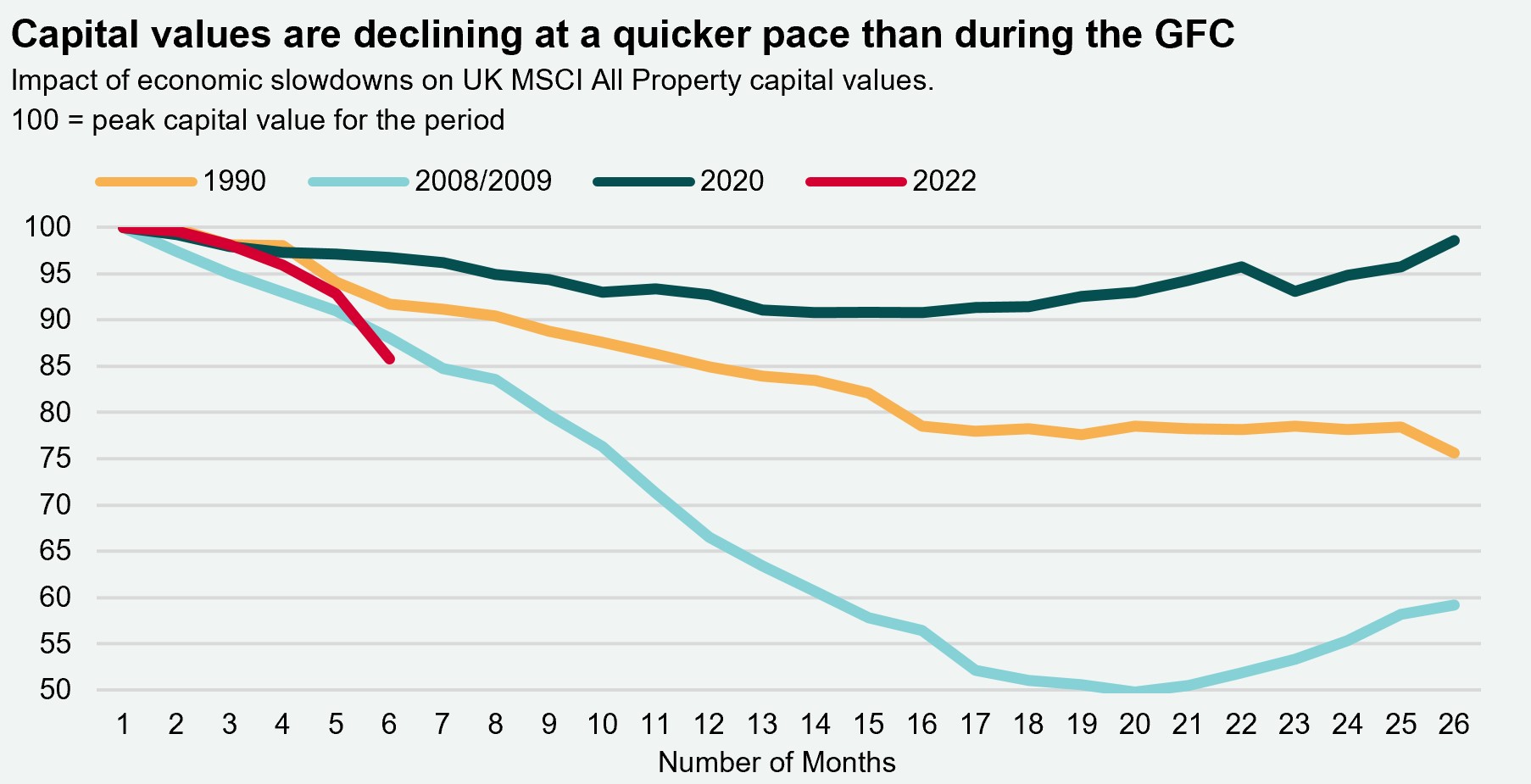

Your Leading Indicators | Autumn Statement | GDP | Unemployment

Discover key economic and financial metrics, and what to look out for in the week ahead.

2 minutes to read

Here we look at the leading indicators in the world of economics. Download the dashboard for in-depth analysis into commodities, trade, equities and more.

What can we expect from the ‘Autumn Statement’?

On Thursday, Jeremy Hunt, Chancellor of the Exchequer will outline the UK government’s fiscal plan for the economy. Hunt has already announced a plan to increase corporation tax to 25% by next April, but we will have to wait until Thursday to see his plan for business rates. The Chancellor is expected to announce c.£34bn in spending cuts, while raising taxes by approximately £20bn. Hunt is also expected to keep tax-free thresholds at the same level for inheritance, income, pensions and capital gains levies to increase taxes via ‘the back door’ due to high levels of inflation. Markets have largely already priced in the ‘Autumn Statement’, as Hunt will likely exercise fiscal discipline now that the risk premium from the previous budget has largely been reversed.

What will the impact be on GDP?

Fiscal tightening in the ‘Autumn Statement’ could cause a deeper and longer downturn. Currently, Oxford Economics expect a 1.0% peak-to-trough fall in UK GDP, while Capital Economics forecast a 2.0% contraction. However, both expect a deeper peak-to-trough fall in GDP and a slower recovery if the expected £54bn in fiscal consolidation comes to fruition on Thursday. This poses a problem, as every 1.0% fall in GDP growth increases borrowing by 0.7% of GDP. Therefore, a weaker economy creates a larger fiscal hole for the Chancellor. However, tighter fiscal policy could mean the Bank of England tempers its rate hikes sooner than expected.

UK unemployment remains near 50-year lows but is no longer tightening

The UK unemployment rate was 3.6% in the three months to September, 0.2 percentage points (pps) lower q-q, however up by 0.1pps from 3.5% in the three months to August. The UK labour market remains tight, largely due to a smaller workforce. Indeed, 21.6% of the UK working age population was economically inactive in the three months to September, which is 1.4pps higher than it was pre-pandemic and up by 122k people between Q2 and Q3 2022. The ONS also outlined that more businesses are reporting holding back on recruitment because of economic pressures. September’s unemployment data therefore shows early signs that the labour market may be turning. However, economists still expect the Bank of England to hike rates at its meeting in December, but by 50bps instead of the 75bps rise it implemented earlier this month.

Download the latest dashboard