Prime London Sales Report: November 2020

Prime central London sales index: 5298.5

Prime outer London sales index: 256.8

2 minutes to read

Price growth in prime outer London is outpacing central London in the final months of 2020 as demand for space and greenery remains strong after two national lockdowns.

Average prices increased 1.6% between June and November in outer London, which includes areas like Wandsworth, Belsize Park and Chiswick. Prices fell 0.1% over the same period in prime central London.

There was no notable impact on prices during the second national lockdown as there was during the first. Following quarterly declines of more than 3% in April and March, the decrease in the 12 months to November was 3.3% in POL and 4.3% in PCL.

Overall, the relatively muted price performance in all areas since the market re-opened in May underscores how the release of pent-up demand has been balanced by fragile sentiment surrounding the UK economy. Prices in PCL have also been kept in check by international travel restrictions.

We forecast 4% growth in PCL next year and 5% in POL on the basis that any economic fallout from the pandemic will be more limited in prime markets. Different sectors of the economy have been affected in a wide-ranging way by Covid-19.

Two common sources of demand in prime London are finance and tech. While many tech stocks have risen during the pandemic, the UK government’s assessment was that finance and insurance has been one of the least-impacted sectors of the economy.

The easing of international travel restrictions as vaccines are rolled out will further boost demand.

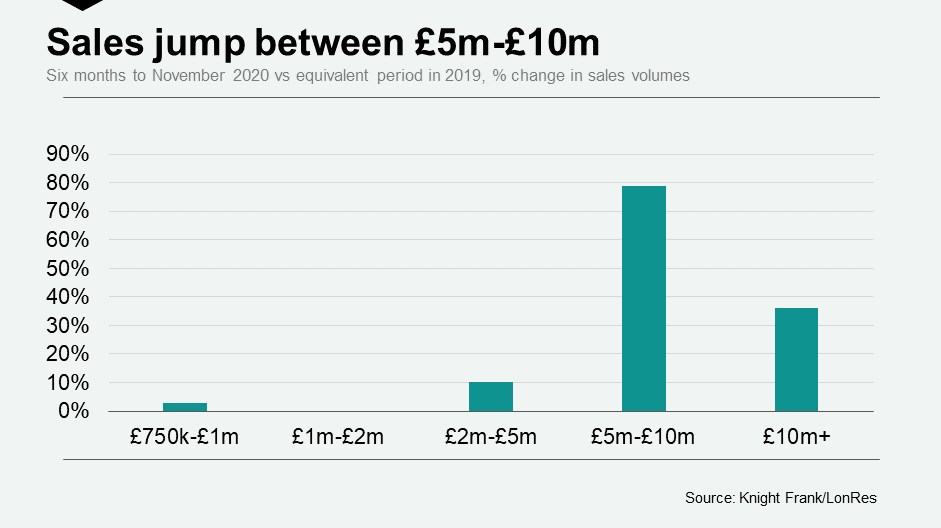

Furthermore, momentum is building in higher-value markets across London, which has been particularly notable between £5 million and £10 million, as the below chart shows.

The increase underlines how the market is not simply responding to a stamp duty holiday, the effect of which is negligible in this price bracket.

Instead, it reflects growing demand for houses, which tend to be more numerous in this price bracket and more in-demand among domestic buyers. Above £10 million, supply includes a higher number of luxury penthouses.

It is also a result of how far prices have fallen in recent years due to tax changes and political uncertainty, which had a more marked impact in higher-value markets. Average prices between £5 million and £10 million fell 8.8% in the two years to November, the largest fall of any price band.