Curation Over Cookie-Cutting: Re-inventing London’s Retail Floorspace

Relevance – the generic override to any successful retail location. The watchword for the pipeline retail developments across the capital.

2 minutes to read

A limited development pipeline

‘Build it and they will come’. ‘Clone Town Britain’. Two of the old mantras of retail that have hopefully been well and truly consigned to history.

This is hugely significant in that these two mantras defined the agenda for retail development throughout the 1990s and 2000s. And for retail development, read retail over-development. Too much retail floorspace was developed, not enough of which had its own, clear identity and purpose. Fast-forward to now and we have a clear situation of an over-supply of underwhelming retail space.

Given this situation and retail’s relative fall from grace in the real estate hierarchy generally, the retail development pipeline is understandably constrained, both in London and across the country. Why build more space if there is too much already?

The retail development pipeline may have slowed to a trickle, but there is still several retail schemes in the offing, particularly in the capital. Very different from each other. And very different from what went before.

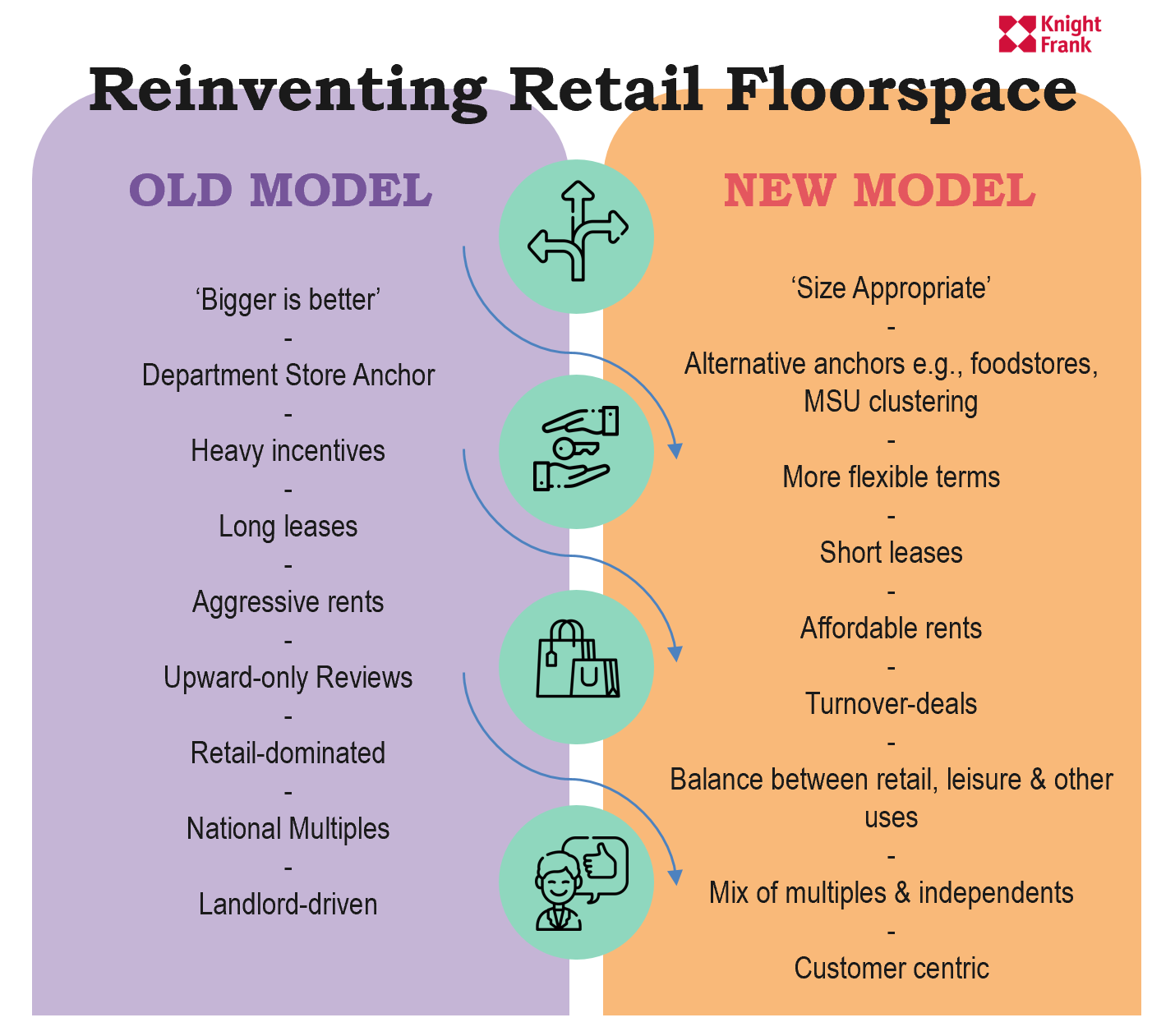

Out with the old…

The established shopping centre model no longer applies to new retail space. Bigger is not always better, excess space will not necessarily let up and will probably be vacant longer term. Department stores are not necessarily the reliable anchor they once were. On the one hand, the list of credible department store operators has diminished (c.f. Debenhams and House of Fraser). On the other, those that are still active in the market are far more selective as to what space they take.

Without the assurance of a major anchor store, MSUs and other tenants may take far more persuading. And they are far less likely to pay top-dollar rents in a vain chase for space. And generous incentives such as long rent-free periods, pin money and fit-out contributions may no longer cut the mustard either. Instead, retailers are far more risk-averse and nowadays affordability is paramount. Rather than long leases with upward only reviews, retailers are much more likely to push for shorter terms and de-risked deals, such as turnover rents.

Nor is the potential occupier base as ‘standardised’ as it used to be. Many of the ‘usual suspect’ tenants are no longer with us and the new breed of would-be occupier is far more diversified – a positive in terms of space curation, but often a negative in terms of covenant strength.

The old model is dead – and new ones are only just starting to emerge. But are they ‘models’ at all or bespoke solutions?

…in with the new

One thing is certain: the cookie-cutter approach no longer applies. And there is no ‘one size fits all’ blueprint for successful retail development, no ‘model’ as such.

What can we learn from a review of recent and forthcoming new retail developments in London?

Our first case study looks at Battersea Power Station.