UK Housing Market Activity Improves Despite Mortgage Rate Rises

Rate cut expectations have softened since early January, but a seasonal spring bounce is taking shape.

4 minutes to read

It has to be said, 2024 is not unfolding as planned for the UK housing market.

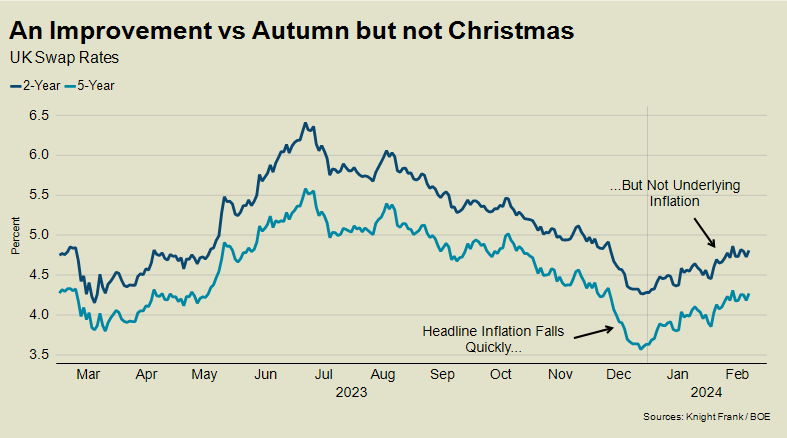

The five rate cuts predicted this year by financial markets in early January have become three as strong wage growth fuels underlying inflation. That’s pushing mortgage rates in the wrong direction.

The initial New Year optimism was sparked by a sharp fall in the cost-of-living in the final quarter of 2023. However, private sector wage growth in Q4 last year was ahead of expectations at 6.2% we learned this month.

It means the bank rate is likely to stay at 5.25% at the next two meetings of the Bank’s Monetary Policy Committee (MPC) on 21 March and 9 May, as we explored last week.

The outlook is not entirely clear though. The Bank risks deepening the UK’s shallow recession if it doesn’t cut quickly enough, its former chief economist Andy Haldane recently warned. This particular dilemma follows accusations the Bank was too sluggish in raising rates after the pandemic, leading to 14 consecutive hikes.

The first three-way split in the MPC’s decision this month since August 2008 highlights its predicament, with two members voting to raise rates despite headline inflation falling faster than expected.

Not for the first time in recent years, it makes you wonder who would want to be a central banker.

As expectations of a cut move further into the distance, the result for the UK housing market is that more lenders have nudged mortgage rates back above 4% in recent weeks.

The five-year swap rate (the instrument used to price fixed mortgages of the same length) topped 4.3% last Thursday morning, which compares to less than 3.6% in the period between Christmas and the New Year. The word that comes to mind is “ouch”.

Goldman Sachs tempered its outlook last week when it said it expected a cut in June rather than May due to the resilience of the labour market.

Despite the tougher lending landscape, the housing market has been on an upwards trajectory since the autumn, as the chart below suggests. Perhaps just not quite as steep as hoped for seven weeks ago.

“The signs are positive and demand indicators are heading in the right direction ahead of the spring market,” said James Cleland, head of the Country business at Knight Frank. “Many buyers are cautious about the wider economic environment and, as the last two months have reminded us, realistic pricing is key.”

“We had strong expectations towards the end of 2023, however the market has been slower out of the blocks than anticipated,” said Rory Penn, head of London sales at Knight Frank. “The signs are pretty clear though that this year will be stronger than 2023 with offer levels up and buyer sentiment improving.”

Underlining the resilience of demand, the number of offers made across the UK in January was 7% higher than last year, Knight Frank data shows.

After a relatively strong start in 2023 due to a post-mini-Budget bounce and a change of Prime Minister, stubbornly-high inflation and rising rates meant transactions were down by a fifth and mortgage approvals by a quarter compared to 2022.

This year, we expect transactions and prices to rise as rates calm back down – see our latest forecast here.

Irrespective of the swings on the swap market, the overall robust health of the housing market was underlined when HSBC issued its financial results last week.

It said the quality of its mortgage book was strong, having grown its UK market share to 8% from 7.7%. With an overall loan-to-value ratio of 53%, there are hardly red lights flashing on the dashboard.

“It’s a frustrating period for mortgage lenders,” said Simon Gammon, head of Knight Frank Finance. “They are keen to build their mortgage books but are feeling hamstrung by what is happening in the swap market. Their margins are already thin, which means they have to respond quickly when rates rise.”

So, while the UK housing market is heading in the right direction, some of the spring has gone from its step since the early days of January.

It may return next Wednesday of course, depending on how far the Chancellor goes in his pre-election Budget.