Prime London Sales Market Makes Hesitant Start to 2024

February 2024 PCL sales index: 5,320.5

February 2024 POL sales index: 272.7

3 minutes to read

A developer once said that after a slowdown, you need no further bad news for two consecutive quarters for a recovery to take hold.

Perhaps an overly-simplistic rule but one that comes to mind when looking back at the last few months.

Inflation fell faster than expected in the final quarter of last year and by Christmas money markets were pricing in five interest rate cuts of 0.25% in 2024.

The positive mood didn’t last long into 2024 due to stubborn underlying inflation, as we explored here, and mortgage rates have begun to creep back up.

In the background is a swirl of bad news that includes an increasingly heated countdown to the general election and overseas military conflicts.

And then came this month’s Budget.

The key headline for prime London markets was the abolition of the non-dom tax regime from next April.

To date, those with non-dom status have not paid tax on their worldwide income for up to 15 years under a fairly complex set of rules, making the UK somewhat of a global outlier.

From next year, new arrivals will pay nothing for four years before paying the same as other UK residents, a simplification the government has said will raise £2.7 billion a year by 2028/29. There were 69,000 non doms in the tax year ending in 2022.

Current non doms may well feel the rules of the game have changed in the middle of the match but the property market in London’s most expensive postcodes could get a boost from next April when a two-year transition period begins during which they will only pay 12% on their worldwide income.

For a full reaction to the Budget including changes to multiple dwellings relief on stamp duty, please click here.

Meanwhile, the average annual price fall in prime central London (PCL) was -2.4% in February while the comparable figure in prime outer London (POL) was -1.6%.

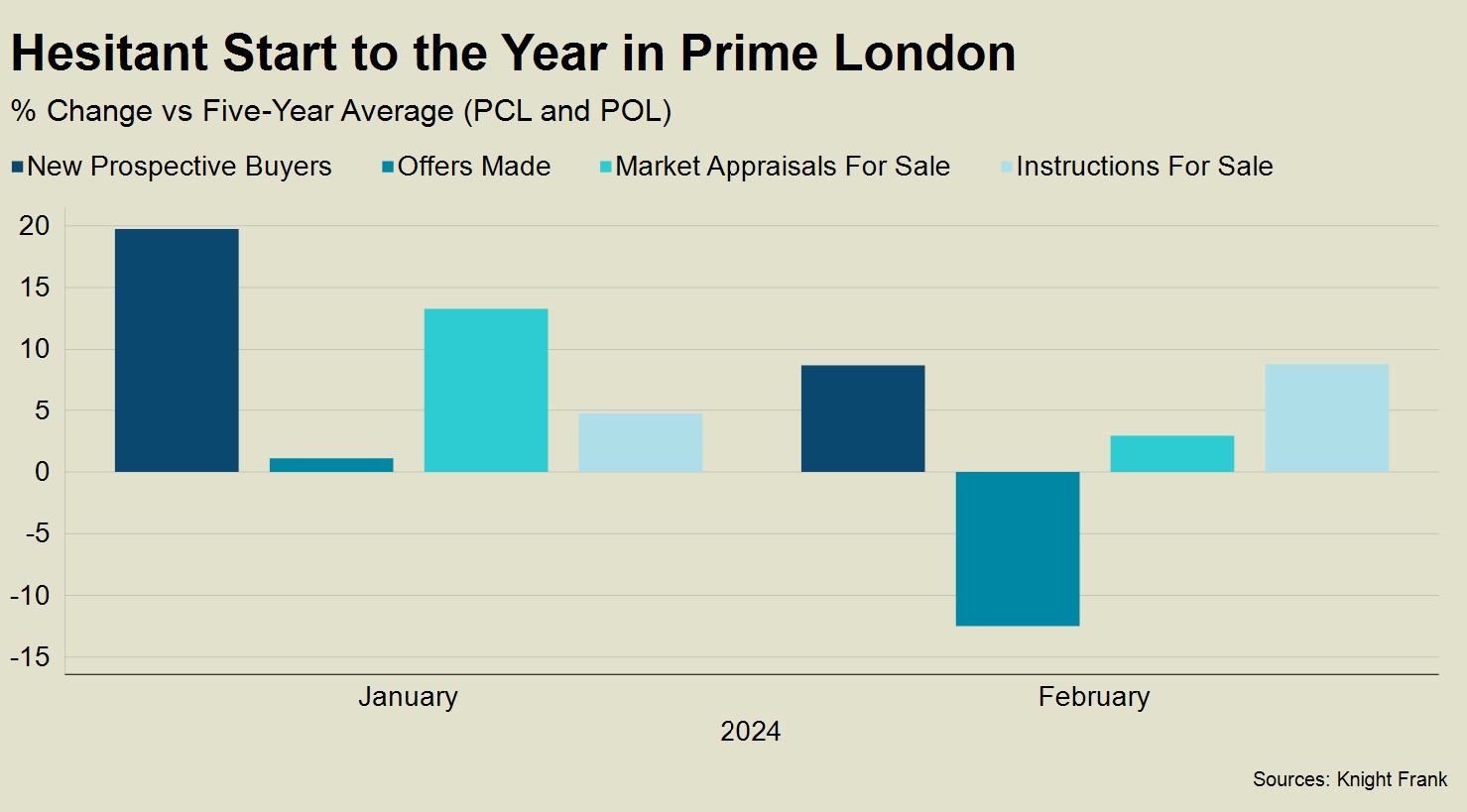

It was an uncertain start to 2024 that can be seen on the chart below.

On the demand side, the number of new prospective buyers was 9% higher than the five-year average in February, according to Knight Frank data adjusted for leap years.

That was lower than the equivalent rise in January and reflects the slightly gloomier mood in the second month of the year in relation to the outlook for mortgage rates.

This change was also visible in the number of offers made, which is a good measure for buyer sentiment. While the number was up by 1% in January versus the five-year average, there was a 12% decline in February.

And while the number of instructions for sale was up 9% in February versus a 5% rise in January, that was the result of a the relatively higher number of market appraisals carried out in the first month of the year. Market appraisals were only up by 3% in February compared to a 13% jump in January.

For buyers and sellers, they should look for some hope in what the Bank of England says rather than what it does (it is unlikely to cut) when it meets later this month.