Covid-19 in Africa: Focus on North Africa

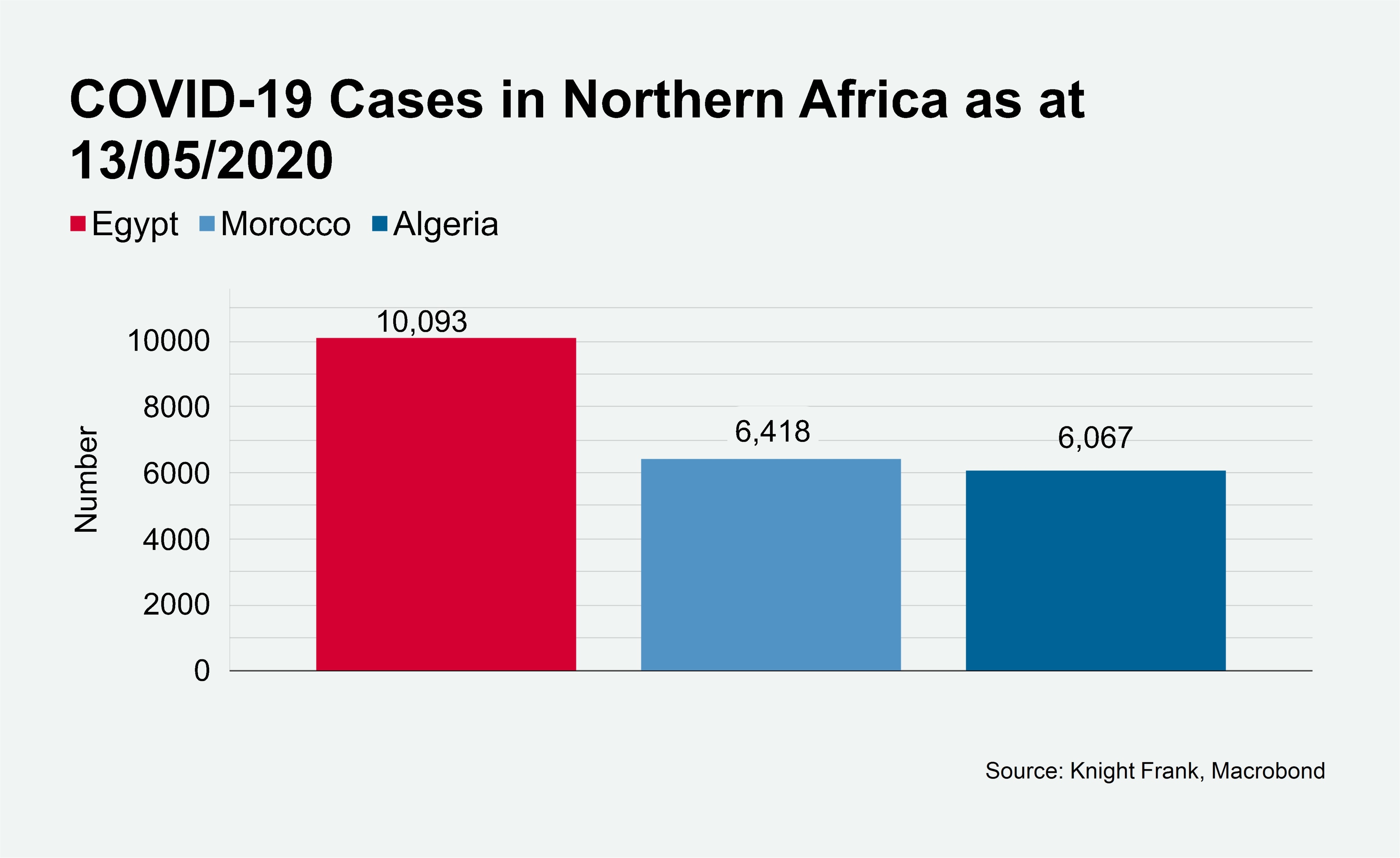

Within Africa, North African countries have recorded the highest numbers of Covid-19 cases. While economic outlook in the region has previously been clouded by political uncertainty, the impact of Covid-19 on individual economies is expected to vary depending on which sectors are prevalent in each economy.

6 minutes to read

In Algeria, the pandemic’s impact has been exacerbated by plummeting oil prices and continued political uncertainty. The IMF has projected that the country’s GDP will contract by 5.2% in 2020 down from 0.7% growth rate witnessed in 2019 before rebounding t oa 6.2% growth rate in 2021.

In Egypt, the pandemic is anticipated to disrupt the recent steady economic growth, which has been attributed to the 2016 IMF’s macroeconomic stabilisation program. The pandemic’s impact on the country’s tourism sector and export revenues is set to significantly increase Egypt’s financing needs, with the IMF already providing US$2.8 billion in additional funding. Despite these challenges, according to the IMF, Egypt’s economy is expected to remain the most resilient in the region with GDP growth projected at 2.0% in 2020, down from 5.6% in 2019.

Disruption in the tourism and manufacturing sectors due to the pandemic coupled with the current impact of drought on the dominant agricultural sector, are anticipated to push Morocco’s economy into a recession for the first time in more than two decades. The IMF has projected that Morocco’s economy will contract by 3.7% in 2020, down from the 2.2% growth rate in 2019, before rebounding to a 4.8% growth rate in 2021.However,as a net oil importer, the rapid fall in oil prices and access to funding are likely to ease the pressure on the country’s economy.

|

Algeria

Fiscal & Monetary Policies

- The declaration and payment of income taxes for individuals and enterprises have been postponed, except for large enterprises.

- Relaxation of contractual deadlines and suspension of penalties for companies that experience delays in completing public contracts.

- Introduction of unspecified compensation for losses incurred by private firms.

- The Bank of Algeria lowered its reserve requirement ratio from 10% to 8% and later to 6%.

- The bank further lowered its main policy rate to 3.0% from 3.5%.

- The bank has further eased solvency, liquidity and NPLs ratios for banks. Banks are also allowed to extend payments of loans without a need to provision against them.

Government Interventions

- Ban on international travel.

- Closure of learning institutions.

- Suspension of Public transport.

- Partial lockdown and curfew measures.

- Suspension of all demonstrations.

|

|

Egypt

Fiscal & Monetary Policies

- The government has announced stimulus policies in worth EGP 100 billion with EGP 50 billion targeted at the tourism sector.

- The moratorium on the tax law on agricultural land has been extended for two years.

- The stamp duty on transactions and tax on dividends have been reduced.

- Capital gains tax has been postponed until further notice.

- The preferential interest rate on loans to tourism has been reduced from 10% to 5 % while for SMEs, industry and housing for low-income and middle-class families has been reduced from 10% to 8%.

- The limit for electronic payments via mobile phones has been raised to EGP 30,000/day and EGP 100,000/month for individuals, and to EGP 40,000/day and EGP 200,000/per week for corporations.

- A new debt relief initiative for individuals at risk of default has also been announced, that will waive marginal interest on debt under EGP 1 million if customers make a 50% payment.

- The regulations requiring detailed information on borrowers issued last year have been relaxed alongside the suspension of credit score blacklists for irregular clients and waiver of court cases for defaulted customers.

- The central bank has also launched an EGP 20 billion stock-purchase program.

Government Interventions

- Imposing night-time curfews.

- Temporary closures of places of worship.

- Ban on international air travel.

- Suspension of all types of legumes exports for three months.

- Strategic planning on reopening of the economy to coexist with Covid-19.

|

|

Morocco

Fiscal & Monetary Policies

- Businesses with less than 500 employees made temporarily idle and experiencing a reduction in turnover of more than 50% can defer social contribution payments until June 30. Their employees who become temporarily unemployed and are registered with the pension fund will receive 2,000 dirhams a month and can put off debt payments until June 30.

- Companies with an annual turnover lower than 20 million dirhams can also defer tax payments.

- Provision of a tax exemption for additional compensation paid by firms to employees in the formal sector up to a limit of 50% of the average monthly net salary.

- The Central Bank reduced the policy rate by 25 bps to 2.0%.

- To reduce volatility, the Capital Market Authority decided to revise downwards the maximum variation thresholds applicable to financial instruments listed in the Casablanca Stock Exchange.

- Bank al-Maghrib further decided to; expand the range of collateral accepted for repos and credit guarantees to include public and private debt instruments, increase and lengthen central bank refinancing operations to support banking credit to SMEs and provide FX swaps to domestic banks.

- The government will further guarantee 95% of banks’ new short-term loans to SMEs through the Central Guarantee Fund.

Government Interventions

- State of health emergency declared.

- Suspension of all international passenger flights.

- Ban on public gatherings.

- Closure of learning institutions and places of worship.

|

Source: IMF Policy Tracker

Impact on Real Estate Sectors

Further to the above government interventions, we analysed market activity in the different real estate sectors, across the region between March and April 2020. While the level of impact has varied across different sectors, the retail and industrial sectors have been severely impacted as a result of the pandemic across the region.

In Morocco, residential transactions have been halted as a result of the closure of notary offices due to the imposition of lockdown measures. Rents in the sector are expected to record slight declines of not more than 20% with the possibility of recovery by the end of the year. In the commercial sector, occupiers are looking to renegotiate their leases in order to obtain greater levels of flexibility. Rent defaults have primarily been recorded by small and medium occupiers, where these missed payments have been classified as debt rather than default as a result of government interventions. Furthermore, state-owned offshoring parks have offered the possibility of delaying payments or making monthly payments. We expect rents will decline slightly by not more than 10% due to the limited supply in prime offices.

Algeria’s relative independence from foreign markets has been a safety net in terms of the initial impact on the real estate market. In the commercial sector, all active transactions have been delayed including the shift of most banking institutions and multinationals to the Bab Ezzouar financial district. In the residential sector, developers have started to incentivise sales rather than leases in a bid to absorb any potential future impact from the crisis.

In Cairo, rents across the commercial and residential sectors have remained stable. However, commercial and residential developments have stalled as a result of the containment measures adopted by the government.