Global Residential Outlook – 2 October 2020

Key takeaway:

Urban residential prices largely held firm in Q2 with the Turkish city of Izmir leading our 150-city rankings in our Global Residential Cities Index.

The trends we’ve identified suggest urban housing markets are displaying a degree of resilience in the face of the pandemic. The index’s annual rate of growth declined marginally from 3.6% to 3.4% between March and June this year.

All eyes are on the third quarter to determine whether second (and third) waves of the pandemic put a brake on sentiment, demand and hence price growth

3 minutes to read

Categories:

Need to Know:

European governments are tightening measures to contain second waves of the virus with parts of the UK, Madrid, Marseille under local lockdowns.

In the US, democrats are assembling a new $2.4tn economic stimulus package, targeting a vote next week.

Banks are delaying relocating UK-based staff to the EU before the Brexit transition period ends due to fears of being confined by coronavirus restrictions

Residential digest

Europe

Our weekly look at the UK residential market identifies six themes that will shape the UK market in the coming months – from sentiment to the timeline for a vaccine and from Brexit to the UK’s stamp duty holiday, Tom Bill sets out what lies ahead.

According to Nationwide, UK house prices increased by 5% in September compared to the same month a year ago. This is the highest annual rate of growth in four years.

In Spain, the government has extended the prohibition of evictions and of "abusive increases in residential rents" until 31 January 2021, but mortgage holidays have come to an end.

Asia Pacific

In Australia, lending rules for first time buyers are due to be relaxed further by March 2021, the rules will also apply to those seeking a mortgage with the intention of increasing access to credit and ramping up the speed which applications are assessed.

Residential building approvals in Australia fell by 1.6% in August, driven by a decline in apartment approvals, which fell by 11% percent, while detached house approvals rose by 4.8 per cent.

Hong Kong recorded 4,358 sales in August, a 7% increase year-on-year despite the resurgence of COVID-19 in August and the subsequent tightening of social distancing restrictions. With the number of infections dropping gradually in late August, potential buyers became active in flat viewing again, leading to improved sentiment in the residential market.

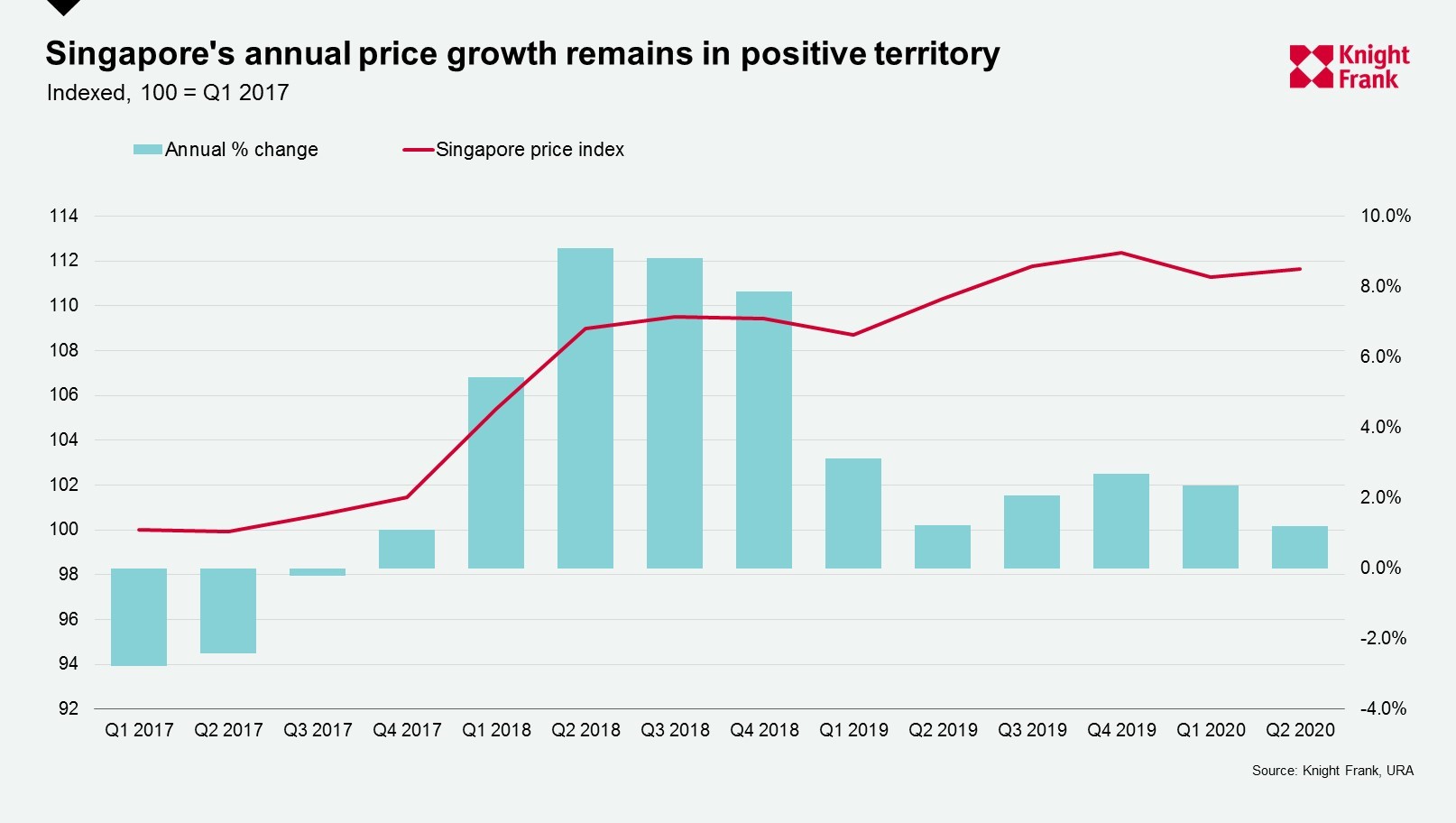

In Singapore, residential prices continue to rise year-on-year although the rate of growth moderated to 1.2% in Q2 2020 and a flash estimate by the Urban Redevelopment Authority's (URA reported growth of 0.8% in Q3. Landed transactions doubled to 512 units in Q3 (based on transactions up to Sept 22), versus just 211 units in Q2.

US and Canada

In Manhattan, 21 contracts were signed above $4 million last week - the highest total since the second week in March. Last week’s total is higher than the same week in 2019 when 18 contracts were signed.

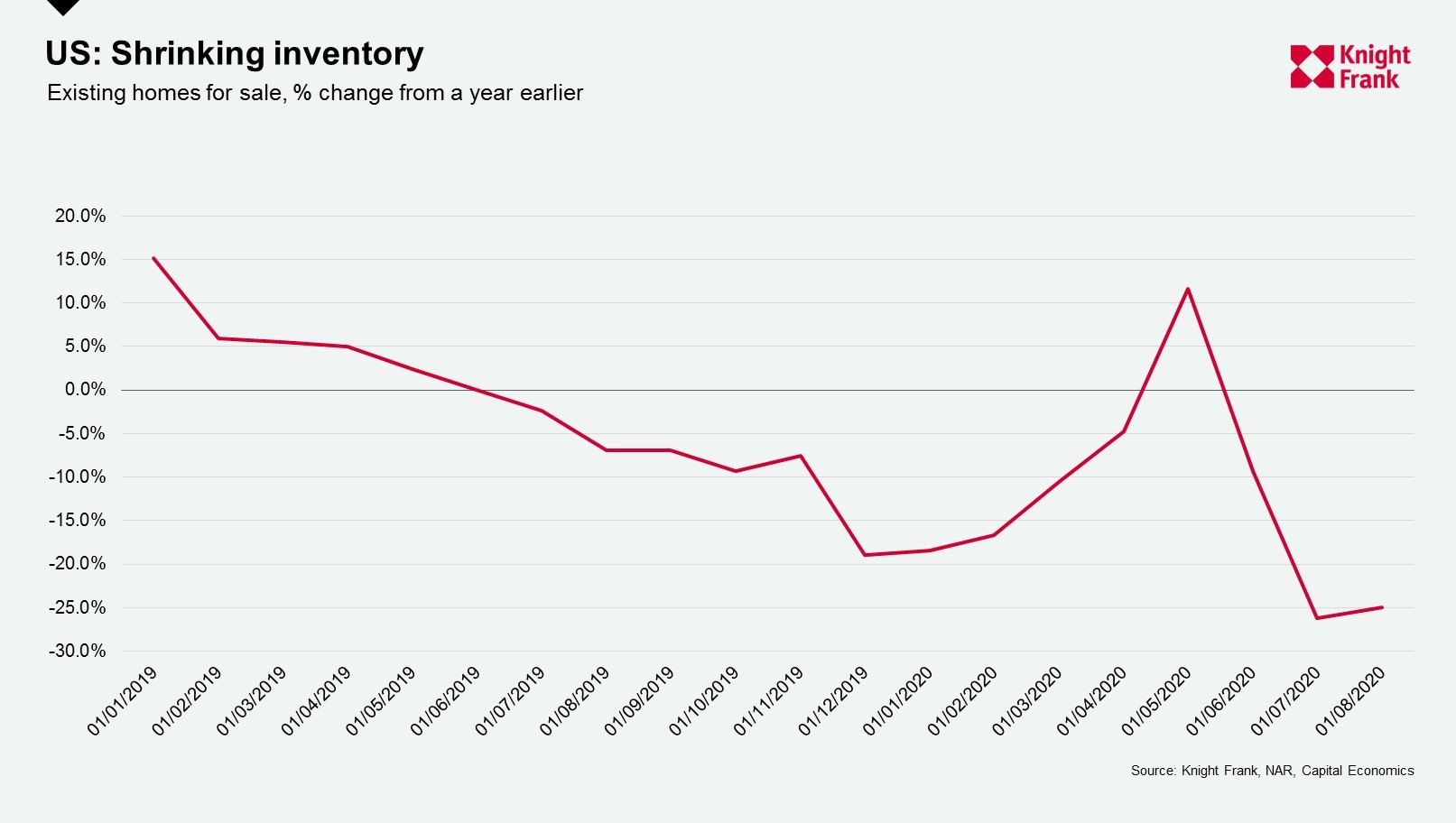

In the US, surging demand has led to a sharp drop in the number of new homes for sale, with the fall driven by a collapse in the inventory of completed homes. Although an uptick in building permits for single family homes will provide some support, completed inventory is expected to remain tight. Capital Economics forecasts new home sales will fall back from over 1 million annualised in August to around 900,000 by early next year.

Recommended listening

This week we focus on the sustainability agenda, looking at the key findings from our new Active Capital report and speak to a leader in the field, Richard Walker, Managing Director of Iceland Foods. Click one of the links below to listen:

Apple

Spotify

Acast