UK House Price Forecasts: January 2024

The outlook has become more positive over the last three months as interest rate expectations have changed markedly

5 minutes to read

In October, financial markets were pricing in a single interest rate cut of 0.25% by the end of 2024. At the end of last week, they were expecting five.

The main reason for this changing outlook is that inflation is falling faster than expected. As a result, mortgage lenders have dropped their rates fairly significantly in recent weeks, partly to win business in a low-volume market.

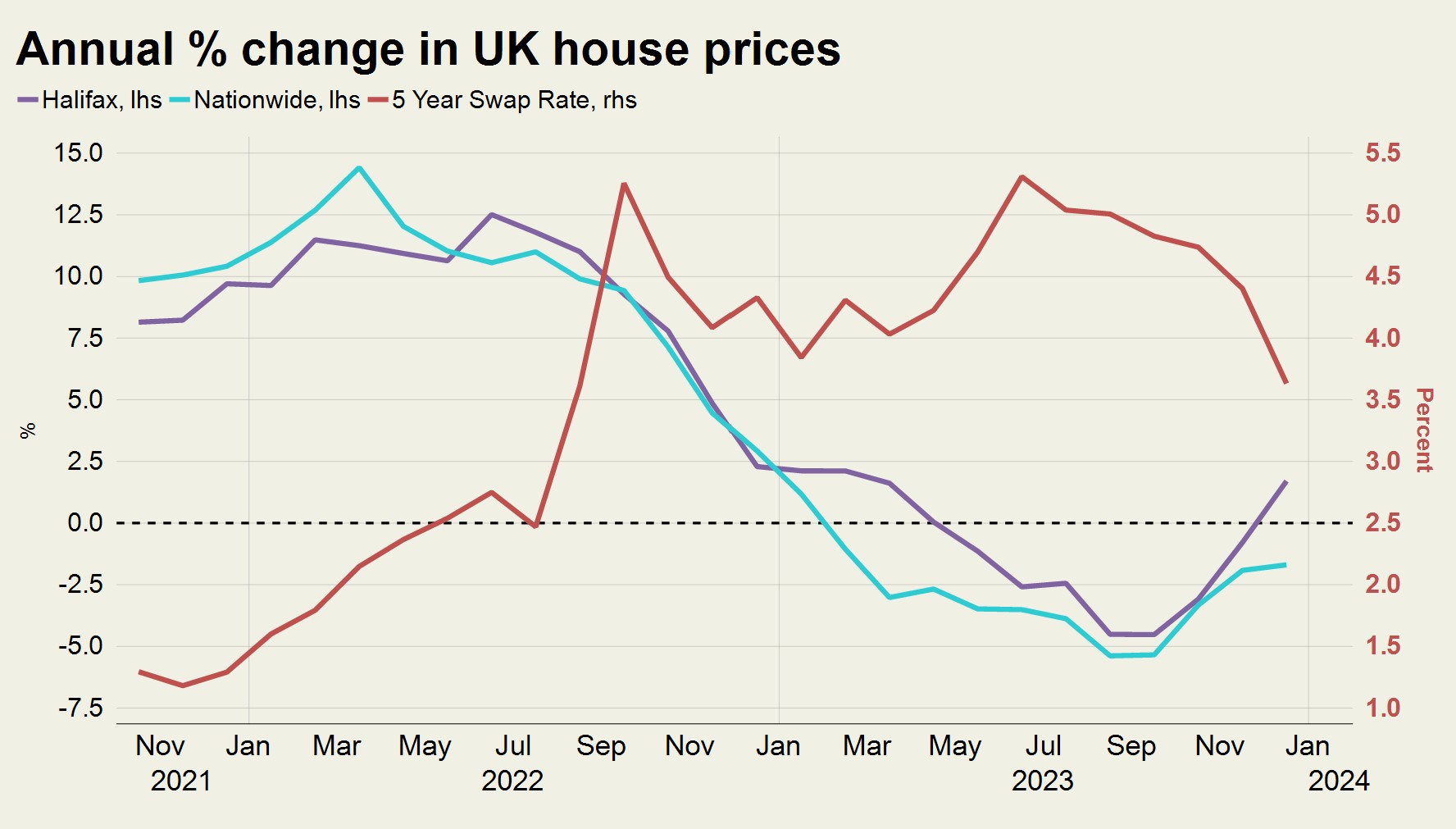

The best five-year fixed-rate mortgage is now under 4%, which was made possible after the five-year swap rate fell a full percentage point over the final quarter of 2023.

As a result of this more positive backdrop, we have revised our UK house price forecasts from three months ago.

UK Sales Forecasts

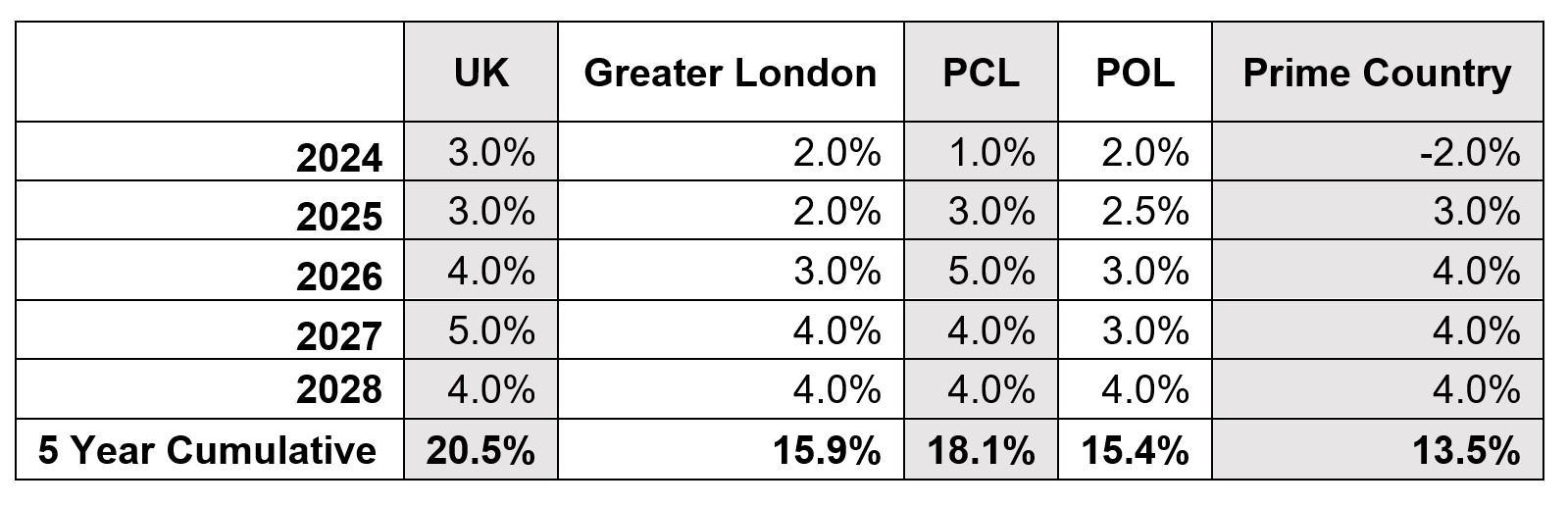

We now expect UK mainstream prices to rise by 3% in 2024, which compares to a decline of 4% predicted in October. With low-level single-digit growth in subsequent years, we expect cumulative growth of 20.5% in the five years to 2028.

Data from Halifax and Nationwide certainly suggests a corner is being turned. While the former reported a 1.7% increase in 2023 and the latter posted a fall of 1.8%, that compares to a 5% decline that both identified in August.

With UK housing transactions a fifth below their five-year average, we waited until a clear pattern emerged showing prices were bottoming out, which we believe is now the case – see chart below.

As a result of stronger demand, the number of mortgage approvals was 10% higher in November than the previous year and we expect a double-digit percentage increase in sales volumes this year compared to 2023.

We forecast slightly lower growth for the mainstream London market (+2%) this year as continued affordability constraints in the capital mean lower-value areas of the country are likely to outperform.

In the prime country house market, we now expect a narrower decline this year (-2%) as the market comes down from the highs of the pandemic in recent years. Realistic asking prices will remain important as the ‘race for space’ is no longer driving demand as it was during successive lockdowns.

We expect somewhat more positive growth in prime London markets, although they face greater risks as a result of the general election this year. We expect prime central London (PCL) and prime outer London (POL) to underperform the wider UK market this year.

Given that prices in PCL are still 17% lower than their last peak in mid-2015, we believe growth will kick in more fully from next year.

Forecasts relate to average prices in the existing homes market. New build prices may not move at the same rate.

The General Election

How long the current momentum in the housing market continues depends to some extent on when the general election takes place.

There is a risk that Rishi Sunak can’t fully control the timing if ideological splits within his own party on the issue of immigration grow wider, which adds an element of uncertainty. Speculation over the stability of the government is not good for sentiment in the housing market, as we saw in 2019 under former PM Theresa May.

The ongoing conflict in the Red Sea and the threat it potentially poses for higher UK inflation is another risk on the horizon.

On the plus side, activity could be boosted further by pre-election giveaways in the March Budget. There is speculation surrounding tax cuts as well as measures to help first-time buyers including longer fixed-term mortgages, smaller deposits, and a revived help-to-buy scheme.

A Labour victory appears the most likely outcome and while it has ruled out introducing rent controls or a wealth tax, other measures could dampen demand in prime property markets.

These proposals include overhauling the non-dom tax regime, increasing the 2% stamp duty surcharge for overseas buyers, adding VAT to school fees, and changing inheritance tax rules.

UK Rental Market Forecasts

Landlords have left the sector in recent years due to extra red tape and taxes, which has put strong upwards pressure on rental values. However, supply is recovering as demand is gradually being absorbed and more sellers have become landlords in a sales market where price growth has been minimal.

New listings in PCL and POL were only 7% below the five-year average in December, Rightmove data shows.

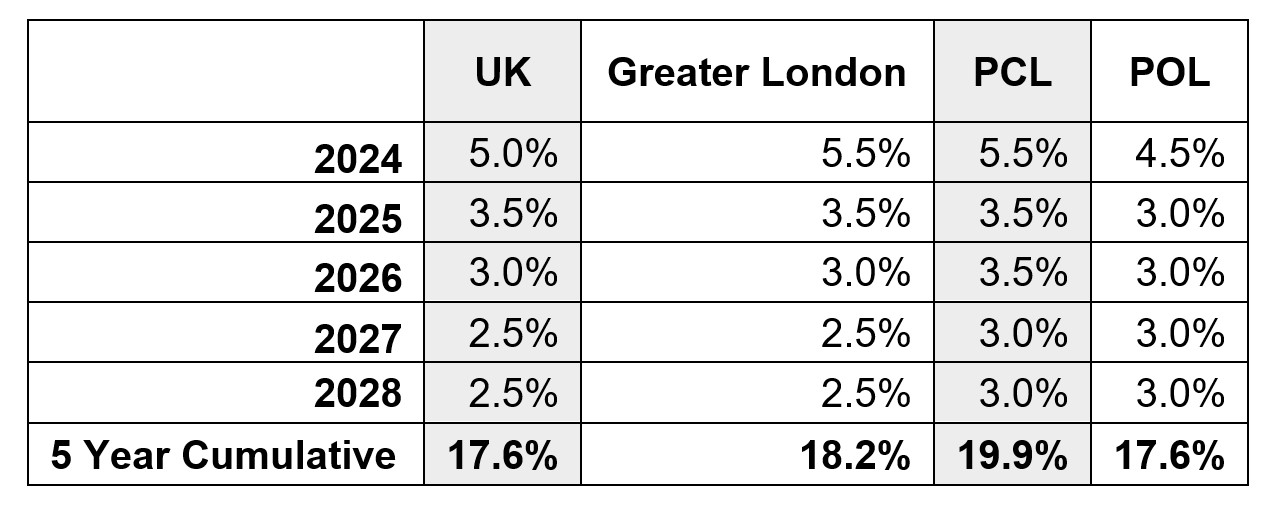

We have not altered our rental forecasts dramatically from October and forecast 5.5% rental value growth this year in PCL, which would be lower than the 8% registered in 2023. Meanwhile, we expect a 4.5% increase in POL, down from 6.8% in 2023.

Rental value growth should be stronger in lower-value markets as the supply/demand distortions are greater. Property owners are typically more discretionary in higher-value markets and have been able to let while price growth has been flat.

There were 4.3 new prospective tenants for every rental listing below £1,000 per week in PCL and POL in the final quarter of last year, Knight Frank data shows. Above £1,000 per week, the figure was 2.7.

That said, rising mortgage costs, taxes and red tape (including the Renters Reform Bill) should maintain upwards pressure on rents this year by keeping supply in check. And for context, our forecast of 5.5% in PCL this year was last beaten in 2011 if you ignore the distortive impact of the pandemic.

Across the UK, annual growth was 6.2% in November, according to the ONS, the highest rate since records began as the wider UK rental market grapples with the same supply-demand issues.

As these reduce gradually, we expect UK rental value growth to decline slightly to 5% this year, with a slightly higher figure of 6% in London, where demand is strongest.