Financial services sector driving office market in Nairobi

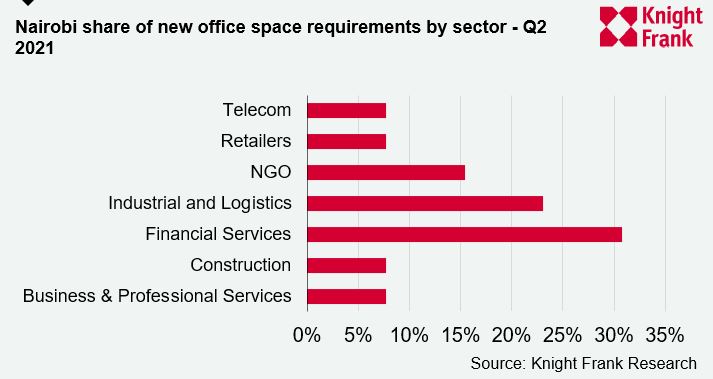

According to Knight Frank’s Q2 2021 Africa Office Market Dashboard, the share of new office space requirements in Nairobi was dominated by the financial services sector that took up 31% of office space.

3 minutes to read

There have been encouraging signs that businesses that had previously put office requirements on hold due to the pandemic are now reactivating their searches.

In Q2 2021, the levels of enquiries and activity increased, which combined with landlords becoming more flexible, allowed for discounted rents and lease concessions such as rent-free periods. This ensured improved levels of take up as they bid to attract and retain new occupiers.

This increased office market activity has underscored the ‘flight to quality’ trend with businesses taking advantage of more affordable rental levels plus the chance to occupy better quality office accommodation, with improved facilities placing employee wellbeing at the forefront.

According to Knight Frank’s Q2 2021 Africa Office Market Dashboard, the share of new office space requirements in Nairobi was dominated by the financial services sector that took up 31% of office space followed by Industrial and Logistics sector with 23%, NGOs at 15% and Business & Professional services, Construction and Telecom sectors each taking up 8% of office space in the city, respectively.

Anthony Havelock, Head of Agency, Knight Frank Kenya commented: “The future of the office is certainly not dead and we are seeing contrary signs of a push to return to the office both from organisations but also led by employees. This has been evident in the number of enquiries that we are receiving plus the active requirements with key sectors such as financial services and NGO’s driving demand.

"We continue to see the trend of Nairobi being the regional focus as multinationals confidence returns and they look to either enter the market here for the first time or expand their existing operations. There are noticeable indications of increased take up and larger transactions starting to return to the market. Headline rents have largely remained stable for the best quality buildings but there is continued downward pressure on the poorer quality stock. The outlook is cautiously positive as the oversupply dynamic which has dominated the market for so long is starting to ease”.

Nairobi has continued to see a gradual return in business confidence reflected by the increased number of business entities registered. According to the Registrar of Companies there was a 25% month on month change with 8,483 companies registered in July 2021 compared to 6,786 companies registered in June 2021. Knight Frank anticipates this will result in increased demand for offices later in the year.

Across the 28 African cities Knight Frank monitors, prime headline office rents remained relatively resilient with 16 out of the 28 cities tracked experiencing rental stability during Q2 2021.However, market performance continues to vary between countries.

Nigeria for example has recorded increased occupier activity in the market driven by office relocations from the CBD to the suburbs, as occupiers gravitate to locations offering both better quality accommodation, as well as more affordable occupational costs. In addition, in locations such as Tanzania, Knight Frank anticipates the prime office market will recover underpinned by renewed investor confidence fuelled by the new leadership.

However, markets such as South Africa continue to see increased vacancy rates and downward pressure on prime rents against the backdrop of the pandemic and existing supply glut prompting landlords to offer incentives and discounts.

Tilda Mwai, Senior Researcher Knight Frank Africa added: “The overarching trend across Africa’s office market has been the flight to quality. Occupiers remain intent on occupying flexible spaces that place employee wellbeing above all else but also with favourable lease terms. As such, tenant released space has been a key concern to landlords in Grade B buildings in some of the countries."

Professional services sector has continued to fuel demand accounting for 28% of all the new office requirements alongside the industrial and logistics sector that accounted for 16% of new requirements.

For more information, please contact Tilda Mwai