Farmland price rise slows

Price growth is slowing, but farmland is still outperforming other asset classes

1 minute to read

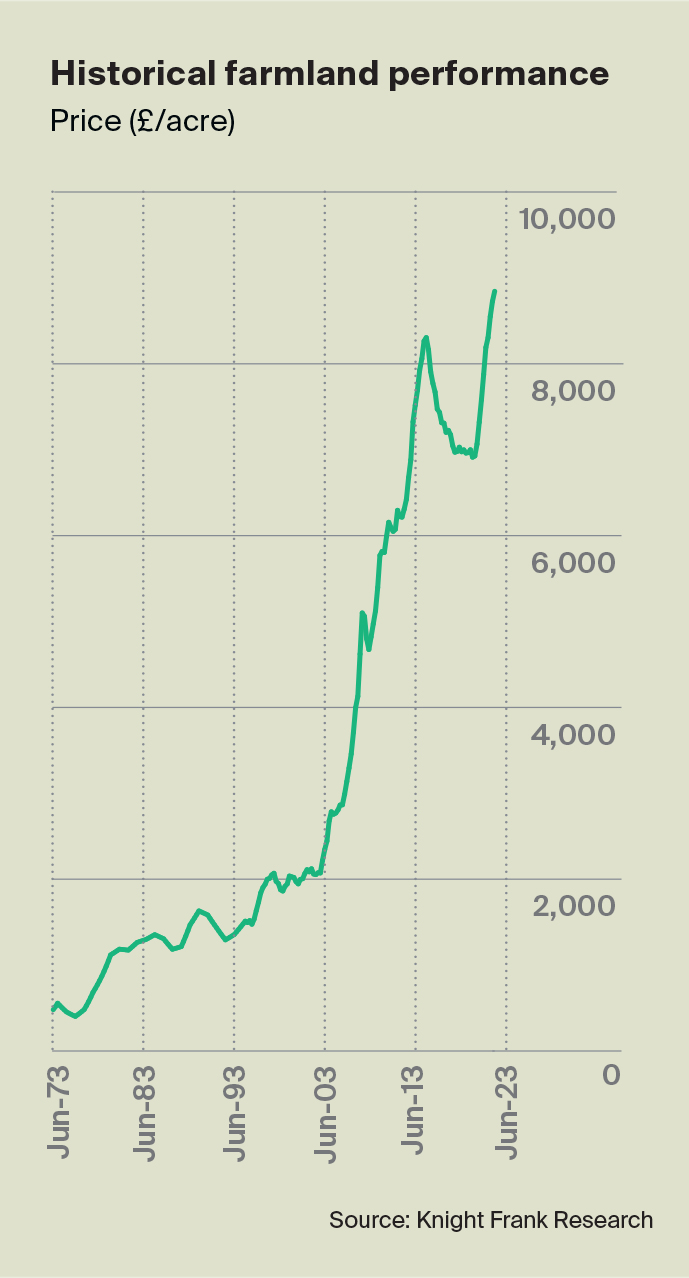

The average value of bare agricultural land in England and Wales rose during the second quarter of the year at the slowest rate since March 2021.

According to the Knight Frank Farmland Index, prices increased by just over 1% to £8,845/acre. Annual growth at 8% also slipped into single figures for the first time since the final three months of 2021.

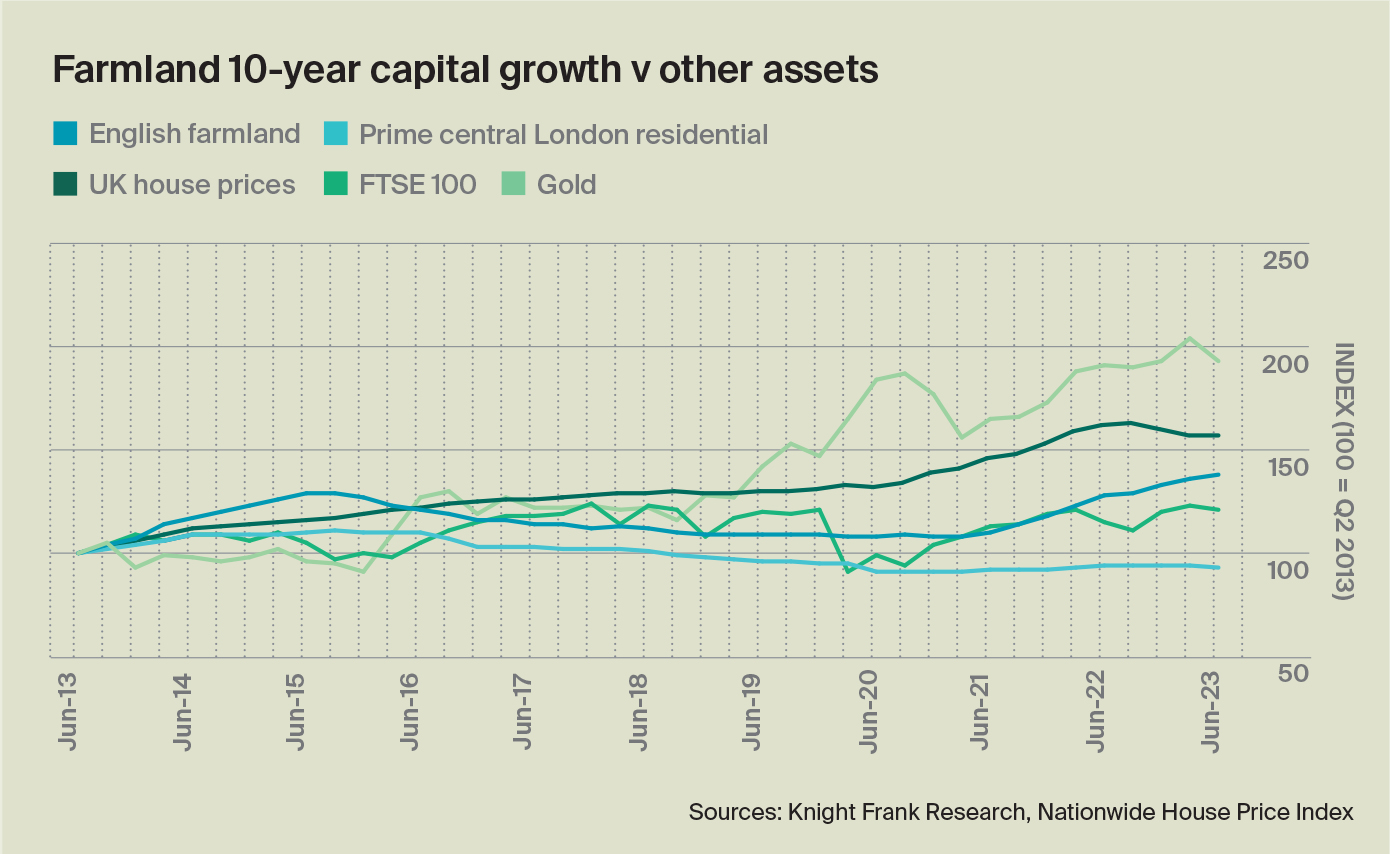

Farmland, however, has outperformed the FTSE 100 equities index, gold, prime central London houses and mainstream house prices over three and 12-month periods. Over five years, only gold has seen stronger capital appreciation.

After a period of surging growth – our farmland index has risen by 28% since the market troughed at the end of 2020 – a passage of more moderate performance was perhaps to be expected. Spiralling interest and inflation rates have also undoubtedly been playing on the minds of prospective buyers.

A rise in the availability of farmland for sale is also contributing. To the end of June almost 20% more land had been publicly advertised compared with the same period in 2022, according to the Farmers Weekly Land Tracker.

However, a total of almost 43,000 acres over six months is still very low historically.

Despite the increase in supply, there is still not enough land on the market to match regional demand across the country, especially in areas where residential and infrastructure development has led to a number of landowners with rollover funds to spend.

Environmentally minded potential buyers also remain in the market, although many are yet to actually purchase. The recent launch of the 9,486-acre Rothbury Estate in Northumberland (pictured), which has significant potential to deliver nature-based solutions, will be a very interesting test of the market due to the scale it offers potential investors.