Covid, currencies and confidence: the global economy in five charts

Covid cases are reaching record highs. However, investor sentiment is improving with hopeful news in vaccine development, leading to a retreat from safe haven assets.

3 minutes to read

Covid cases continue to hit fresh daily highs. In the US there has been over 2 million confirmed cases since the beginning of November. Three percent of the North American population has tested positive the highest of any region. Europe and Latin America both sit at 2%.

Europe has been a hotspot accounting for 39% of the confirmed daily cases in the most recent seven days, yet the fresh wave of lockdowns is seeing this start to fall back. Sweden, which has been closely watched for its approach, is the latest to impose stricter measures.

Third quarter GDP results continue to be release with many surprising on the upside. The UK saw GDP rise by 15.5% in Q3, the Euro area by 12.6% and the US at an annualised rate of 33.1%.

Despite restrictions being less severe than earlier in the year, consumers have already spent much of the savings they built up and will likely reduce spending and increase savings. There is a clear drop-off in activity where lockdowns have been imposed, such as in The UK and France. This means that in fourth quarter we will likely see a contraction in GDP. Economies in Asia-Pacific are leading the recovery. This is particularly evident in China, where domestic demand is now above the levels of Q4 2019, according to Oxford Economics.

Investment may pick up on the back of positive vaccine news. This combined with continued governments and central bank support could counteract some of the fall in consumption, lessening the drop in activity.

In a show of investor sentiment, equity markets in the US reached new record levels on Monday after Moderna announced its Covid-19 vaccine showed 94.5% efficacy. This came a week after Pfizer and Germany’s BioNTech reported 90% efficacy. With many other vaccines in Phase 3 trials we could see more results published in the coming week – any positive signs will continue this momentum.

Whilst there is a lot of optimism on the speed of recovery it won’t be uniform globally. Any vaccine rollout is likely to be staggered across countries and regions and could slowdown the return to normality, especially when it comes to international travel.

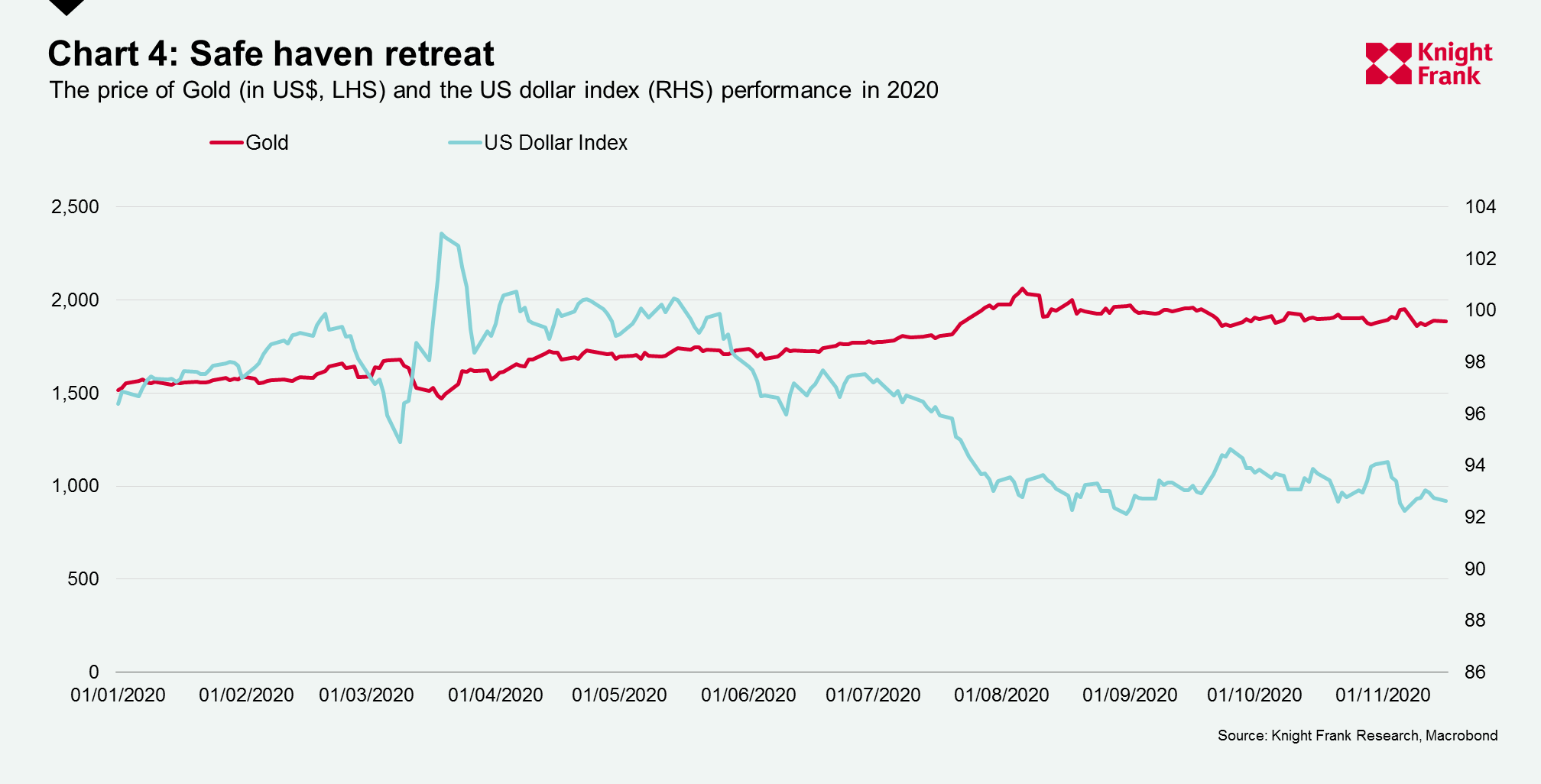

The optimism surrounding the global recovery is leading investors to pare bare safe haven bets. In the wake of the recent vaccine news we have seen gold settling below $1900 after hitting over $2000 in August, although it remains almost 25% above its 2020 opening.

The dollar dipped slightly as with lower demand for US treasuries. After rallying at the beginning of the pandemic the dollar has weakened around 10% against a basket of currencies and is 4% weaker than the start of 2020. The change in international investor buying power is shifting.

Wall Street analysts have predicted the dollar could fall by 20% if vaccines become widely available leading to faster economic rebound.

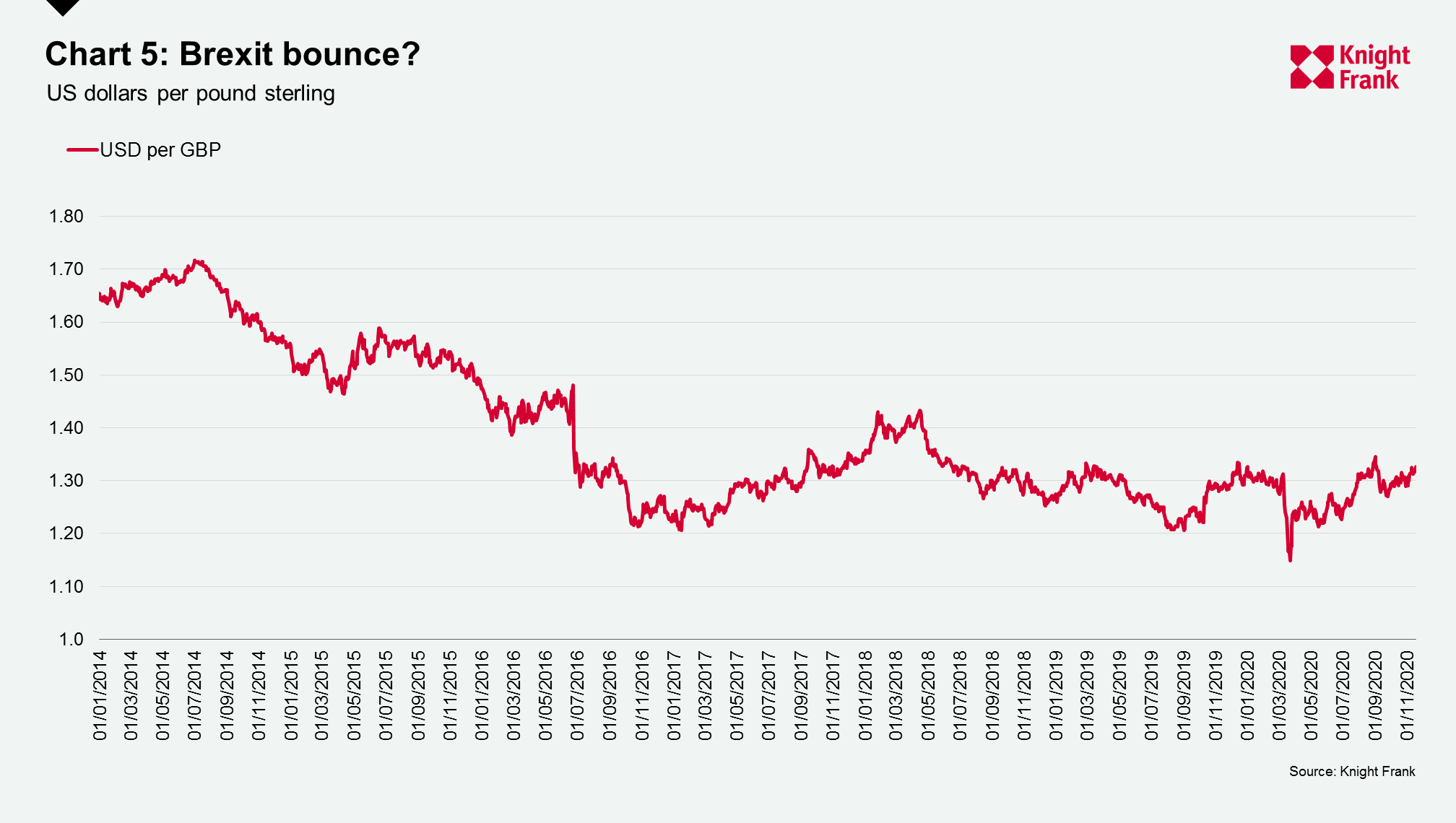

In the UK, Brexit is never far from the headlines. It was reported this week that we could see a deal agreed between the two sides next week. Any indication on progression towards a deal has been meet with a bounce in the pound. If a deal is agreed, we would undoubtedly see the pound strengthen immediately and likely continue to do so for some time. In early 2020 UBS wrote that the pound has been undervalued since 2014 and that they expect to see it rise to $1.40 by the end of 2020 with a three-year equilibrium of $1.54.

The opportunity for discounts from currency on inbound investment will narrow and will continue to do so if the pound builds strength. For international purchasers of residential property this needs to be considered alongside the 2% overseas buyer surcharge being introduced in April. To see what the tax implications for purchase currently are and will be from April 2021 use the Knight Frank overseas buyer calculator.