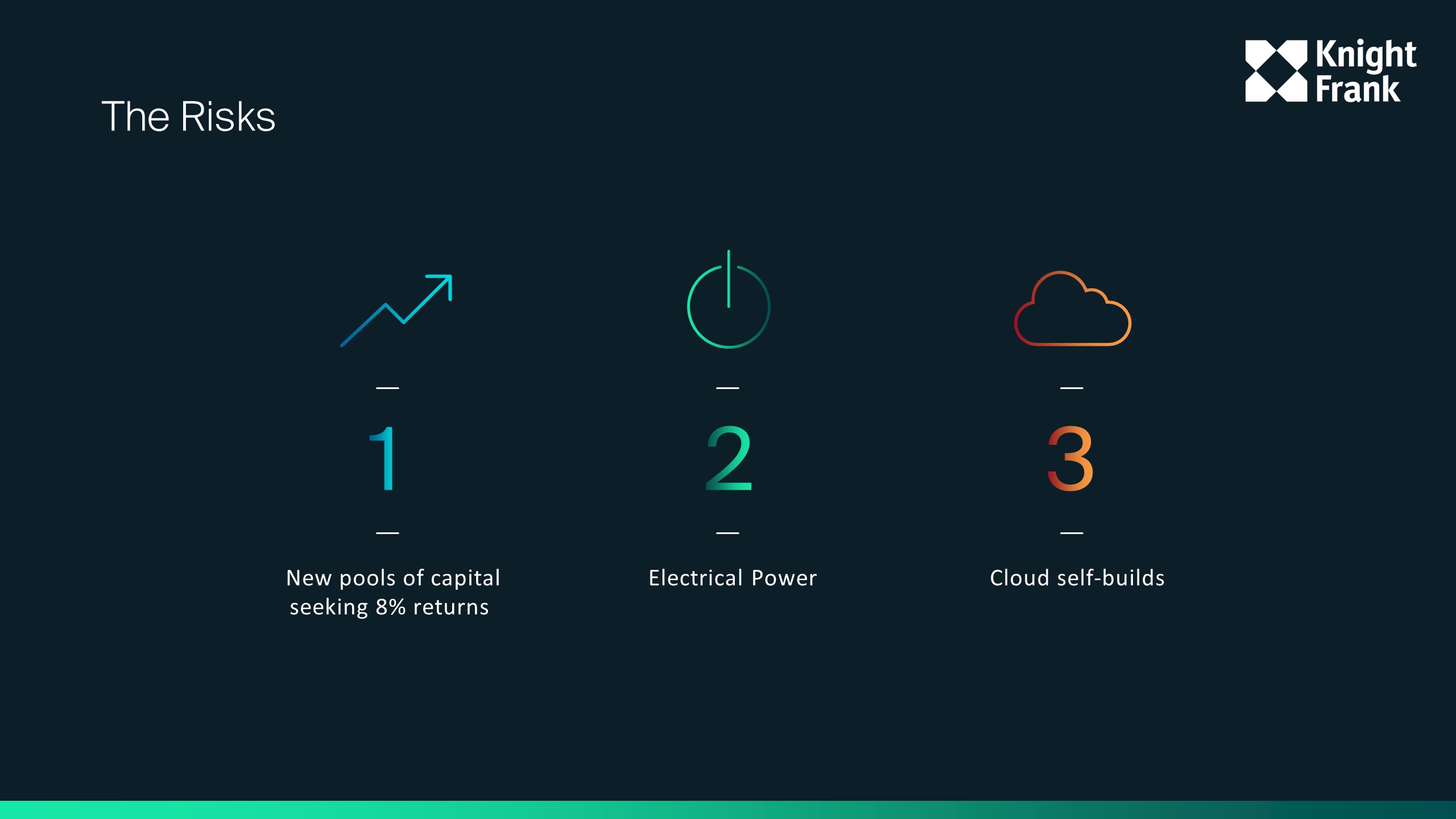

What are the risks?

As you’d expect, investing in this space does come with a set of risks.

One of the biggest threats to today’s colocation market is the emergence of new capital coming into the sector and driving off 8-10% returns, undercutting the market and enabling higher front-loaded capital deployment during the acquisition of new viable data centre development sites.

The second risk is power. All the Tier 1 markets have effectively run out of available electrical power, with new connections only predicted to be delivered in a four to five year timeframe. Naturally, this kills viability, and as such, operators are having to seek alternative power solutions, such as solar, wind and gas.

The final risk consideration is the Cloud building its own facilities and reducing its reliance on colocation operators. This has already begun to happen, and whilst it won’t kill the colocation market – the Cloud wouldn’t want to hold the liability of their own application performance – we do expect to see a slight slowdown in take-up and a softening of headline rents.

But there are plenty of opportunities

There is a dearth of available high-voltage power and there is a growing need to implement sustainable solutions; Microsoft recently announced a commitment for all its data centres to be carbon negative by 2030. There is a serious opportunity for investors or new entrants to link both green power infrastructure with viable data centre real estate in emerging or profit-making markets.

These insights were first explored at the European Breakfast. You can watch an on-demand version of the event here. All data was accurate at the time.

Want to find out more? You can read our latest EMEA Data Centres report in partnership with DC Byte here.