Prime London Lettings Report: November 2020

Prime central London lettings index: 148.3

Prime outer London lettings index: 155.9

1 minute to read

Average rental values continued to fall in prime areas of the capital in the final quarter of 2020, pushed down by high levels of supply.

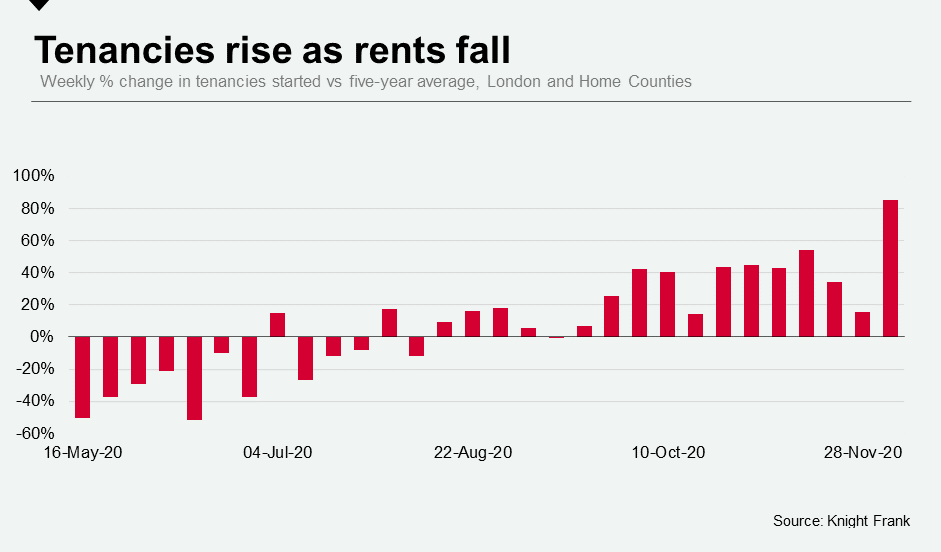

However, activity levels remain well above the five-year average.

The decline in average rents was 10.5% in prime central London in the year to November, while in prime outer London the fall was 9%. These were the largest decreases since the global financial crisis although around half as steep as 2008/09.

The declines have been less marked in south-west London, where supply has not built up to the same degree. In locations with a predominance of family houses, a strong sales market means the supply of rental properties has been kept in check.

In Wimbledon, the annual decline was 3.3% in November, while it was 5.4% in Richmond. Falls were also less marked in Belsize Park (-5.6%) and Hampstead (-3.8%).

In more central areas, the combination of a glut of former short-let properties and weaker demand has driven rents lower.

Demand from international students and corporate tenants has been weaker since the pandemic. However, the rollout of the vaccination programme may see both travel restrictions ease and sentiment improve among international students, which could have a marked impact on demand in prime London lettings markets in 2021.

Despite the declines, the number of tenancies started remains well above the five-year average, as the below chart shows. Many tenants are moving due to a need for more space, while also taking advantage of lower rents.

The number of new prospective tenants registering was more than double the five-year average during October and November. Viewings were 85% above the five-year average in the same period.