Living Sector Gaining Traction given its Counter-Cyclical Nature

We take a look at this lesser-known sector and what it means for Asia-Pacific and its investors in 2023.

2 minutes to read

According to a survey conducted during Knight Frank’s Active Capital launch webinar in October 2022, almost half of the 600 respondents (see Figure 1) selected the living sector as one of the top three sectors they will be targeting in 2023 and are keen to take advantage of the sector’s structural changes.

Active Capital webinar live poll results

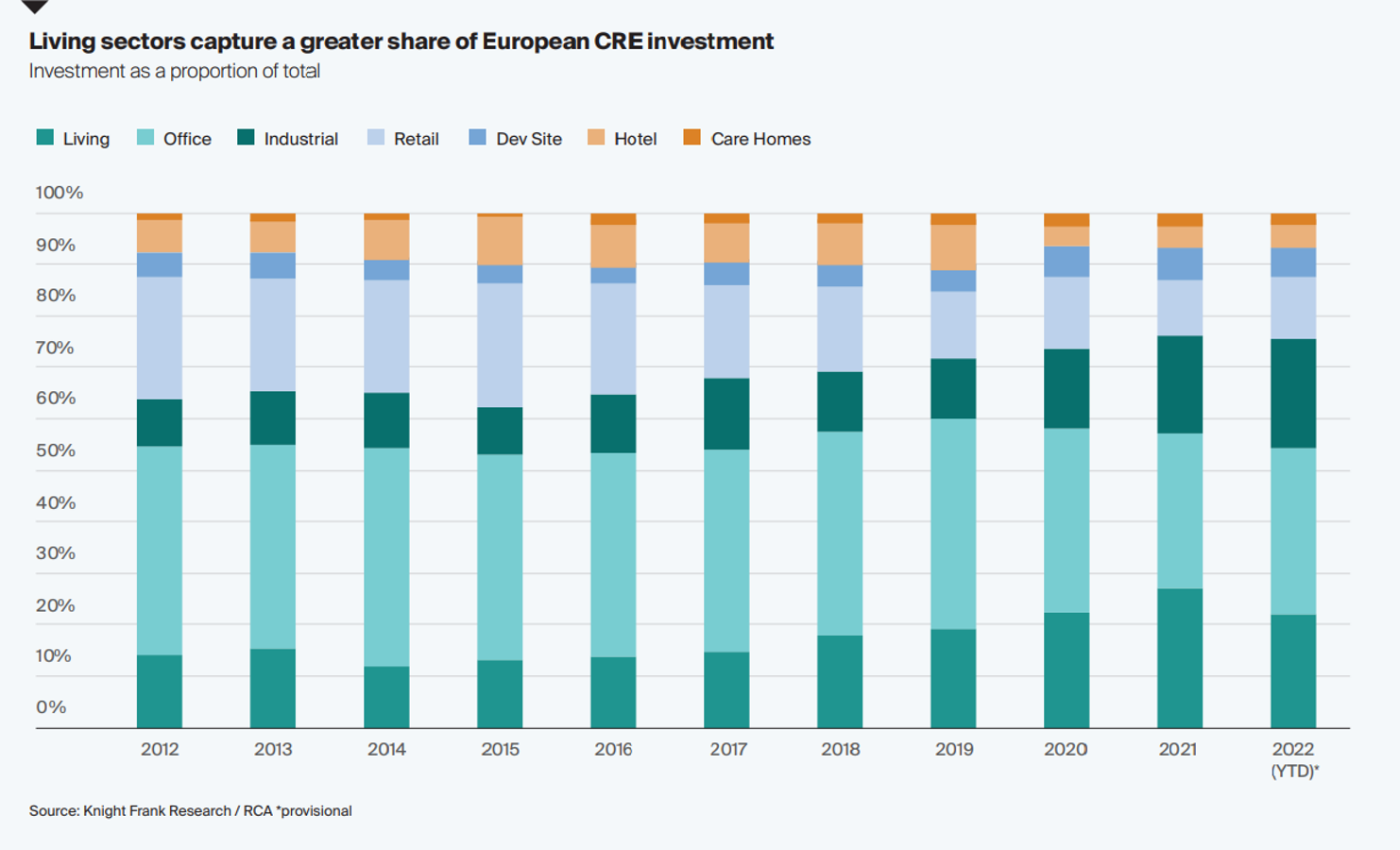

Although a non-traditional class of corporate real estate (CRE) due to demographic changes and lifestyle needs, this sector has been at the centre of attention in recent years as seen by the tremendous growth in its share of European CRE investment volume over the past ten years. It has also garnered the interest of international investors, particularly the Asia-Pacific investors, as cross-border investments into Living accounted for about 53% in 2022.

European Living Sectors Investor Survey

This sector has proven to be highly defensive in a downturn. For instance, with more people returning to universities to get re-skilled, it has rendered the student property subsector to benefit from countercyclical demand profiles. As the UK and some parts of Europe are home to world-class universities, they have been commanding the majority of the investment interest when it comes to student property, as shown by the European Living Sectors Investor Survey – 2022/23 report findings. Despite so, student property is still a relatively newer asset class, with demand outpacing supply which in turn causes stiff competition and pushing prices up.

Top 5 locations for investment

Over in Asia-Pacific, there is much room to catch up in terms of fundamentals. There is a structural demand-supply imbalance due to the construction delays as a result of the pandemic, coupled with the lack of such products in the market. As such, the returns have surprised on the upside, particularly when the re-opening of the economy kickstarted the return-to-campus trend that we have seen the uptick in terms of occupancies and pricing.

Being a nascent sector, supply and quality cannot match up to that of Europe and the UK, but the region is starting to see more of this alternative asset class, especially in Japan.

The East Asian nation leads the region in investment into the Living sector, particularly its well-established multi-family and senior living assets. With the yen weakening to a 30-year low and interest rates being largely stable, it is a good window of opportunity for cross-border investors to add a few Japanese Living sector assets to their portfolios. Yields for the sector have also shown to be resilient relative to that of other asset classes.

___

The Asia-Pacific Outlook Report is an annual publication that delves into the repercussions of the pandemic, increasing interest rates, and rising mortgage rates on the Asia-Pacific residential landscape using official statistics and outlines the forecast for 2023.

For more insights, please download the full report here.