Another bout of mortgage volatility tees up a big week for the Bank of England

Making sense of the latest trends in property and economics from around the globe.

6 minutes to read

Prime rents

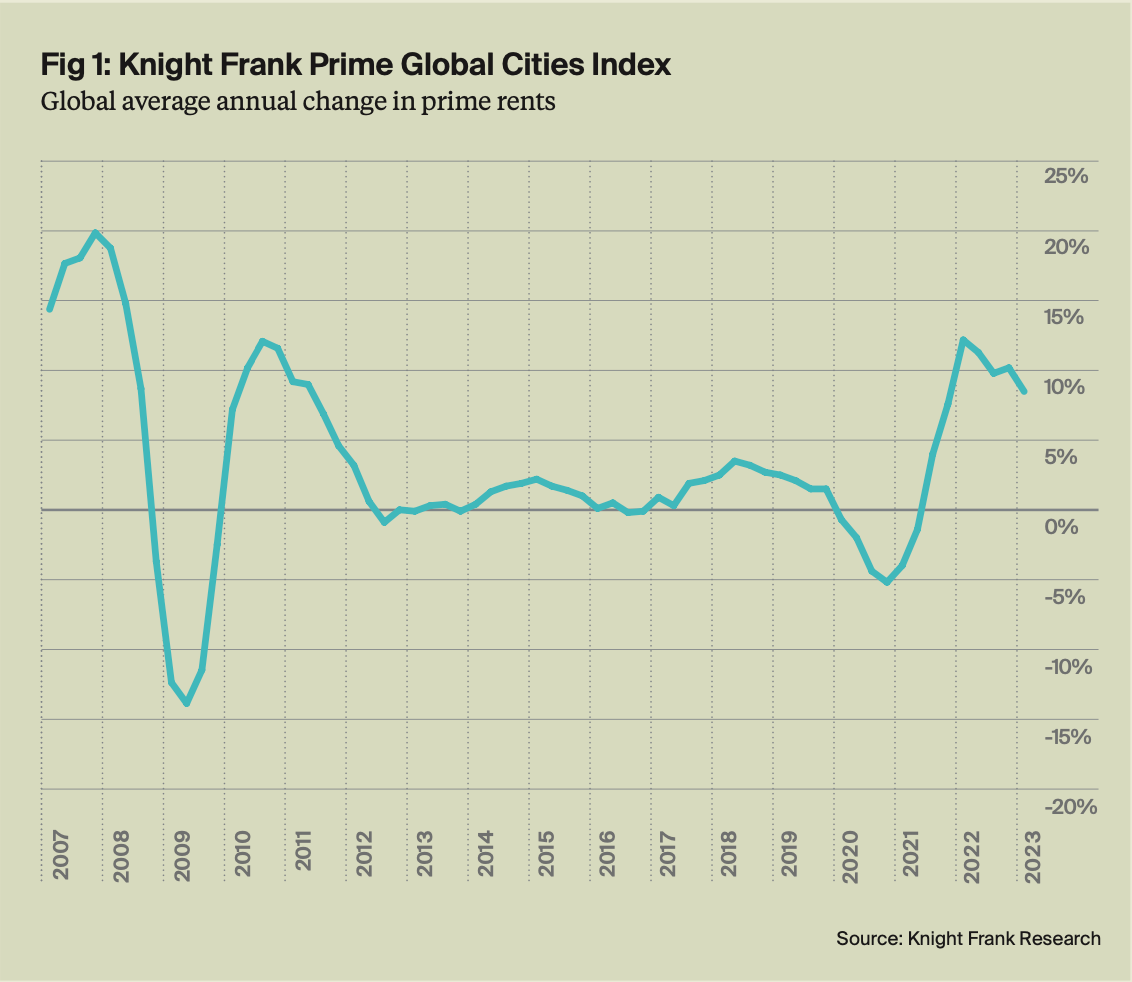

The post-pandemic recovery in city economies that began in late-2021 triggered an unprecedented period of rental growth for prime homes.

Lockdowns disrupted construction, putting pressure on new supply. Meanwhile, landlords were lured to part with homes amid strong demand in the sales market. Cities reopened and workers returned, adding a sharp uptick in demand for a depleted supply of rental properties.

We're seeing signs of easing, but not much (see chart). The Knight Frank Prime Global Rental Index, out this morning, rose 8.5% in the 12 months to March this year, slipping back from the 10.2% recorded the previous quarter. Rents hit record highs in eight of our 10 markets and the index now stands 21.7% above the pandemic low of Q1 2021.

Singapore leads with rental growth of 31.5% over the past 12 months. International workers flooded back to the city following the reopening of borders in late 2022 and successive hikes in stamp duty rates have raised the cost of property purchases, nudging potential buyers into renting. London follows with growth of 16.9%. Sydney, Toronto and New York also recorded double digit growth.

How governments will react to higher rental costs remains the key question for investors. Rent caps seem to be off the table in most markets for now, and policy focus is shifting to encouraging a surge in new build- to-rent accommodation.

Volatility

Official figures published last month showed that the annual rate of inflation during the year to April had fallen by less than economists had expected. The core rate of inflation actually accelerated to the highest level since the early nineties.

It was an ugly surprise. The subsequent spike in gilt yields prompted a wave of volatility in mortgage markets, with lenders pulling entire ranges amid a surge in applications from borrowers seeking to beat rate hikes. Markets are skittish, and earnings data published yesterday generated another big reaction. Two-year gilt yields surged 0.25% points to 4.87%, the highest level since 2008. The five-year swap rate moved above 5%, raising the likelihood of further increases in mortgage rates.

These are big moves on the back of just two numbers, but it is clear that investors are worried about a dreaded wage-price spiral, or that the UK economy is uniquely vulnerable to rising prices in a manner that would justify significantly higher interest rates over the long-term. Bank of England governor Andrew Bailey doesn't think so - "we still think the rate of inflation is going to come down, but it's taking a lot longer than expected," he told reporters yesterday.

How long is anyone's guess, but the Bank last month said the headline rate of inflation would drop to around 5% by the end of this year and be below the 2% target in early 2025. We'll know a lot more on Wednesday morning when we see the CPI reading for May. The Bank will publish its decision on whether to raise the base rate from 4.5% the following day.

For more, see this piece from Tom Bill, published on Monday.

Mortgage lending

The first three months of 2023 were very subdued in the mortgage market as the impacts of the mini-budget were still being felt. Lenders advanced £58.8 billion to borrowers, down almost a quarter on the same period a year earlier and the lowest level since the depths of the pandemic, according to official figures published yesterday.

The near-term outlook looked broadly similar. Lenders committed to lend £48.9 billion, down 16.1% on the previous quarter and 40.7% less than a year earlier. A recovery began in late March and gathered pace into April and May, which will show up in the next round of figures, but the prevailing volatility in the mortgage market suggests it's going to be a muted year for mortgage lending.

The banks are eager to do business and have shown a willingness to absorb volatility in order to keep their books ticking over. More than 90% of lending was done at rates less than 2% above the base rate during the quarter, the highest proportion since 2008. High loan-to-value lending is holding up too, and the share of lending at LTV ratios above 90% was largely unchanged compared to a year earlier. Meanwhile, arrears ticked up at an annual rate of 12.5% and now stand at £14.9 billion, still relatively low at just 0.89% of all outstanding mortgage debt.

A new phase

The inflationary period that has dominated global economics since the pandemic appears to be entering a new phase - at least in the US.

The US Consumer Price Index fell to just 4% in the year to May, the weakest rate of growth since March 2021. Though core prices are barely moving, markets think the reading is enough for the Federal Reserve to at least pause its cycle of interest rate hikes later today. Whether that will mark the end of this period of tightening is uncertain, and will depend on whether the prevailing themes hold in June's CPI, but the focus is now moving to how long it will be before the first cut - anything this year looks unlikely.

The US reading mirrors themes in the Eurozone, where the annual rate of inflation dropped to 6.1% during the year to May, the lowest level since Russia's invasion of Ukraine. Again, core inflation proved sticky, easing to just 5.3%, from 5.6%, but most signs are encouraging. The annual rate of inflation fell in 18 of 20 eurozone member countries during the period.

In other news...

Despite the strength in the labour market, homeworking appears to be less popular with businesses. The latest ONS (BIC) survey found 47% of companies surveyed were not using or intending to use increased home working as a permanent business model, its highest level since September 2021 and above the 20% who were using or planning to use it - Will Matthews has more.

Industrial development and financing costs remain elevated due to inflationary pressures. However, well-capitalised investors may find that taking on development risk now could offer strong returns with a favourable risk profile, writes Claire Williams.

For a round up of the latest UK residential market data, Chris Druce has his latest update here.

Elsewhere - Bellway flags demand woes as high rates weigh (Reuters), China readies for stimulus as economic recovery founders (FT), demand for Europe factory space rises 29% amid ‘nearshoring’ rush (FT), the UK's competition watchdog goes after Asda and Sainsbury's over land restrictions (Times), Geneva mulls a new wealth tax (Bloomberg), and finally, NYC office occupancy rises above 50% for the first time since the pandemic (Bloomberg).