Prime central London prices rise as race for space calms down in outer areas

April 2022 PCL sales index: 5432.3

April 2022 POL sales index: 272.0

2 minutes to read

There are early signs that the robust price growth present in UK property markets since the pandemic is calming down.

Nationwide reported that growth fell to 12.1% in April from 14.3% in March. Part of the reason is rising supply, which the RICS reported last month had increased for the first time in a year. The slowdown comes against the background of rising inflation and mortgage rates.

Now, it appears that prime outer London (POL) may also be peaking.

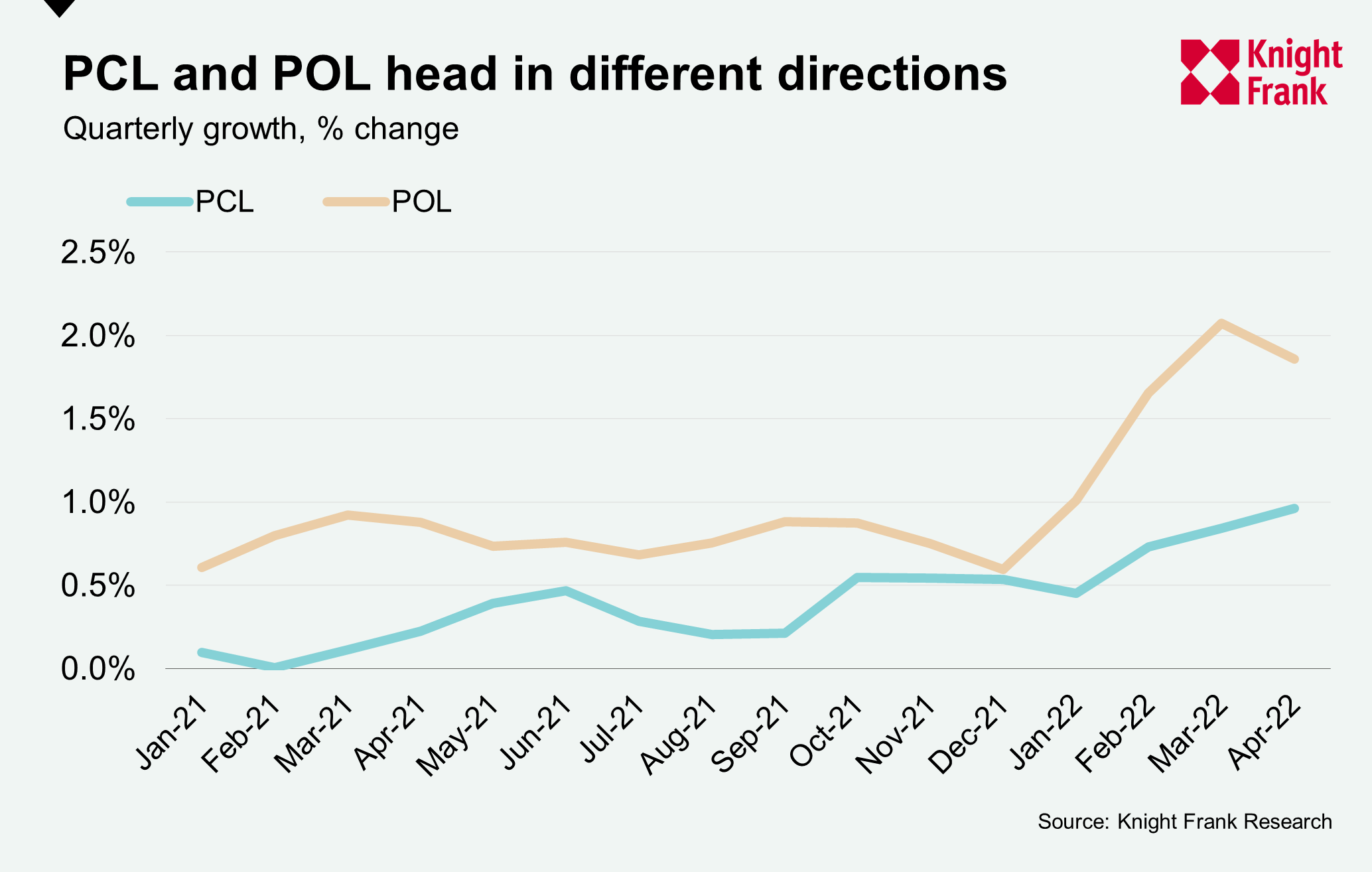

Average prices in POL rose by 1.9% in the three months to April, which compared to 2.1% in March. It was the first such slowdown this year, as the chart below shows.

Meanwhile, prime central London (PCL) prices remain in steady recovery mode, with quarterly growth reaching 1% in April, the highest such figure since July 2015.

“The property markets in central and outer London are increasingly on different trajectories,” said Tom Bill, head of UK residential research at Knight Frank. “Price growth in outer London is moderating as the race for space becomes less frenetic and rising mortgage rates and the higher cost-of-living take their toll. Meanwhile, prime central London is recovering after six subdued years and a relatively quiet pandemic, a process bolstered by the gradual return of international travel.”

As a result of these calmer conditions in recent years, buyers in central London sense more relative value. Higher taxes and political uncertainty following Brexit means that average prices in PCL are 14% lower than they were at the start of 2015. Prices in POL have declined by 4.7% over the same period.

Meanwhile, annual growth in PCL reached 2.3% in April, which was the highest rate since May 2015. Annual growth was 4.5% in POL.

We forecast that average prices in PCL will increase by 6% in 2023, with cumulative growth of 22.2% in the five years to 2026, outperforming other UK residential markets. In prime outer London, we expect 16% growth over the same period.

Demand remains very strong compared to supply across London, which will keep broad upwards pressure on prices. While new sales instructions (supply) in the first four months of the year were 1% higher than the five-year average, the number of new prospective buyers (demand) was 69% higher.