Daily Economics Dashboard - 5 February 2021

An overview of key economic and financial metrics.

2 minutes to read

Download an overview of key economic and financial metrics on 5 February 2021 2020.

Equities: Globally, stocks are higher. In Europe, gains have been recorded by the CAC 40 (+1.0%), FTSE 250 (+0.6%), STOXX 600 (+0.4%) and the DAX (+0.2%). In Asia, the TOPIX (+1.4%), S&P / ASX 200 (+1.1%), KOSPI (+1.1%), Hang Seng (+0.6%) and CSI 300 (+0.2%) were all up on close. In the US, stocks rose for their fourth consecutive day on Thursday. Futures for the S&P 500 and Dow Jones Industrial Average (DJIA) are both +0.4%.

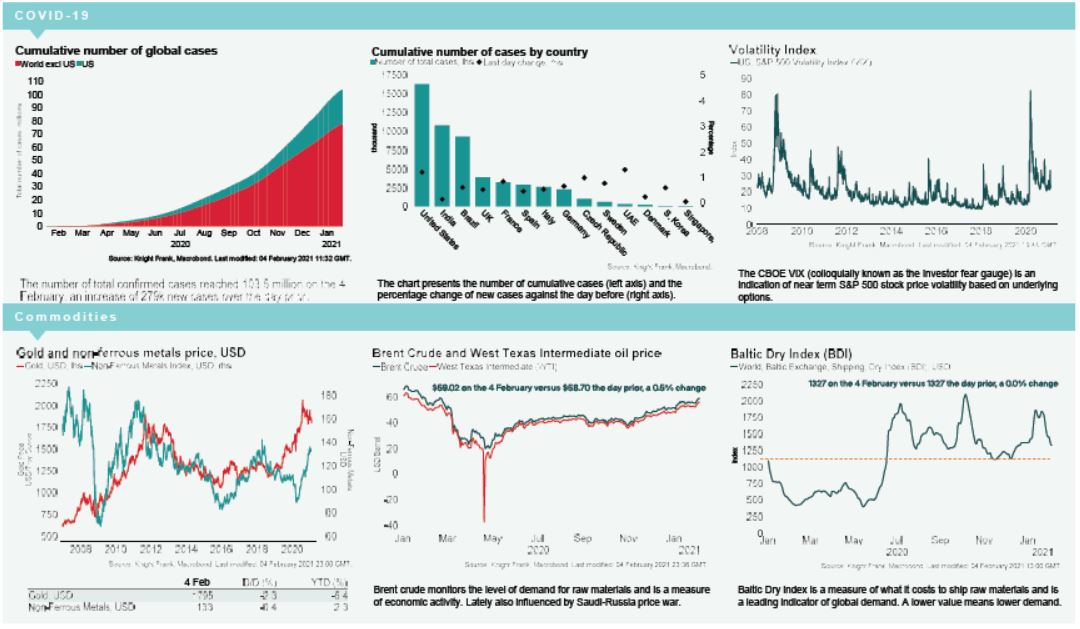

VIX: Following a -5% decrease over Wednesday, the CBOE market volatility index has declined a further -0.1% this morning to 21.7, remaining above its long term average (LTA) of 19.5. The Euro Stoxx 50 volatility index is also lower, down -2.3% to 20.9, remaining below its LTA of 23.9.

Bonds: Yesterday, a sell-off in 30-year US treasury yields pushed the yield curve to its steepest level since 2015, with the spread between 30-year yields and 5-year yields circa 147.3bps. This morning, the UK 10-year gilt yield and US 10-year treasury yield have both softened +1bp this morning to 0.45% and 1.14%, their highest levels since March 2020 and January 2021, respectively. Meanwhile, the German 10-year bund yield has held steady at -0.46%.

Currency: Sterling appreciated to $1.37, while the euro is currently $1.20. Hedging benefits for US dollar denominated investors into the UK and the eurozone are at 0.50% and 1.37% per annum on a five-year basis.

Baltic Dry: The Baltic Dry remained unchanged at 1327 on Thursday, the first session in ten to not record a daily decline. The index therefore remains at its lowest levels since 22nd December and -29% below the four-month high seen in mid January.

Oil: Brent Crude and the West Texas Intermediate (WTI) and have both increased +1.2% this morning to $59.55 and $56.91, their highest prices since January 2020.

US Unemployment: There were 779k new unemployment applications in the week to 30th January, below market expectations of 830k and lower than the previous week’s reading of 812k. This is the lowest number of jobless claims since the last week of November and the third consecutive week of a decline in applications.