Is now the time for industrial development?

Assessing the potential risks and rewards of industrial development at present

8 minutes to read

Development and financing costs remain elevated due to inflationary pressures. However, well-capitalised investors may find that taking on development risk now could offer strong returns with a favourable risk profile.

Greater price certainty

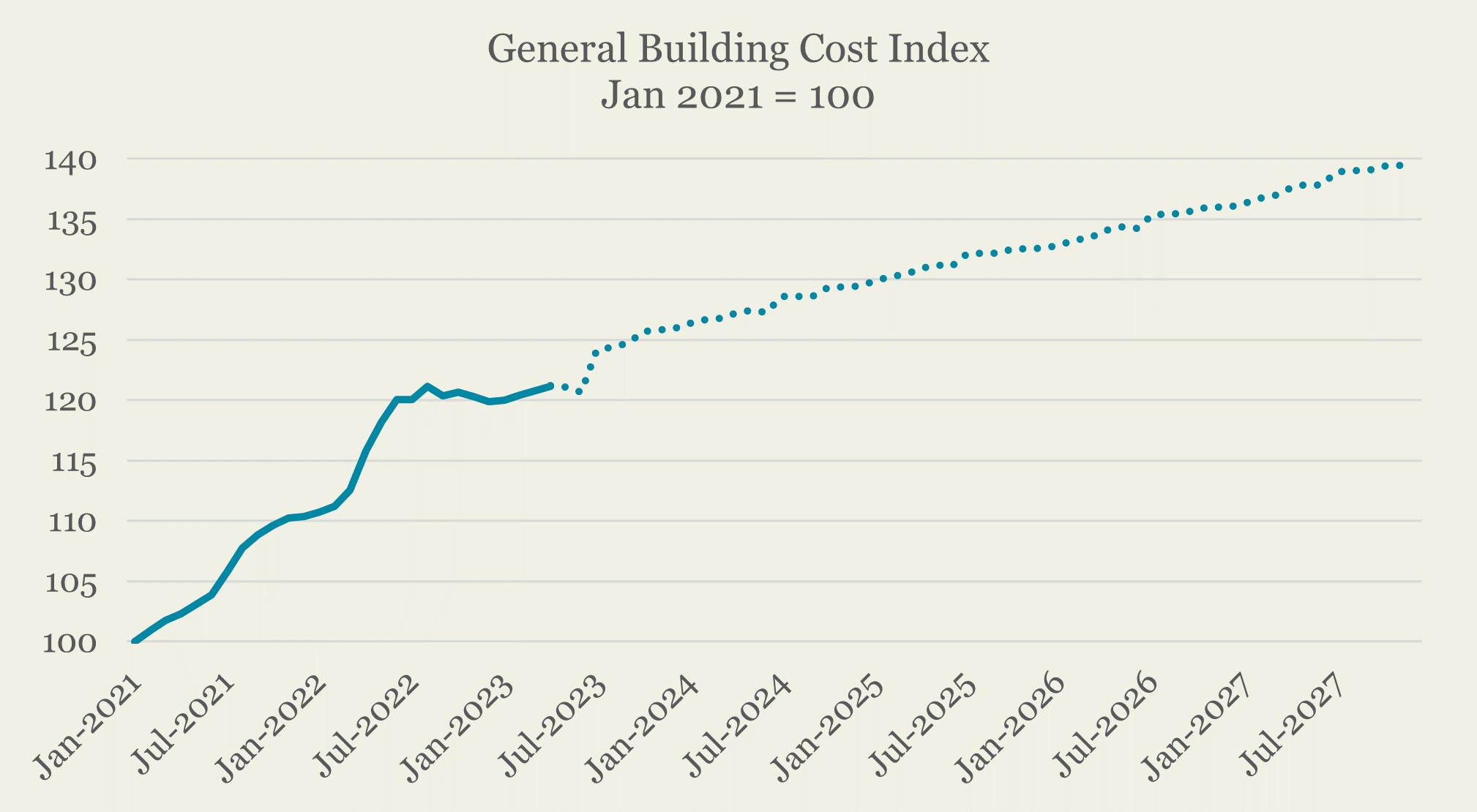

Despite continued inflation, construction prices have stabilised. The BCIS General Build Cost index shows that construction costs rose 8.0% (provisional) in the year to March 2023. However, prices dipped slightly month-on-month, and price growth is forecast to slow throughout 2023, with price growth of c.5.1% expected for 2023 (BCIS) and further moderation expected in 2024, with an increase of 2.6% anticipated (BCIS).

Compared with other sectors, the industrial sector benefits from short construction timeframes; the typical build period is typically 18 months or less, compared with several years for offices. Shorter build programmes can provide developers with greater price certainty or enable them to secure fixed-cost contracts for construction in advance, thus reducing risks associated with inflation.

Source: BCIS

Land pricing

Buying land may be difficult at present, given where yields and borrowing costs have gone. The increase in construction and financing costs, coupled with a softening in exit yields, means that, often, development appraisals can no longer justify current land prices.

Our Land Values Model shows that values in Q1 2023 are 36% down on Q1 last year. This decline is not surprising given the outward shift in exit yields, negative capital value growth and weaker expectations for future returns (both from rental income and capital value growth). However, the model is appraisal-driven; based on what an investor will pay for land, it doesn’t consider asking prices; or seller expectations. It is also worth noting that there is significant variation across markets.

With investors facing more significant uncertainty around inflation, borrowing costs, rental growth and exit yields, there has been a mismatch in terms of buyer and seller expectations on pricing, which has led to fewer land transactions recorded in the second half of 2022 and into 2023 (compared with H1 2022 or H2 2021).

However, land values have remained relatively stable over the past six months (down on average only 2% over the last six months) and the stabilisation in pricing is likely to encourage a rise in transactions in the second half of the year.

Reduced competition

Despite a fall in land values over the past year, our Land Values Model demonstrates that, as of Q1 2023, just 12 out of the 378 markets tracked have land values lower than three years ago (Q1 2020). Thus, development remains viable for most locations on land acquired a few years ago.

For developers with existing land banks, now could be a favourable time to bring forward new developments with less supply-side competition. Waiting for interest rates to fall or the economic outlook to improve could mean missing the opportunity to generate rental income and capture rental growth over the next few years; it could also mean greater competition when they do bring forward development.

As well as the inflationary impacts, some investors (and developers) are moving down the risk curve due to heightened economic uncertainty. Relative to standing investments, development projects have more downside risks. Developers are therefore holding off commencing construction until they have a pre-let agreement.

As a result, development activity is falling, with fewer development starts. Of the 162 developments granted planning consent since the beginning of 2022, 23% of these schemes are confirmed to have started construction (by mid-May 2023), compared to 71% of schemes consented between 2019-2021.

BCIS data confirms this trend, construction new orders for industrial were down -17.5% (y/y) in Q4 2022, and we expect this to fall further throughout 2023. There was a sharp spike in new orders in 2021, which led to a rise in development completions in 2021/2022, but we expect the rate of completions to slow throughout 2023 and into 2024.

However, over the past six months, prime yields have rebased and stabilised, build costs have held steady, and continued rental growth and rising prospects for rental growth (across most markets) have meant that the viability of development has improved across many markets. Many markets have crossed the development viability threshold in the past six months, with our Land Value Model recording fewer markets where development is not currently viable in Q1 2023 compared with Q3 2022. These factors may boost land sales and development activity towards the end of the year and into 2024.

Grade-A vacancy to remain low

Despite the uptick in new supply over the past couple of years, take-up levels have been robust, with 167 million sq ft of space taken up by occupiers in the past three years, up 54% on the three years previous. This voracious appetite for space has eased over the past few quarters, with just 6.9 million sq ft of space taken in the first quarter of 2023, down -17% on Q4, while Q4 recorded a -27% decrease on Q3. Take-up in Q1 2022 was on par with pre-pandemic levels suggesting the market may be normalising.

Despite demand returning to more normal levels, the market remains supply constrained. Vacancy rates are currently 4.0% (Q1 2023). Though they have increased over the last quarter, they remain low relative to pre-pandemic levels. We expect vacancy rates to rise further in 2023 due to the various headwinds facing occupiers. However, we are starting from a low base, and the uptick in vacancy is likely to be felt more in older, poor-quality facilities or weaker locations.

Strong demand for Grade-A facilities remains, with occupiers increasingly looking for higher quality, modern facilities equipped to enable them to fulfil their ESG goals, maximise their efficiencies, reduce running costs and enhance their operations in terms of automation and technology. On the other side of the equation, construction activity is decreasing. The bifurcation in demand and stymied supply will keep vacancy rates for grade-A facilities low and support rental growth.

A positive outlook for rental growth

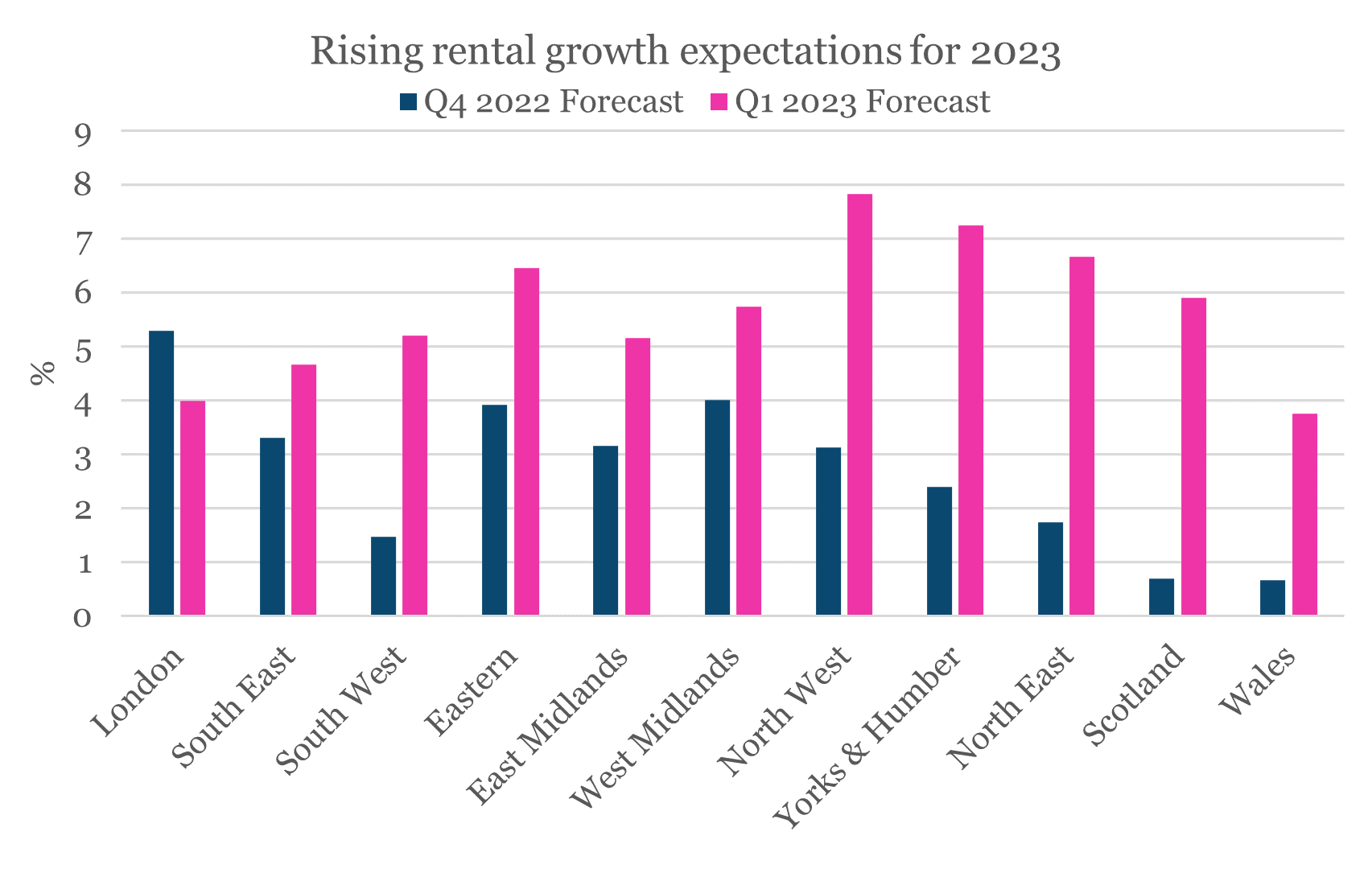

According to the Q1 2023 forecasts from RealFor, UK industrial rents are expected to increase by 5.1% this year. This represents a significant upward revision from their Q4 2022 forecasts, when 3.6% growth was anticipated in 2023. The North West and the Yorkshire and Humber regions are expected to perform best, with 7.8% and 7.2% growth forecast, respectively.

The rise in rental growth forecasts means that investors can anticipate improved income returns improving the viability of some developments. Our Knight Frank Industrial Land Values Model demonstrates that between Q3 2022 and Q1 2023, a significant number of locations have once again become viable for industrial development.

Source: RealFor

A third option?

Another option may be industrial open storage land or IOS. From a developer/investor perspective, these types of sites can be brought into use quickly (depending on planning) and cheaply and generate an income without significant investment or financing.

Demand for IOS has increased in recent years. The drive for intensification of industrial land has meant that logistics operators, particularly those active within the M25 or large urban centres, often face high site coverage ratios; in prime London sub-markets, site coverage ratios for new developments will typically exceed 60%. With minimal external space available for HGV movements, parking or electric vehicle charging onsite, operators are looking for offsite options to accommodate these needs.

IOS can accommodate additional fleet vehicles and enable operators to scale up operations without taking on additional facilities. Parcel carriers prefer to operate with low site densities (around 25-35%), and IOS can be used to store fleet vehicles offsite, enabling them to increase vehicle movements without increasing capacity at their warehouse. Operators can also use IOS to accommodate general storage and allow operators to scale up (or flex up) their operations rapidly.

If the location is suitable, IOS could be used as a distribution hub or help facilitate the consolidation of goods before bringing them into a city, with large trucks unloaded and goods moved on to vehicles suited for the last leg of the journey. With the UK government recently approving the use of longer HGVs on British roads, the demand for IOS as distribution hubs looks set to increase. These longer vehicles require additional yard space for manoeuvring, and their extra length may make them less suited for city roads. An increasing number of UK cities are introducing (or expanding) their Clean Air Zones (CAZs), which may drive demand for IOS.

From an investor perspective, this is a nascent but growing sub-sector in the UK’s industrial market, underpinned by strong occupier demand. It has been part of the US market industrial market for a while, growing significantly as an asset class following the GFC market downturn in 2007/2008, and now the UK market appears to be following suit. In July last year, UK fund manager Moorfield and Peloton Real Estate partnered to create a joint venture into the sector, targeting an initial £100m portfolio and has recently added a £26 million portfolio of four sites currently leased to BCA (car auctions), the sale price reflects a 13.1% net initial yield.

IOS boasts anti-cyclical qualities which could stand investors in good stead, should the UK economy weaken. As a (typically) cheaper option compared with traditional storage, IOS could appeal to cost-conscious occupiers needing to flex their operations up or down.

The growth in occupier demand for this type of space comes from various users; it requires little capital expenditure and can generate an income while also giving the option for future development. Depending on the location (and planning), IOS may make an attractive third option for those uncertain about committing to development.