UK house transactions, oil prices, and tax evasion

Making sense of the latest trends in property and economics from around the globe.

5 minutes to read

To receive this regular update straight to your inbox every Monday, Wednesday and Friday, subscribe here.

The Labour Party used its conference earlier this month to crown itself as the party of homeownership. We got pledges on everything from the return of 'new towns', and freeing up greenbelt land for development, to a recruitment drive in planning departments and a pledge to fast track infrastructure projects.

The Conservatives responded with a range of policy briefings to the weekend papers. Saturday's Times reported that senior Tories 'are discussing' whether to include a pledge to cut stamp duty as part of its election manifesto. The policy would be one of two "major pledges" that are on the table, the other being a promise to abolish inheritance tax.

The Sunday Times had details of a package of support to help first-time buyers that could be announced in the autumn statement next month. That package could include a 12-month extension to the 95% mortgage guarantee scheme that is due to end in December and a new type of Isa aimed at incentivising people to buy their first home - officials have floated lifting the current price cap from £450,000.

An extension of Help to Buy has now been ruled out. The Times reported back in May that a new iteration of the scheme was 'back on the table', but the Treasury is concerned that a revival would prove inflationary, according to the Sunday Times report. Polling by YouGov in Saturday's paper illustrates why the party views homeownership as such a key issue: while 45% of voters over the age of 65 support the party, this drops to 30% of those between 50 and 64. Only 12% of 25 to 49-year-olds say they will vote Conservative at the next election.

The autumn bounce

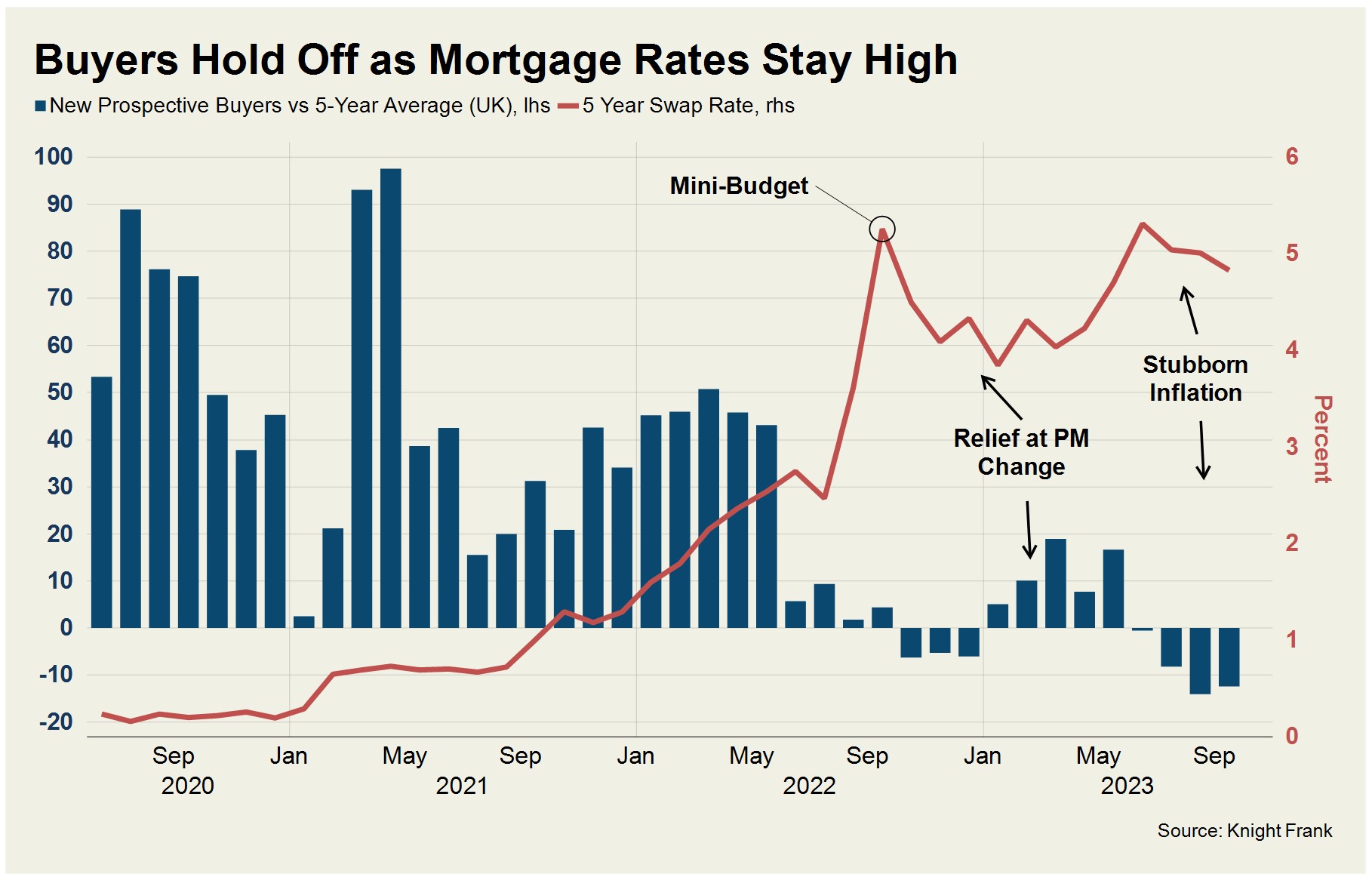

For the second year running, the traditional autumn pick up in housing market activity has failed to materialise.

Last autumn was dominated by the mini-budget, and there was a relatively quick fix. The Conservatives switched leader, mortgage rates eased and housing market activity started to recover - though only to a point. This year conditions are likely to remain muted, at least until spring, Tom Bill writes in his update this morning.

Transaction volumes were 14% below the five-year average in August, according to HMRC data. Mortgage approvals were down by a third. After an initial period of relief earlier this year, when swap rates fell and demand strengthened, this summer’s flow of poor inflation data and the prospect of rates that will stay higher for longer has caused a second consecutive period of weak trading in the final few months of the year - see chart below.

While the outlook for inflation has improved, the Bank of England is uncertain as to what it will take to cross the so-called 'last mile'. "Relief will only come once buyers and sellers accept that rates have settled at their new normal and house prices reflect that," Tom writes. "Next spring will be an important moment. If inflation feels tamed and mortgage rates appear stable, the pent-up demand that must be currently building may produce a more normal seasonal pattern of activity."

Oil prices

Fears that interest rates will remain higher for longer is driving yields on long-duration government bonds higher. I covered the US angle on Friday, but this is a broader trend - yields on 30-year British government bonds rose to their highest in more than 25 years on Friday.

Again, this is about what it's going to bring inflation through the last few percentage points back to target. The Hamas-Israel conflict and the prospect of a broader, regional war is likely to push oil prices higher, which will be inflationary, analysts say. Fluctuations in recent days have pushed international benchmark Brent crude as high as $96 a barrel, up from $85 before the conflict began on October 6th. Forecasts range from $100 to up to $140 in the case of an escalation, with the range reflecting the degree of uncertainty as to what happens next.

The European Central Bank's September inflation forecast — which predicts that consumer-price growth will slow to 2% in 2025 — is based on an estimate of an oil price of $82.7 per barrel this year, dropping to $77.9 in 2025.

Tax evasion

"In this world nothing is certain except death and taxes, Benjamin Franklin famously said. Billionaires may not yet have achieved immortality, but they have certainly become more agile at avoiding the taxman."

That was Nobel Prize-winning economist Joseph Stiglitz opening in a new report for the EU Tax Observatory, a think tank hosted at the Paris School of Economics.

The world is packed with think tanks making recommendations, but this is a relatively influential group and the recommendations chime with recent calls from populist politicians globally. The group lobbied for the introduction in 2021 of a global minimum tax of 15% on multinationals and it now wants a similar scheme for the super-rich, which it says have effective tax rates equivalent to 0% to 0.5% of their wealth due to the frequent use of shell companies.

Due to the automatic exchange of bank information, the group estimates that offshore tax evasion has declined by a factor of about three over the last 10 years. The global minimum tax of 15% on multinationals introduced by 140 nations in 2021 was crucial in that process, but "has been dramatically weakened" in the intervening period, the report finds. It was initially expected to increase global corporate tax revenues by close to 10%, but a growing list of loopholes has reduced its expected revenues by a factor of 2.

The group's key proposal is a global minimum tax on billionaires, equal to 2% of their wealth. That would raise close to $250 billion from less than 3,000 individuals annually. A strengthened global minimum tax on multinational companies, free of loopholes, would raise an additional $250 billion per year.

Taxing companies is one thing, taxing increasingly mobile wealth is a bigger challenge.

In other news...

Stephen Springham unpacks the impact of Britain's Indian summer on retail sales, and makes some predictions for the final quarter. Read it here.

Plus, British workers coming into the office every day outnumber those who spend part of the week working from home (Bloomberg).