New starts nosedive but will 2024 brighten by spring?

Plus, predictions across development and living sectors

6 minutes to read

News this week that new build starts across England plunged in the third quarter of 2023 should not come as a surprise. Back then, the government had only just paused its interest rate hiking cycle in September for the first time since December 2021, and annual inflation was still hovering above 6%.

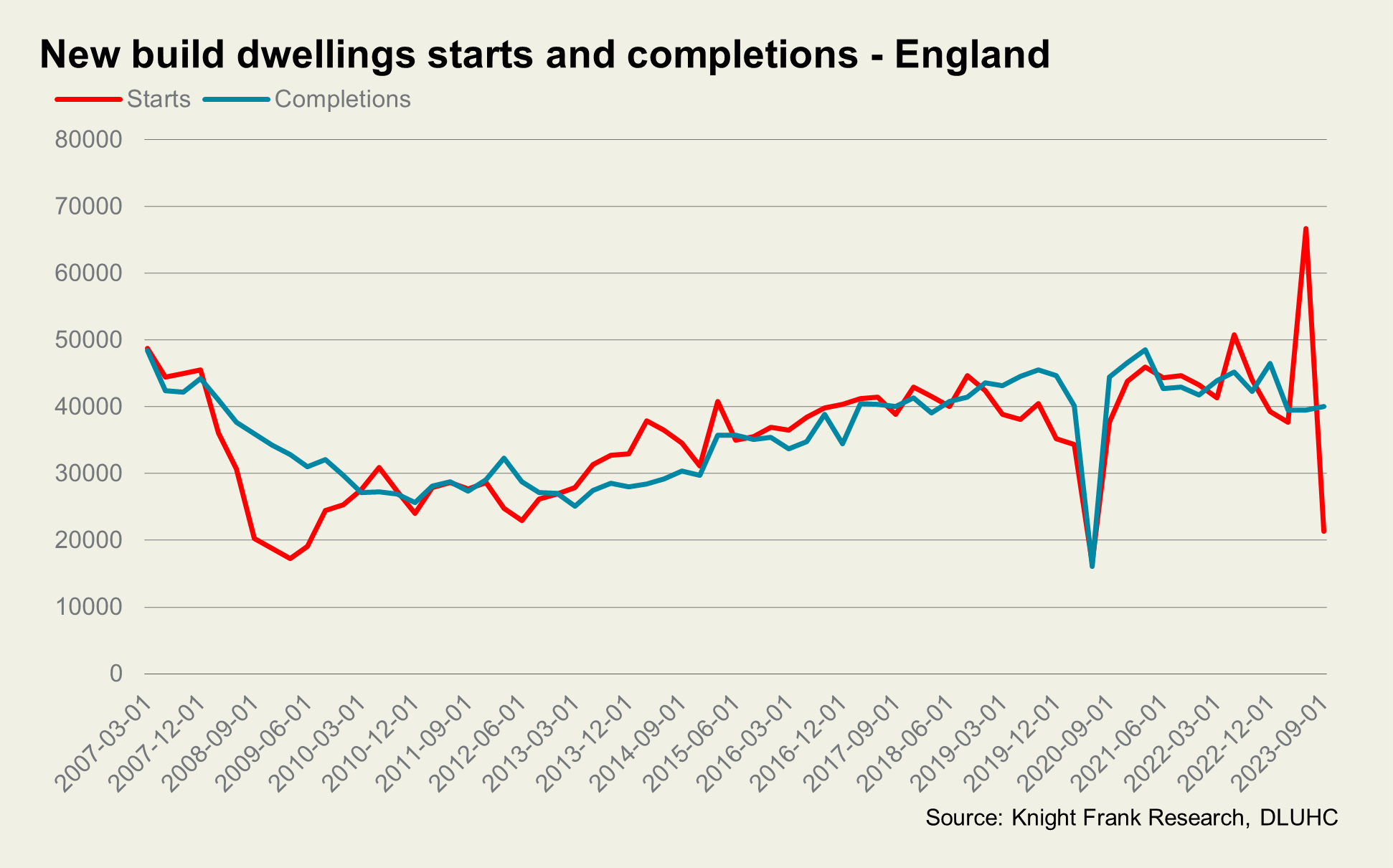

Housing starts fell by 68% in Q3 last year compared to the previous quarter to 21,300 – the lowest level since the Covid market shutdown in spring 2020 and close to the sluggish volumes seen in 2008-09 (see graph). The quarterly decline came after an artificial surge in starts in Q2 2023, when units jumped ahead of new environmental regulations. But starts were also down 52% compared to the same quarter of 2022, reflecting the more challenging development landscape of late 2023.

Whilst sentiment has become more positive since the start of the new year, these latest statistics provide yet greater evidence that the next government needs to accelerate the delivery of new homes.

So, aside from a general election, what else is in store for developers in 2024? Our team of analysts at Knight Frank have answers for you across new homes, land, planning, build-to-rent, student, and seniors housing below…

Development land and new homes – Anna Ward

Wish An increase in development and regeneration in urban centres where currently some schemes are stalling due to viability issues and planning approval delays.

Prediction Build cost pressures, affordable housing quotas, energy efficiency targets and dual staircase requirements will continue to squeeze land values. But key market dynamics are shifting into more positive territory which should lead to improved conditions by the spring. Housebuilder sales rates are picking up, the pace of build cost growth has slowed significantly, and the double digit falls in our Knight Frank land index have bottomed out. Plus, UK house prices are already stabilising, mortgage rates have come down, and there could be some relief in the form of first-time buyer incentives in the March Budget.

Advice Despite the uncertainty surrounding election timing, 2024 should be a much better year for the industry. Interest rates are levelling off and build costs have already eased, so there are opportunities for forward-thinking developers to build now and sell in a few years into a market starved of stock. De-risking across large scale projects through block sales to investors and operators in build-to-rent, student and seniors housing will be key.

Anna is an associate in our residential research team

Build to rent – Lizzie Breckner

Wish Single-family housing saw huge levels of investment in 2023, accounting for 40% of total BTR investment. I hope that this will not be a flash in the pan, and that housebuilders will continue to see the benefit of SFH as part of a blended, diversified exit strategy, even once the new homes market starts to improve along with falling mortgage rates.

Prediction A bumper Q4 for BTR investment and an improving macroeconomic backdrop will lead to a strong BTR investment market in 2024. Those who have been ‘waiting in the wings’ are becoming active again and there will be increased competition for limited investment opportunities. Plus, more stabilised stock will transact.

Advice Yields look more attractive and interest rates are coming in, so 2024 will be a year of buying opportunities. Developers will need to be focused on designing efficient purpose designed schemes to improve viability, given build costs. That, and more sophisticated deal structuring, is going to help to make the schemes work.

Lizzie is an associate in our living sectors research team

Planning – Stuart Baillie

Wish I would like to see local authorities being better resourced to help get things done on time. We need to get the basics right. This will require more of a steer from government and more certainty and clarity. Our quarterly survey of 50 volume and SME housebuilders demonstrates that planning is an ongoing major constraint.

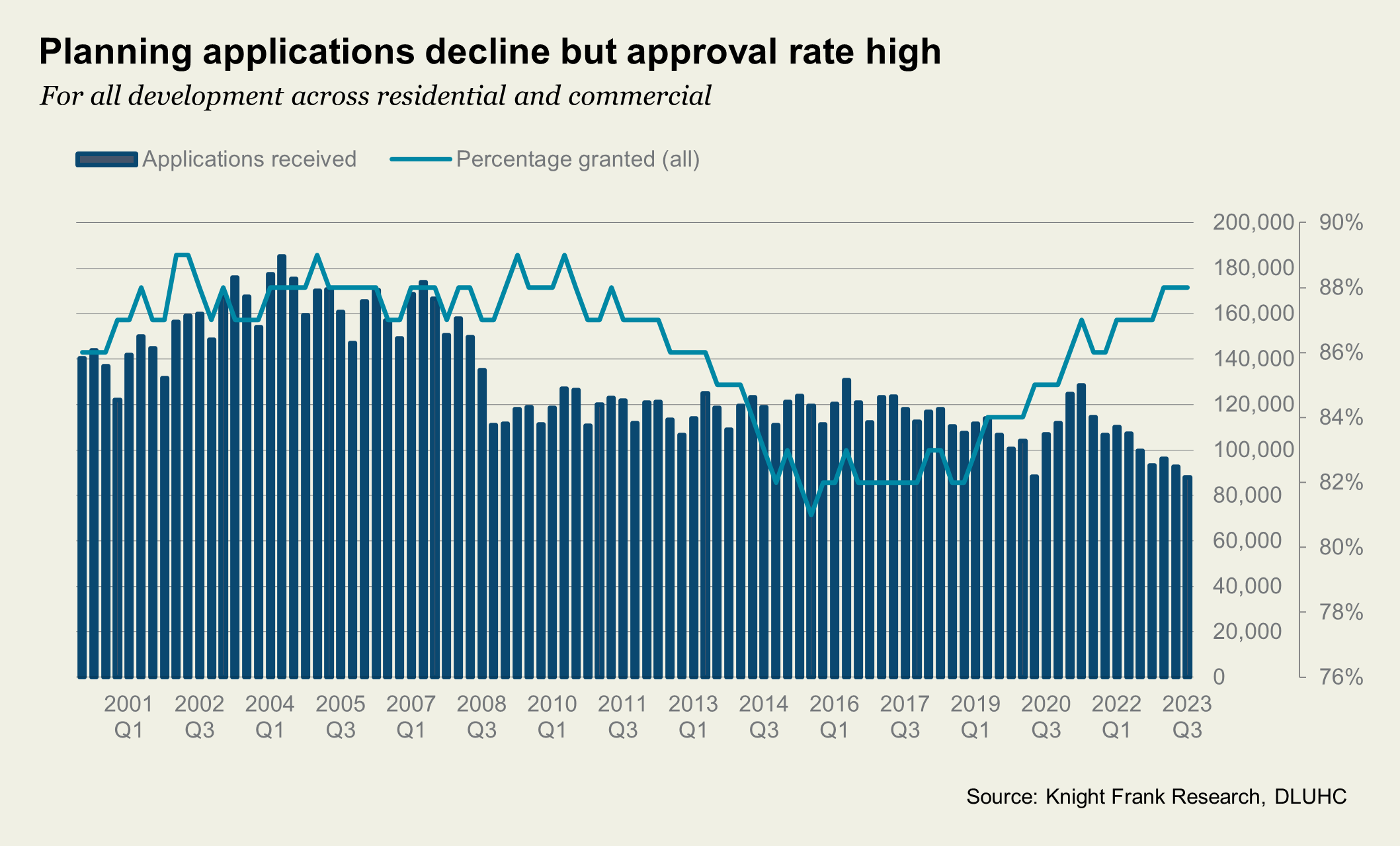

Prediction Housebuilding delivery will go down before it goes up…a drop off in application volumes and more schemes going to appeal with fewer local plans coming through means there will be a medium-term slump in delivery. There has been a sharp drop off in the volume of planning applications, yet the approval rate is still above 80% which shows perhaps that planning timeframes are more of a deterrent, particularly for SME developers with less deep pockets (see chart). Approvals are still common, but they take longer to get to.

Advice Don’t wait. Commit to the planning process, as cumbersome as it is. It is important to do the groundwork and be persistent because there isn’t going to be a fast-track solution agreed anytime soon. Any new government will soon realise that planning reforms are incredibly difficult to bring about.

Stuart is a partner and head of our UK planning team

Student (PBSA) – Katie O’Neill

Wish A better understanding from local councils of the benefits of PBSA in communities and crucially how it can help alleviate pressures on local housing markets.

Prediction The performance of PBSA as an asset class in 2024 will continue to be underpinned by the same theme: a structural imbalance between supply and demand for accommodation. Tricky to navigate planning policies, high construction costs, and a lack of available and suitable land plots all represent notable headwinds to maintaining or meaningfully increasing supply from current levels. The shortfall in much needed PBSA in our most popular university towns and cities will increase.

Advice Characterised by counter-cyclical performance, inflation hedging resilience and a lack of volatility, the advice to clients is to get involved. There is no silver bullet solution to the challenges the industry faces around delivery, but collaboration between the public and private sector will be essential to increasing supply. Higher Education Institutions are at the nexus: they hold planning data on the number, demographics, and residential requirements of projected intakes that enables conclusions to be drawn on future requirements. Insufficient or unsuitable accommodation constitutes a risk to their growth plans and to an institution’s reputation, and there is real opportunity for a more linked up public and private strategic approach.

Katie is an associate in our living sectors research team

Seniors housing – Andrew Sandison and Sam Heffron

Wish We are in a window where management teams are collegiate re sharing data, knowledge, lessons learnt, etc. We hope this continues to facilitate the trend of increasing public release of volume high-quality data, particularly around the inflation tracked nature of income and operating costs. This will further support investment decisions and accelerate the number of transactions.

Prediction We are forecasting 2024 investment volumes to outperform last year. This year will be a recovery year of sorts. The heady mix of forecasted deflation, interest rate cuts, improved HPI outlook, stable build costs, falling utilities costs, lower mortgage costs and higher availability of mortgages, all provides a more positive backdrop than last year. Icing on the cake would include a helpful outcome of the government’s Older Peoples Housing Taskforce, a further income tax cut in the next budget and other economic incentives pre-election, and more widely, democracy winning in the USA election and ongoing growth in China’s economy.

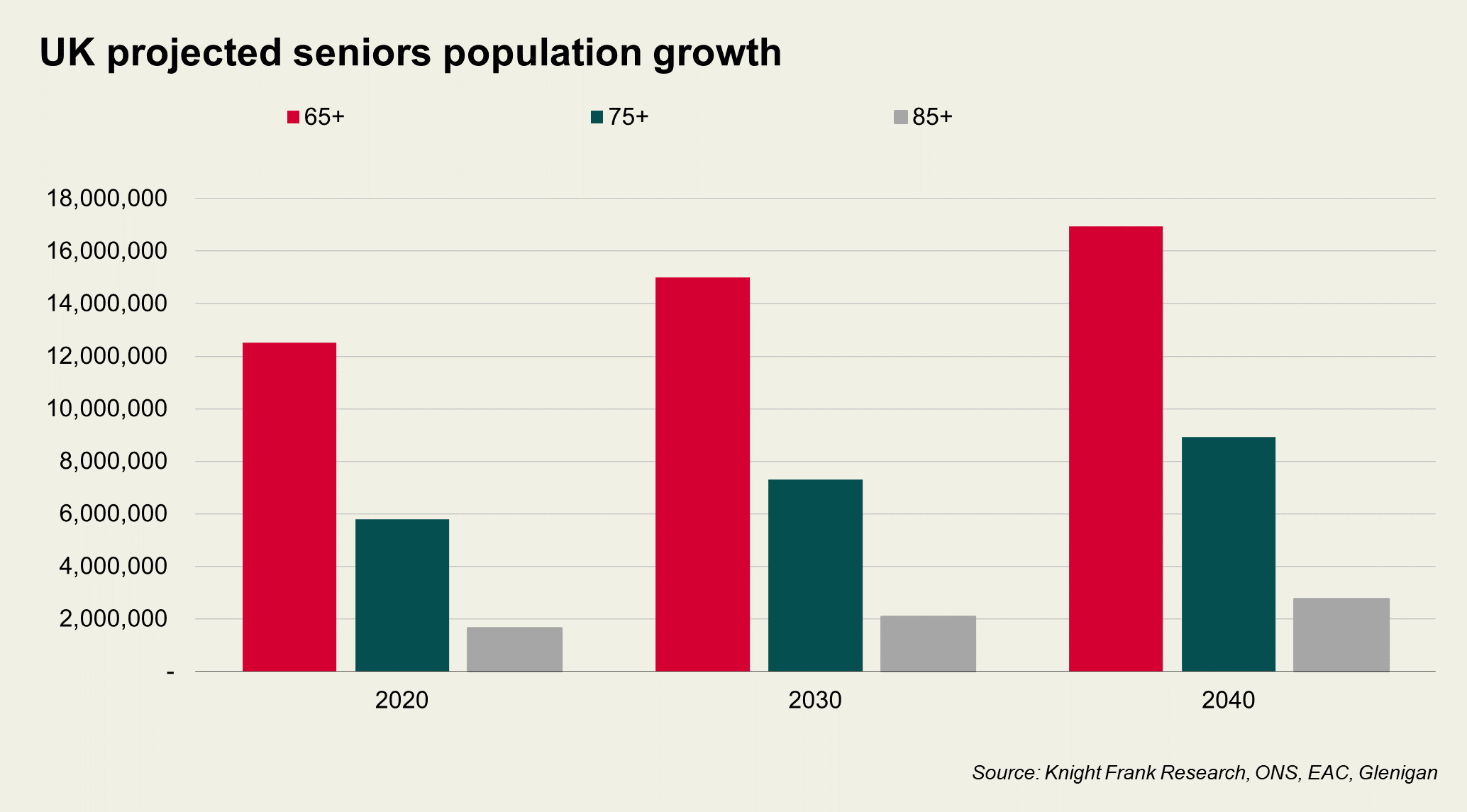

Advice Real values are currently down, and leverage is accretive (just) and will be diluted as values come back. Those investing today can capitalise on more favourable valuations before inflation abates and tailwinds accelerate. Durable growth is underpinned by fundamentals of an aging population, chronic undersupply, and limited competition. When combined with defensive cash flow traits, seniors housing offers a truly unique value proposition for property investors seeking alternatives to traditional strategies.

Andrew and Sam are senior analysts in our living sectors research team