What do interest rates hikes mean for the UK housing market?

Your monthly question on economic trends shaping housing markets.

3 minutes to read

What do interest rates hikes mean for the UK housing market?

The question is currently being greatly debated among commentators, forecasters and within our own team – what will hawkish interest rate moves mean for house prices? With two successive 50bps moves by the Bank of England (BoE), I decided to explore the impact higher base rates will have on affordability.

A few months ago I asked would a base rate of 3% cause the housing market to reverse?, at the time 3% looked as though it may be the peak but more hawkish tones have taken hold and expectations have shifted. The latest forecasts from Capital Economics were a peak of 4% in 2023, but have moved this week to 5%. Looking at futures and the market expectation is that they may reach 5.5% or 6% following last week’s budget.

What does it mean for mortgage rates?

The average spread over base rate, since the series began in 1995, is 128bps for a two-year fix and 183bps for a five-year. This implies mortgage rates would climb to somewhere in the region of 5.25-7.5% from 3.6% in August and a low of 1.2% in September.

However, we could see spreads start to narrow as we get closer to the end of the current hiking cycle. Some forecasters expect the spread to be around 70bps when rates reach their peak. This level was seen as recently as February 2020, and in 2019 the average spread was 84bps. True, they have widened in 2022 as the market prices in future rate rises, but if we look at previous tightening cycles they tend to rebalance. That means mortgage rates might top out at 5-6.5%.

The horse has bolted, affordability is already being stretched.

Interest rate moves alone in 2022 have added 25% onto the average cost of a mortgage. If rates top out at 4.8% that figure goes to 42% - if they climb to 6% it’s a 60% increase. That is before factoring in any house price growth. Even with the stamp duty cut reducing the amount of mortgage needed by £2,500 for any purchase above £250,000, the resultant change is a saving of around £12 a month.

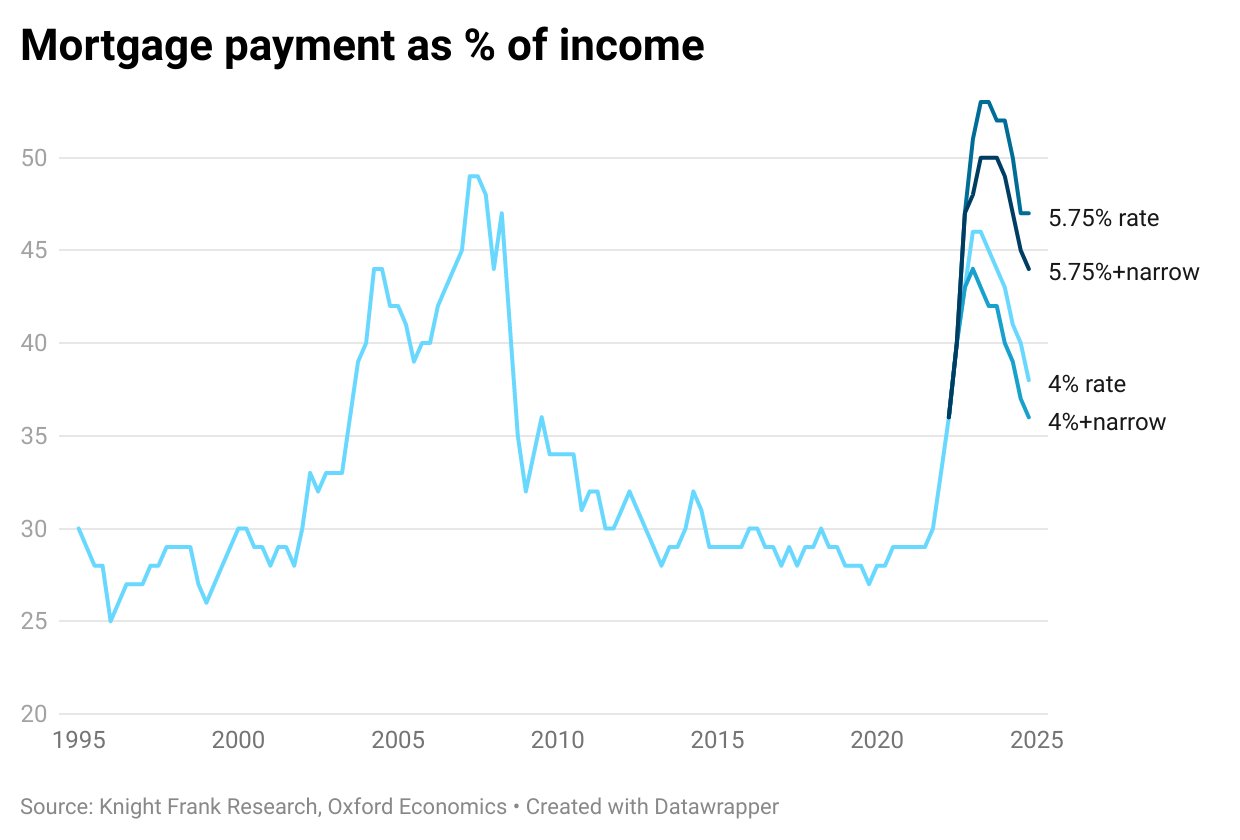

The average proportion of income spent on a new mortgage has hit a level not seen since 2008 at 39%. This is far below the 50% witnessed in 2007. We have crunched the numbers including average house prices, our latest forecasts, predictions for wages and the two interest rate scenarios, with and without spreads narrowing, to see what that would do to affordability.

Assuming rates reach 5.75% with no narrowing, the proportion jumps to levels above those last seen in 2007. With interest rates undoubtedly rising, especially to balance the fiscally loose budget, the path for spreads and wages will be key.

Not only that but there is a lagged effect of affordability due to mortgage offers being in place for up to nine months. Some 95% of mortgage advances in the second quarter of 2022 were for fixed rates. In addition, existing mortgage holders can ‘port’ mortgages and a staggering 83% of outstanding mortgages are on a fixed rate with an average rate of 2%. As these unwind there could be more pressure.

The picture painted has resulted in a raft of bearish forecasts for UK house prices. Capital Economics are forecasting a 5% fall in 2023 and 2% in 2024, Oxford Economics pencil in a 0.5% decline followed by almost 5% and HSBC a 7.5% fall. We recognise prices, on balance, will come down after period of strong growth. However, we cannot deny the underlying imbalance in supply and demand still playing out, as well as the strong employment market which will limit forced sales. We are currently reviewing our forecasts after weighing up all the above so watch this space.