Which global cities lead our prime residential price forecast for 2023 and 2024?

With the global economy in a state of flux, we’ve revisited our 26-city forecasts for 2023 and 2024.

3 minutes to read

Surging inflation and resulting interest rate hikes have dominated the headlines in the first half of 2023. Mainstream markets have borne the brunt of the pain, but even here sales volumes, not prices, have been the greatest casualty to date.

Prime residential markets are better insulated to the changing monetary policy environment given the sector’s higher proportion of cash purchasers, 46% according to the latest survey of Knight Frank’s global research network, but they’re not immune.

We last took the pulse of prime city markets in December 2022. Much has changed since then. New Zealand has seen four additional rate rises taking their tally to 12 hikes, Canada has introduced a ban on foreign buyers, Los Angeles’s Mansion Tax is up and running and Singapore has ramped up stamp duty for non-residents from 30% to 60%.

It seemed an opportune time therefore to ask our global research teams to dust off their crystal balls and provide us with their take on the risks and opportunities facing their luxury housing markets and crucially, where they think prices are headed.

Which cities lead the forecast for 2023?

Of the 26 cities tracked, Dubai still leads the rankings for 2023, although annual growth is expected to cool to a less frothy 14%, down from 44% last year.

Surprisingly, 20 of the 26 cities still expect to see flat or positive price growth in 2023.

Tokyo, Paris, Madrid and Miami, all forecast to see 4% growth in 2023, complete the top five.

In Tokyo, persistently low interest rates and strengthening overseas interest explain the positivity, in Miami, low taxes, relative value and Latin demand are the key factors. Whilst for Paris and Madrid a lack of prime stock is cushioning prices.

Optimism…for now

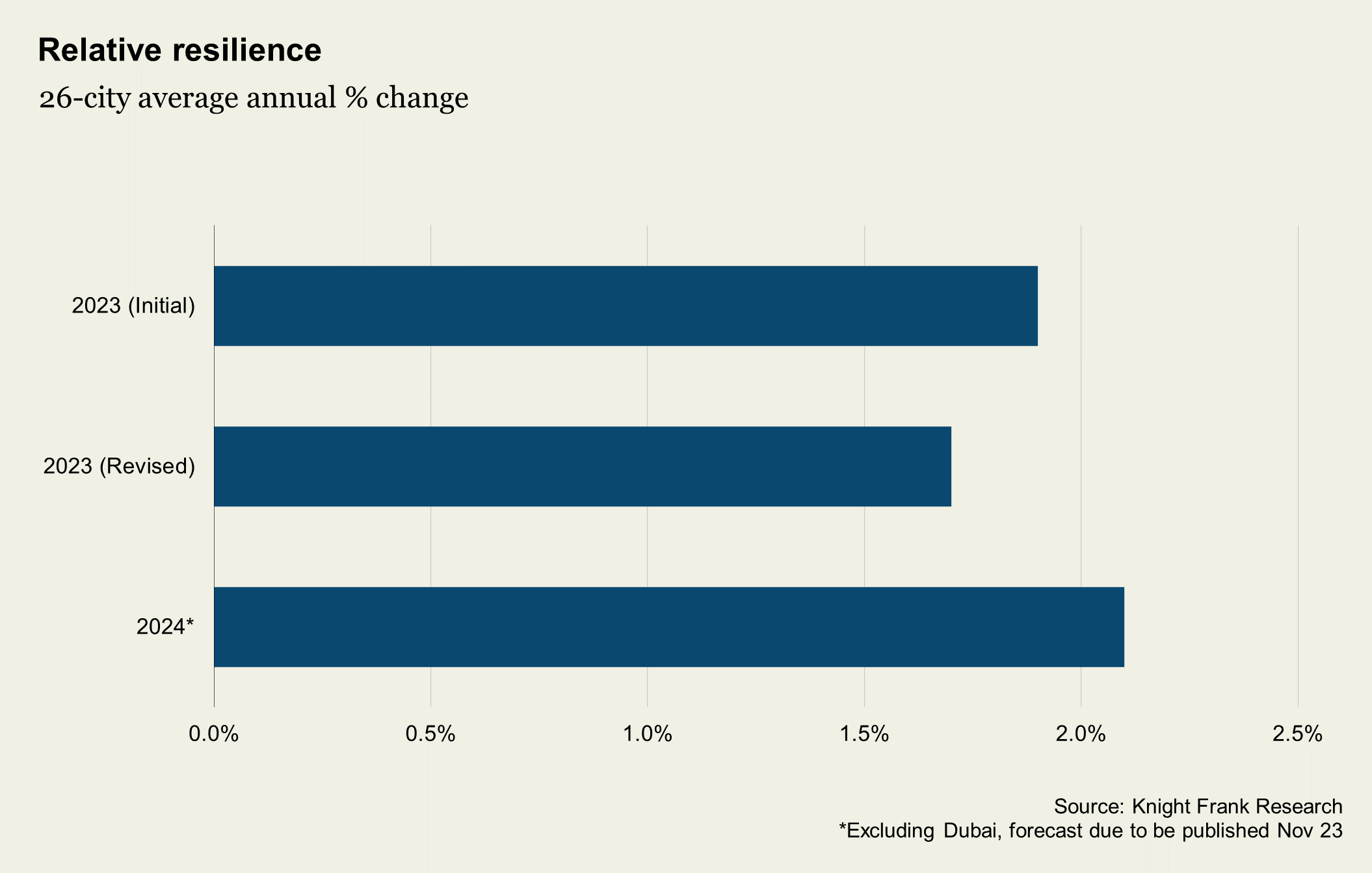

Despite an end to the era of cheap finance, a surging cost of living and the IMF’s downbeat forecast that “advanced economies will struggle to exceed GDP growth of 1.4% by the end of 2024”, the overall forecast has dipped only marginally, from 1.9% to 1.7%, between December 2022 and July 2023.

I asked Christine Li, Knight Frank’s Head of Research in Asia-Pacific what she thinks is behind this positivity. Christine explains, “Firstly, real estate assets appeal in times of uncertainty and high inflation given they allow for diversification and act as an inflation hedge. Secondly, in some parts of the region, such as in New Zealand, there is a growing perception that policymakers are about to pivot, and sales volumes are strengthening given the market still offers firm fundamentals.”

How has the prime price forecast changed?

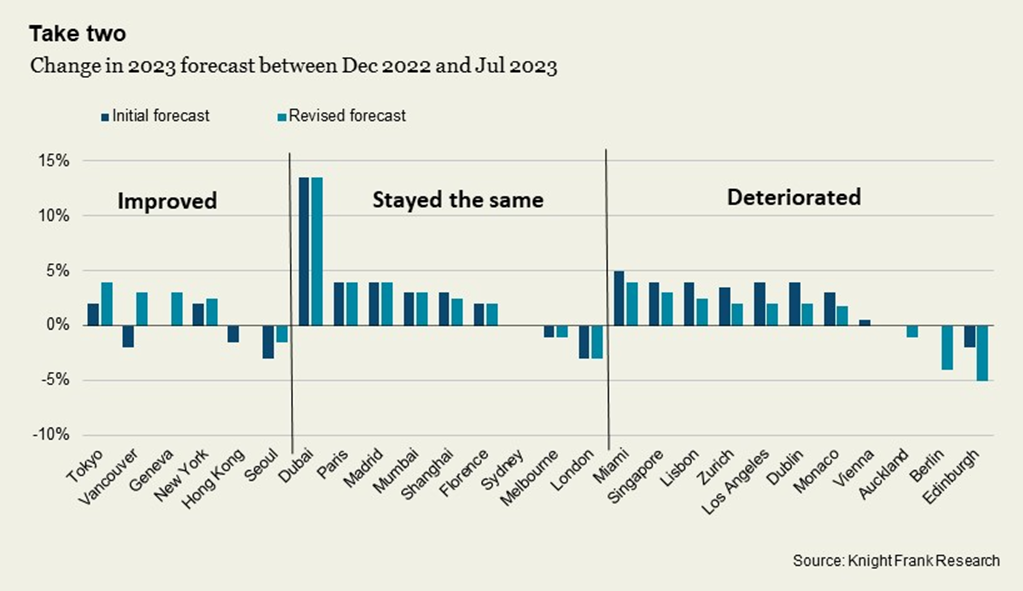

Of the 26 cities tracked, six cities are expected to see stronger performance than that predicted six months ago, nine have remained the same and the remaining eleven expect weaker growth.

Forecasts for Geneva and Vancouver have improved the most in percentage point terms, whilst Berlin, Edinburgh, Dublin, Los Angeles, Zurich and Lisbonn have deteriorated the most, albeit the declines remain relatively small at between 2% and 4%.

What’s the outlook for 2024?

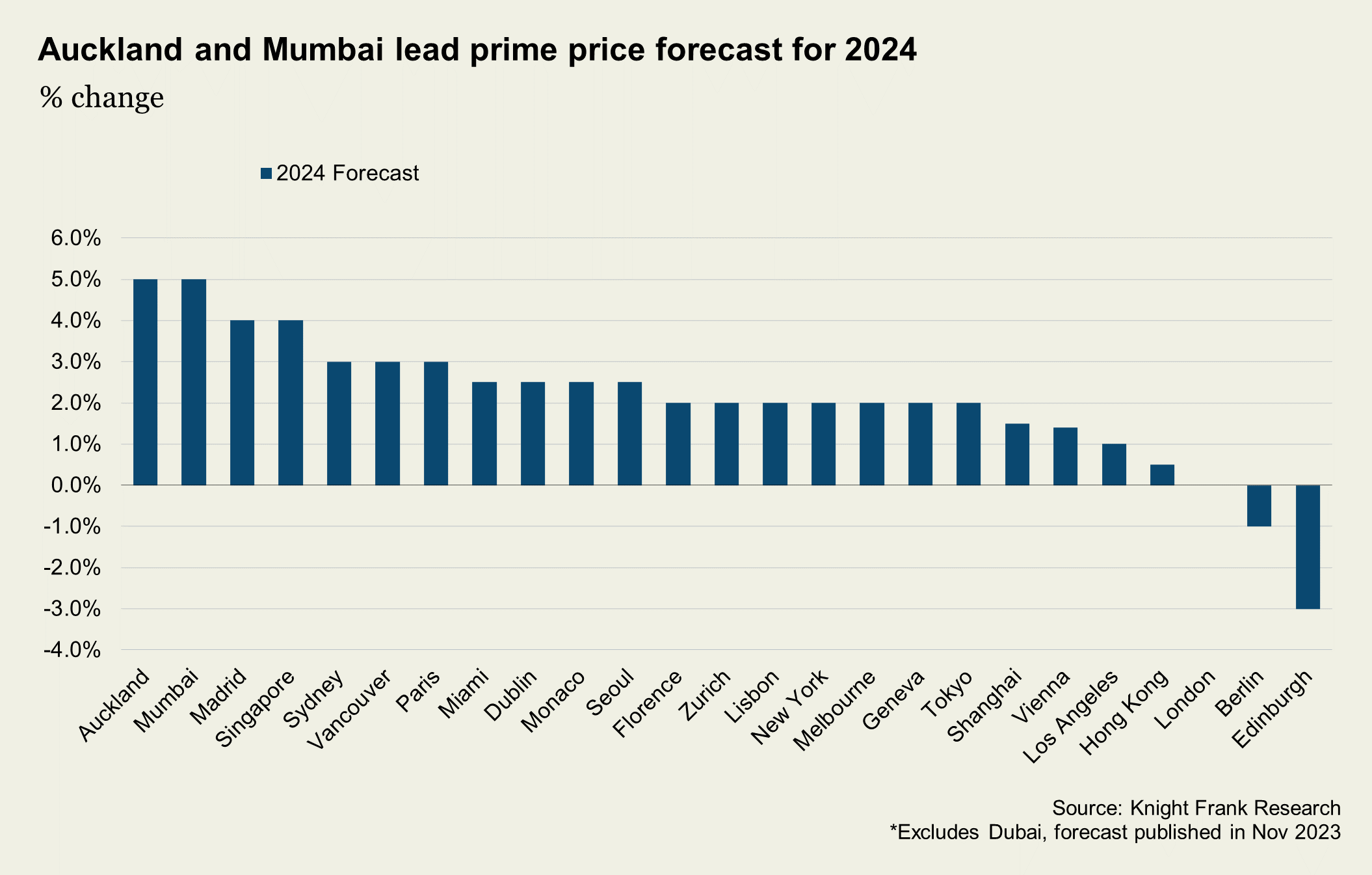

Prime prices are set to improve in 2024, averaging 2% growth, excluding Dubai.

Auckland and Mumbai lead the forecast for 2024, both tipped to see 5% growth over the 12-month period. Auckland is moving into recovery mode having seen prime prices dip 17% since their peak in Q3 2021.

Meanwhile, in Mumbai, improving GDP figures, the city’s relative value and investment in infrastructure will push prices higher, whilst in Singapore (4%) demand will continue to outpace supply.

Madrid (4%), Paris (3%) and Dublin (2.5%) are expected to be the top performers, lack of luxury stock and relative economic resilience behind the positive outlook.

Subscribe for more

To stay up to speed with our global residential forecasts, sign up to our monthly Global Residential newsletter and The Wealth Report series