Stubborn inflation means subdued Autumn for UK housing market

Next spring may produce a seasonal bounce in activity if inflation appears tamed.

2 minutes to read

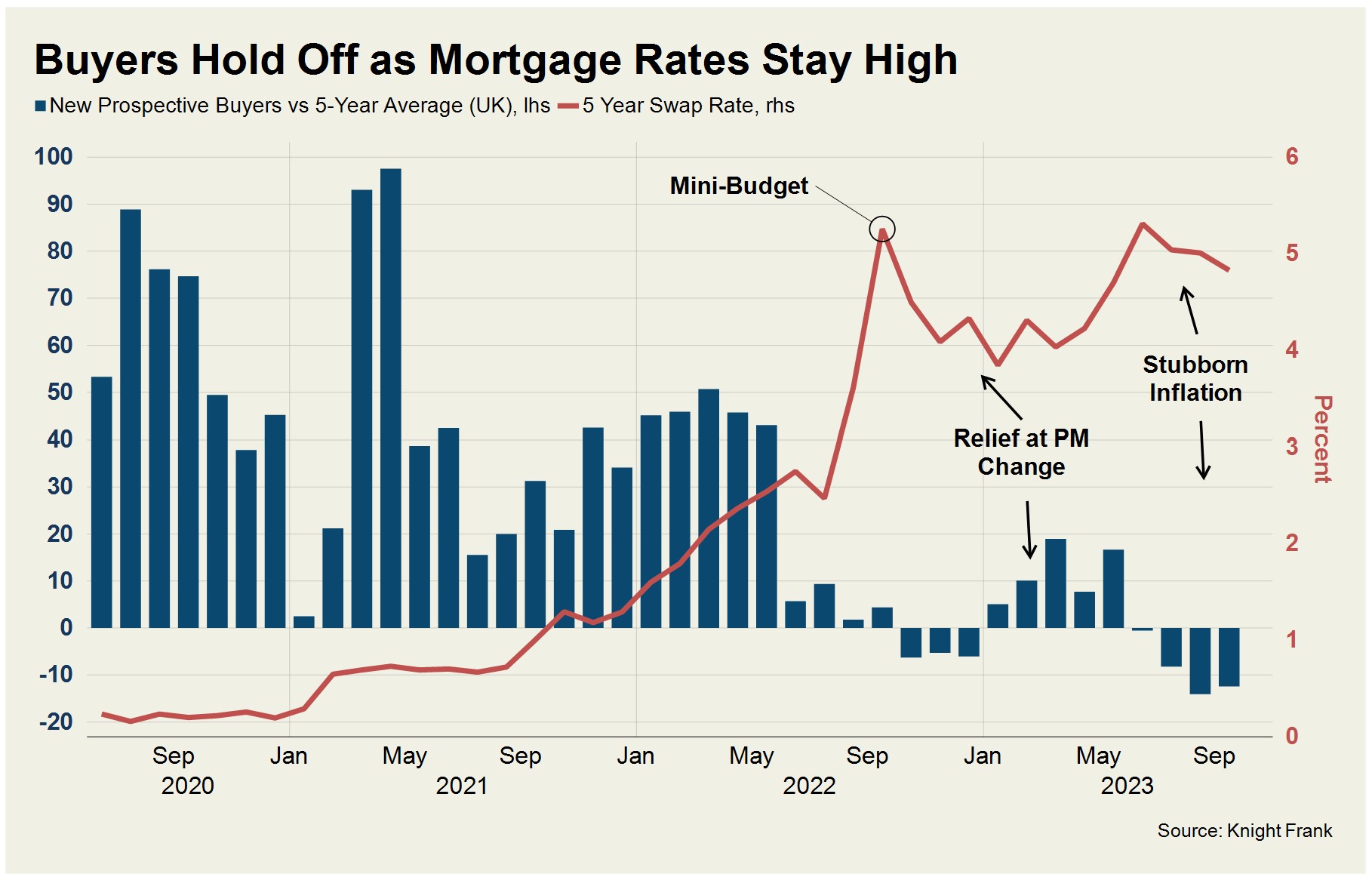

The seasonal autumn bounce has failed to materialise in the UK housing market this year.

It was a similar story last year, with one major difference: in 2022 there was a quick fix.

Last September, borrowing costs spiked when financial markets took fright at Liz Truss’s low-tax mini-Budget.

The Tories switched leader, rates came down and the housing market ticked over in the first half of this year.

Activity levels are once again muted in the final months of this year, but replacing the Prime Minister won’t help this time.

Stubbornly-high inflation is the prosaic cause of the problems currently facing the property market.

Transaction volumes were 14% below the five-year average in August, according to HMRC data, and mortgage approvals were down by a third. Prices have held up better as supply and demand have both dipped and we expect a decline of 7% across the UK this year.

After an initial period of relief, when swap rates fell and demand strengthened, this summer’s flow of poor inflation data and the prospect of rates that will stay higher for longer has caused a second consecutive period of weak trading in the final few months of the year - see chart below.

Comments from Bank of England Governor Andrew Bailey have certainly been gloomy in recent weeks as he talks about the final mile being the toughest in his attempts to bring the cost-of-living pressures under control. The recent conflict in the Middle East could exacerbate the situation with an inflationary rise in the oil price.

In the UK, it is the strength of the Jobs market and wage growth that is driving underlying inflation. Ordinarily, a strong jobs market supports housing transactions, just not when it’s keeping mortgage costs so high.

What will fix the market this time?

Rishi Sunak’s departure may be closer following two poor by-election results last week, but more relief will only come once buyers and sellers accept that rates have settled at their new normal and house prices reflect that.

With the Bank of England fighting a prolonged battle with inflation, nobody is ready to announce “job done” quite yet.

However, after 14 consecutive rises followed by a pause last month, we must be in the endgame, which means next spring will be an important moment.

If inflation feels tamed and mortgage rates appear stable, the pent-up demand that must be currently building may produce a more normal seasonal pattern of activity.

Let’s just hope a general election is not weighing too heavily on people’s minds by then.

Subscribe for more

Get exclusive market analysis, news and data from our research team, straight to your inbox.

Subscribe here